Quick Links

Cintas-UniFirst $5.5B Merger Clears Shareholder Vote: Merger-Arb Spread and CTAS Synergy Play Come Into Focus

Data Snapshot

Key Takeaways

- •UniFirst shareholders have approved the Cintas acquisition at $155 cash + 0.7720 CTAS shares per UNF share (~$5.5B enterprise value at deal terms).

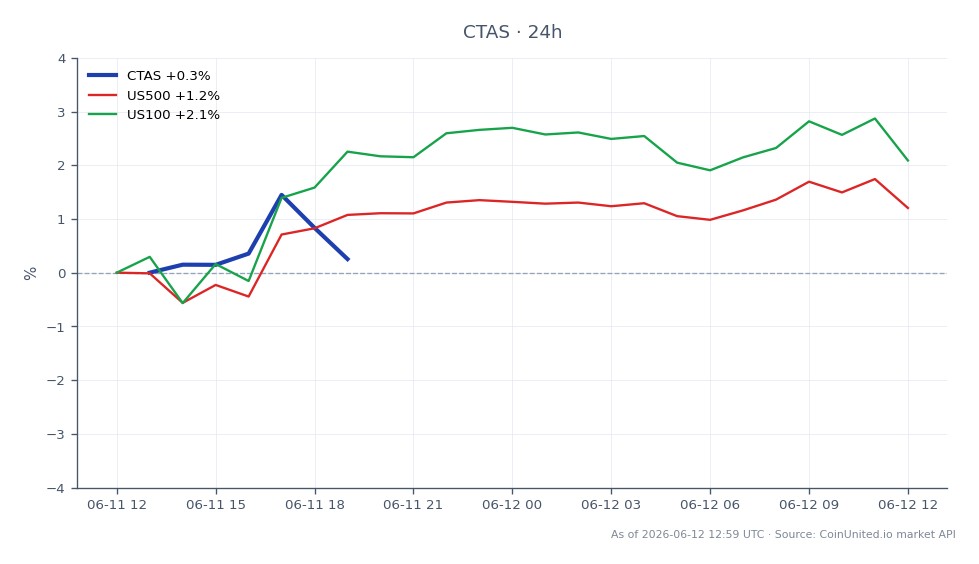

- •With CTAS trading at $182.08, the stock leg of the deal is worth ~$140.57, making the gross implied deal value ~$295.57 per UNF share — the gap to this is the live arb spread.

- •Cintas's $375M synergy target and EPS accretion by year two post-close are the core CTAS bull catalysts; antitrust clearance is the key risk variable.

- •A $350M reverse termination fee from Cintas limits arb downside in a regulatory break scenario — a meaningful structural floor.

- •UNF's eventual index removal and CTAS's rising market-cap weight will generate passive rebalancing flows worth monitoring for systematic traders.

Cintas Corporation's $5.5 billion acquisition of UniFirst Corporation has cleared a critical milestone: shareholder approval. As reported by Cintas's official newsroom and confirmed through SEC filing

Event Analysis

Cintas Corporation's $5.5 billion acquisition of UniFirst Corporation has cleared a critical milestone: shareholder approval. As reported by Cintas's official newsroom and confirmed through SEC filings, the deal offers UniFirst holders $155.00 in cash plus 0.7720 Cintas shares per UniFirst share — implying a per-share value of roughly $310 based on a CTAS reference price of $200.77 as of March 9, 2026. With a Croatti-family voting bloc controlling approximately two-thirds of UniFirst's voting power already committed via a formal Voting Agreement, approval was structurally near-certain from announcement.

What makes this deal strategically significant is the depth of industrial consolidation it represents. Cintas and UniFirst are the two dominant players in U.S. uniform rental and facility services — a capital-intensive, route-density-driven business where scale directly compresses unit costs. At roughly 8.0x trailing EBITDA including synergies, Cintas is acquiring pricing power and route density, not just revenue. Management projects approximately $375 million in operating-cost synergies within four years, spanning materials, production, logistics, and SG&A. This is the kind of transaction that reshapes competitive dynamics for smaller regional operators and aligns with the broader global acquisition and consolidation wave reshaping U.S. industrials in 2026.

The financing structure is conservative by deal standards: a $2.85 billion senior unsecured 364-day bridge loan (underwritten by Morgan Stanley, KeyBank, and Wells Fargo) funds the cash leg, with pro forma net leverage targeted at approximately 1.5x debt/EBITDA post-close — well within investment-grade territory. The outside termination date of January 10, 2027, with two possible 4-month extensions, defines the closing window and frames the risk-arb timeline. A $350 million reverse termination fee payable by Cintas if antitrust action blocks the deal signals meaningful commitment and partially floors downside for arb holders in a break scenario.

This deal fits squarely within the M&A acquisition wave and cross-sector acquisition repricing themes gaining momentum across U.S. equities in 2026. For those tracking the broader pattern, our M&A trading guide covers how acquisition cycles tend to reprice sector peers beyond the direct targets.

What This Means for Traders

The primary trade structure here is a classic merger arbitrage: long UniFirst (UNF) against a short in Cintas (CTAS) sized at the 0.772 share hedge ratio, capturing spread compression as regulatory risk declines toward closing. With CTAS currently trading at $182.08 (per live market data), the stock-leg value of the deal is approximately $140.57 per UNF share, plus $155 cash — implying a gross deal value near $295.57 at current CTAS levels. The spread to that implied value represents the arb opportunity, priced for antitrust and timing risk. Traders can explore acquisition arbitrage strategies for a deeper framework on sizing and hedging these setups.

For directional CTAS traders, the near-term setup is more complex. Acquirers frequently trade down on deal announcement and during integration uncertainty, and CTAS's current price reflects this. The bull case hinges on market confidence in the $375M synergy target and EPS accretion by the end of year two post-close. The bear case centers on integration execution risk and any antitrust complications that could widen the spread and drag CTAS further. Monitoring regulatory clearance milestones will be the key catalyst sequence for both legs. The 2026 Stocks Market Outlook provides broader sector context for U.S. industrials positioning this year.

Index-aware traders should also note that UNF's eventual removal from broad U.S. equity indices will trigger passive rebalancing flows, and CTAS's increased market cap post-merger may lift its index weight over time — a secondary but real flow dynamic for systematic strategies.

Trade Cintas Corporation on CoinUnited.io

Trade CTAS with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

Take 0.7720 × current CTAS price + $155 cash. At CTAS's live price of $182.08, that gives approximately $295.57 per UNF share — the gap between UNF's market price and this figure is your arb spread, representing residual closing risk.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.

">%0D%0A <path d="m65.883 9.018.032 5.181h-1.223c-.773-3.733-2.671-5.73-5.797-5.73-4.441 0-6.5 4.442-6.5 9.913 0 5.985 2.38 10.588 6.79 10.588 3.024 0 5.084-1.898 6.211-6.597h1.287l-.482 6.05a13.606 13.606 0 0 1-7.434 1.93c-7.016 0-11.36-4.409-11.36-11.071 0-7.467 4.989-12.166 11.36-12.166a12.961 12.961 0 0 1 7.112 1.899M68.714 21.89c0-5.47 3.572-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.573 9.205-8.367 9.205a7.908 7.908 0 0 1-8.271-8.464zm11.876.354c0-4.762-1.095-8.406-3.669-8.406-2.38 0-3.478 2.703-3.478 6.92 0 4.762 1.126 8.431 3.701 8.431 2.382 0 3.444-2.735 3.444-6.956M93.236 27.555c0 1.126.515 1.318 2.03 1.416v1.062h-8.497V28.97c1.514-.097 2.03-.29 2.03-1.415V16.16l-1.93-1.126v-.611l5.663-1.77h.709l-.005 14.9zM88.345 8.18a2.625 2.625 0 0 1 5.246 0 2.625 2.625 0 0 1-5.246 0zM109.007 18.157c0-1.867-.709-2.8-2.479-2.8a6.474 6.474 0 0 0-3.604 1.319v10.877c0 1.126.482 1.319 1.962 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.93-1.126v-.612l5.76-1.77h.741l-.129 3.154a7.735 7.735 0 0 1 5.954-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.995 1.416v1.062h-8.432V28.97c1.48-.097 1.963-.29 1.963-1.416v-9.396zM123.52 21.851c0 3.927 1.706 6.308 5.247 6.308 3.54 0 5.985-1.867 5.985-6.5V10.82c0-1.74-.419-2.03-3.058-2.253V7.442h7.37v1.126c-2.252.258-2.574.515-2.574 2.253v11.425c0 5.535-3.797 8.116-8.561 8.116-5.697 0-9.108-2.64-9.108-8.174v-11.4c0-1.77-.321-1.965-2.574-2.221V7.44h9.849v1.126c-2.253.258-2.574.45-2.574 2.22l-.002 11.064zM152.26 18.157c0-1.867-.707-2.8-2.478-2.8a6.484 6.484 0 0 0-3.605 1.319v10.877c0 1.126.483 1.319 1.964 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.931-1.126v-.612l5.761-1.77h.74l-.129 3.154a7.731 7.731 0 0 1 5.953-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.996 1.416v1.062h-8.432V28.97c1.479-.097 1.962-.29 1.962-1.416v-9.396zM166.259 27.555c0 1.126.515 1.318 2.029 1.416v1.062h-8.496V28.97c1.512-.097 2.029-.29 2.029-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.709l-.003 14.9zM161.368 8.18a2.62 2.62 0 0 1 2.622-2.518 2.625 2.625 0 0 1 2.623 2.518 2.626 2.626 0 0 1-4.441 1.786 2.62 2.62 0 0 1-.804-1.786zM175.33 12.976h4.183v1.48h-4.183v10.652c0 1.964.741 2.8 2.253 2.8a3.755 3.755 0 0 0 2.414-.901l.387.58a5.65 5.65 0 0 1-4.956 2.768c-2.64 0-4.57-1.384-4.57-4.989v-10.91h-1.996v-.741a13.265 13.265 0 0 0 5.508-4.928h.965l-.005 4.189zM195.514 19.38v.741h-10.492c-.129 4.506 2.189 7.177 5.342 7.177a5.427 5.427 0 0 0 4.796-2.609l.515.29a6.75 6.75 0 0 1-6.888 5.374c-4.665 0-7.787-3.443-7.787-8.406 0-5.507 3.539-9.3 7.948-9.3 4.313 0 6.566 2.864 6.566 6.726m-10.427-.45h6.437c0-3.025-.805-5.085-2.899-5.085-2.125 0-3.283 2.125-3.541 5.084M207.001 7.054v-.676l5.696-1.545h.707v21.788c0 1.094.064 1.45 1.287 1.545l.805.064v.965l-5.857 1.16h-.838l.129-2.993a6.145 6.145 0 0 1-5.181 2.993c-3.895 0-6.5-3.154-6.5-8.046 0-6.087 3.604-9.59 8.206-9.59a5.117 5.117 0 0 1 3.478 1.126V8.048l-1.932-.994zm-5.342 13.709c0 3.926 1.609 6.855 4.538 6.855a3.901 3.901 0 0 0 2.736-1.03v-8.496c0-2.51-1.062-3.99-2.993-3.99-2.703 0-4.28 2.64-4.28 6.667M219.683 24.754a2.796 2.796 0 0 1 2.587 1.729 2.8 2.8 0 1 1-5.387 1.072 2.75 2.75 0 0 1 1.721-2.6 2.753 2.753 0 0 1 1.079-.2zM230.592 27.555c0 1.126.516 1.318 2.029 1.416v1.062h-8.501V28.97c1.512-.097 2.03-.29 2.03-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.708l.002 14.9zM225.7 8.18a2.626 2.626 0 0 1 4.441-1.787c.488.47.777 1.11.804 1.787a2.625 2.625 0 0 1-5.245 0zM233.842 21.89c0-5.47 3.573-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.572 9.205-8.366 9.205a7.904 7.904 0 0 1-7.809-5.179 7.904 7.904 0 0 1-.463-3.285zm11.876.354c0-4.762-1.094-8.406-3.669-8.406-2.382 0-3.479 2.703-3.479 6.92 0 4.762 1.126 8.431 3.7 8.431 2.382 0 3.444-2.735 3.444-6.956M18.386.684a17.469 17.469 0 1 0 0 34.937 17.469 17.469 0 0 0 0-34.937zm0 31.74a14.277 14.277 0 1 1 0-28.554 14.277 14.277 0 0 1 0 28.554z" fill="%23fff"/>%0D%0A <path d="M18.393 36.019a17.868 17.868 0 1 1 17.86-17.868 17.887 17.887 0 0 1-17.86 17.868zm0-34.938a17.07 17.07 0 1 0 17.063 17.07 17.089 17.089 0 0 0-17.063-17.07zm0 31.74a14.675 14.675 0 1 1 10.366-4.297 14.691 14.691 0 0 1-10.373 4.303m0-28.552a13.877 13.877 0 1 0 13.879 13.878A13.893 13.893 0 0 0 18.386 4.275z" fill="%23fff"/>%0D%0A <path d="M17.42 8.46a8.46 8.46 0 1 1-16.923 0 8.46 8.46 0 0 1 16.924 0" fill="%23E48A22"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="sy6kzo59ya">%0D%0A <path fill="%23fff" transform="translate(.5)" d="M0 0h250v36.019H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

"><path fill="%23fff" transform="scale(1.9886)" d="M27.72,2.61a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-30.14,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-32.16,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-34.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-40.2,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-58.29,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-62.32,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m30.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m22.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m34.16,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m18.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.27,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-56.29,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-48.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2"/><path d="M123.088,117.106a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M123.088,133.085a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M91.095,145.087a1.987,1.987,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989,2.01,2.01,0,0,1,1.989-1.988zM107.109,145.087a1.988,1.988,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989c-.035-1.081.872-1.988,1.989-1.988zM115.098,145.087a1.987,1.987,0,1,1,0,3.977,1.987,1.987,0,0,1-1.988-1.989c-.035-1.081.872-1.988,1.988-1.988zM123.088,145.087a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M151.069,149.064a1.988,1.988,0,1,1-1.989,1.989c-.035-1.082.872-1.989,1.989-1.989zM25.271,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491c0-1.575,1.277-2.852,2.83-2.852h6.492a2.852,2.852,0,0,1,2.852,2.852v6.49h.021z" fill="%23fff"/><path d="M33.38,30.568a2.852,2.852,0,0,1-2.852,2.851H7.798a2.852,2.852,0,0,1-2.851-2.851V7.817a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.75h-.021zM29.315,11.86a2.852,2.852,0,0,0-2.852-2.852H11.842A2.852,2.852,0,0,0,8.99,11.86v14.642a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852V11.86h-.021zM25.271,142.338a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491a2.852,2.852,0,0,1,2.852-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.491z" fill="%23fff"/><path d="M33.38,150.468a2.852,2.852,0,0,1-2.852,2.852H7.798a2.852,2.852,0,0,1-2.851-2.852v-22.751a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.751h-.021zm-4.065-18.686a2.852,2.852,0,0,0-2.852-2.852H11.842a2.852,2.852,0,0,0-2.852,2.852v14.621a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852v-14.621h-.021zM145.171,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.491a2.851,2.851,0,0,1-2.851-2.852v-6.491a2.851,2.851,0,0,1,2.851-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.49z" fill="%23fff"/><path d="M153.301,30.568a2.852,2.852,0,0,1-2.852,2.851h-22.75a2.852,2.852,0,0,1-2.852-2.851V7.817a2.852,2.852,0,0,1,2.852-2.852h22.75a2.852,2.852,0,0,1,2.852,2.852v22.75zm-4.065-18.707a2.852,2.852,0,0,0-2.852-2.852h-14.621a2.852,2.852,0,0,0-2.851,2.852v14.642a2.852,2.852,0,0,0,2.851,2.852h14.621a2.852,2.852,0,0,0,2.852-2.852V11.86zM78.535,62.051c-9.176,0-16.607,7.431-16.607,16.607,0,9.176,7.431,16.607,16.607,16.607,9.176,0,16.607-7.431,16.607-16.607,0-9.176-7.431-16.607-16.607-16.607zm0,30.214c-7.501,0-13.572-6.07-13.572-13.572,0-7.501,6.07-13.572,13.572-13.572,7.501,0,13.572,6.07,13.572,13.572,0,7.501-6.071,13.572-13.572,13.572z" fill="%23fff"/><path d="M78.535,95.649c-9.385,0-16.991-7.64-16.991-16.99,0-9.386,7.64-16.992,16.99-16.992,9.386,0,16.992,7.64,16.992,16.991,0,9.35-7.64,16.991-16.991,16.991zm0-33.214c-8.966,0-16.258,7.292-16.258,16.258s7.291,16.258,16.258,16.258c8.966,0,16.258-7.291,16.258-16.258-.035-8.966-7.292-16.258-16.258-16.258zm0,30.214c-7.71,0-13.956-6.28-13.956-13.956,0-7.71,6.28-13.956,13.956-13.956,7.71,0,13.956,6.28,13.956,13.956,0,7.676-6.28,13.956-13.956,13.956zm0-27.179c-7.292,0-13.223,5.931-13.223,13.223,0,7.292,5.931,13.223,13.223,13.223,7.292,0,13.223-5.931,13.223-13.223-.035-7.292-5.966-13.223-13.223-13.223z" fill="%23fff"/><path d="M69.569,77.507a8.06,8.06,0,1,0,0-16.119,8.06,8.06,0,0,0,0,16.119z" fill="%23E48A22"/></g><defs><clipPath id="arusb4546a"><path fill="%23fff" transform="translate(0 .019)" d="M0,0h157v157H0z"/></clipPath></defs></svg>)

">%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23fff"/>%0D%0A <path d="M106.646 32.584H4.356A3.857 3.857 0 0 1 .5 28.741V3.867A3.853 3.853 0 0 1 4.355.02h102.29a3.86 3.86 0 0 1 3.855 3.848V28.74a3.853 3.853 0 0 1-3.854 3.845z" fill="%23A6A6A6"/>%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23000"/>%0D%0A <path d="M25.063 16.13a4.717 4.717 0 0 1 2.25-3.961 4.84 4.84 0 0 0-3.812-2.059c-1.603-.168-3.159.959-3.976.959-.833 0-2.09-.942-3.447-.915a5.079 5.079 0 0 0-4.271 2.603c-1.848 3.195-.47 7.89 1.3 10.472.886 1.265 1.92 2.679 3.274 2.626 1.325-.052 1.82-.84 3.417-.84 1.584 0 2.05.84 3.43.81 1.42-.021 2.317-1.27 3.171-2.546a10.434 10.434 0 0 0 1.452-2.952 4.572 4.572 0 0 1-2.786-4.197h-.003zm-2.61-7.718a4.643 4.643 0 0 0 1.065-3.33 4.74 4.74 0 0 0-3.064 1.583 4.42 4.42 0 0 0-1.092 3.207 3.917 3.917 0 0 0 3.091-1.46zM44.25 25.674H42.4l-1.015-3.183H37.86l-.966 3.183H35.09l3.493-10.838h2.156l3.509 10.838h.002zm-3.17-4.517-.918-2.83c-.097-.29-.28-.97-.547-2.042h-.033c-.108.461-.28 1.142-.515 2.042l-.902 2.83h2.914zm12.137.515a4.422 4.422 0 0 1-1.085 3.152 3.178 3.178 0 0 1-2.41 1.03 2.415 2.415 0 0 1-2.235-1.109v4.1H45.75v-8.417c0-.835-.021-1.691-.064-2.569h1.529l.097 1.239h.032a3.09 3.09 0 0 1 2.398-1.395 3.095 3.095 0 0 1 2.552 1.088c.645.817.973 1.84.925 2.88l-.001.001zm-1.77.064a3.22 3.22 0 0 0-.516-1.882 1.781 1.781 0 0 0-1.513-.771c-.427 0-.84.15-1.166.426-.349.284-.59.678-.684 1.118a2.26 2.26 0 0 0-.08.528v1.302a2.09 2.09 0 0 0 .525 1.44 1.737 1.737 0 0 0 1.36.587 1.783 1.783 0 0 0 1.529-.755c.389-.59.58-1.29.544-1.995v.002zm10.768-.064a4.422 4.422 0 0 1-1.084 3.152 3.182 3.182 0 0 1-2.413 1.03 2.415 2.415 0 0 1-2.233-1.109v4.1h-1.739v-8.417c0-.835-.021-1.691-.065-2.569h1.53l.096 1.239h.033a3.092 3.092 0 0 1 3.803-1.153c.443.189.836.478 1.148.846.645.817.973 1.84.924 2.88v.001zm-1.771.064a3.22 3.22 0 0 0-.517-1.882 1.778 1.778 0 0 0-1.511-.771c-.427 0-.841.15-1.168.426-.349.284-.59.678-.683 1.118-.048.172-.075.35-.082.528v1.302a2.097 2.097 0 0 0 .523 1.44 1.74 1.74 0 0 0 1.361.587 1.781 1.781 0 0 0 1.53-.755c.39-.59.581-1.289.547-1.995v.002zm11.831.9a2.893 2.893 0 0 1-.964 2.251 4.278 4.278 0 0 1-2.956.949 5.163 5.163 0 0 1-2.809-.675l.402-1.447a4.84 4.84 0 0 0 2.511.676 2.371 2.371 0 0 0 1.53-.442 1.444 1.444 0 0 0 .548-1.181 1.511 1.511 0 0 0-.452-1.11 4.188 4.188 0 0 0-1.496-.836c-1.9-.707-2.85-1.742-2.85-3.104a2.737 2.737 0 0 1 1.006-2.187 3.981 3.981 0 0 1 2.664-.852 5.27 5.27 0 0 1 2.463.515l-.437 1.415a4.31 4.31 0 0 0-2.084-.498 2.121 2.121 0 0 0-1.438.45 1.289 1.289 0 0 0-.437.982 1.327 1.327 0 0 0 .5 1.061 5.63 5.63 0 0 0 1.577.836c.78.274 1.485.725 2.06 1.318.45.521.686 1.192.663 1.88v-.002zm5.762-3.472H76.12v3.794c0 .965.338 1.447 1.014 1.447.26.006.52-.021.773-.08l.048 1.318a3.942 3.942 0 0 1-1.352.192 2.085 2.085 0 0 1-1.61-.63 3.077 3.077 0 0 1-.578-2.107v-3.94h-1.141v-1.302h1.141v-1.43l1.707-.515v1.943h1.915l-.001 1.31zm8.627 2.54a4.284 4.284 0 0 1-1.03 2.959 3.674 3.674 0 0 1-2.865 1.19 3.504 3.504 0 0 1-2.746-1.14 4.154 4.154 0 0 1-1.022-2.879 4.249 4.249 0 0 1 1.054-2.974 3.655 3.655 0 0 1 2.842-1.155 3.577 3.577 0 0 1 2.768 1.142 4.1 4.1 0 0 1 1 2.856v.001zm-1.802.04a3.496 3.496 0 0 0-.465-1.843 1.72 1.72 0 0 0-1.562-.931 1.746 1.746 0 0 0-1.594.93 3.554 3.554 0 0 0-.466 1.877 3.485 3.485 0 0 0 .466 1.844 1.782 1.782 0 0 0 3.141-.015 3.51 3.51 0 0 0 .48-1.863v.001zm7.454-2.356a3.03 3.03 0 0 0-.547-.047 1.641 1.641 0 0 0-1.42.692 2.605 2.605 0 0 0-.434 1.543v4.1H88.18v-5.355c0-.82-.017-1.64-.052-2.46h1.514l.063 1.495h.049c.164-.488.466-.918.868-1.239.363-.271.804-.419 1.257-.42.145 0 .29.01.435.032v1.656l.002.003zm7.774 2.011c.004.264-.017.528-.064.788h-5.214a2.262 2.262 0 0 0 .756 1.77 2.59 2.59 0 0 0 1.707.544c.72.01 1.435-.115 2.11-.368l.272 1.204a6.527 6.527 0 0 1-2.623.483 3.805 3.805 0 0 1-2.86-1.067 3.95 3.95 0 0 1-1.039-2.87 4.473 4.473 0 0 1 .967-2.942 3.331 3.331 0 0 1 2.734-1.253 2.916 2.916 0 0 1 2.56 1.253c.48.728.722 1.586.694 2.456v.002zm-1.658-.45a2.348 2.348 0 0 0-.337-1.335 1.518 1.518 0 0 0-1.384-.725 1.648 1.648 0 0 0-1.381.706c-.297.392-.475.86-.515 1.35h3.62l-.003.004zM37.359 11.005a11.12 11.12 0 0 1-1.25-.063v-5.24c.487-.075.98-.112 1.472-.11 1.994 0 2.912.98 2.912 2.576 0 1.842-1.085 2.837-3.134 2.837zm.292-4.742a3.49 3.49 0 0 0-.688.055v3.984c.192.02.385.028.578.023 1.306 0 2.05-.743 2.05-2.133-.002-1.24-.674-1.929-1.94-1.929zm5.702 4.78a1.832 1.832 0 0 1-1.755-1.225 1.826 1.826 0 0 1-.097-.75 1.87 1.87 0 0 1 1.916-2.031 1.817 1.817 0 0 1 1.851 1.968 1.881 1.881 0 0 1-1.915 2.04v-.002zm.032-3.382c-.617 0-1.012.577-1.012 1.383 0 .79.404 1.365 1.005 1.365.6 0 1.004-.616 1.004-1.383 0-.779-.396-1.363-.996-1.363V7.66zm8.29-.545-1.203 3.84h-.784L49.19 9.29a12.619 12.619 0 0 1-.309-1.24h-.016c-.07.42-.174.835-.308 1.24l-.53 1.668h-.792l-1.132-3.841h.878l.435 1.826c.103.435.19.845.263 1.232h.017c.062-.323.165-.727.315-1.225l.546-1.833h.696l.523 1.795c.126.435.229.861.309 1.264h.023c.062-.426.15-.848.262-1.264l.468-1.795h.84-.004zm4.426 3.84h-.854V8.75c0-.679-.263-1.02-.776-1.02a.888.888 0 0 0-.854.942v2.284h-.854v-2.74c0-.34-.009-.705-.032-1.1h.751l.04.593h.024a1.38 1.38 0 0 1 1.219-.67c.806 0 1.336.616 1.336 1.619v2.3-.002zm2.356 0h-.855v-5.6h.855v5.6zm3.115.088a1.832 1.832 0 0 1-1.851-1.976 1.87 1.87 0 0 1 1.914-2.031 1.816 1.816 0 0 1 1.851 1.968 1.88 1.88 0 0 1-1.914 2.04v-.001zm.032-3.383c-.617 0-1.012.578-1.012 1.383 0 .79.404 1.366 1.003 1.366.6 0 1.005-.617 1.005-1.384 0-.779-.394-1.363-.998-1.363l.002-.002zm5.252 3.296-.063-.442h-.022a1.314 1.314 0 0 1-1.125.53 1.118 1.118 0 0 1-1.178-1.131c0-.946.823-1.438 2.247-1.438v-.071c0-.506-.268-.76-.798-.76a1.8 1.8 0 0 0-1.004.286l-.174-.561a2.46 2.46 0 0 1 1.32-.332c1.005 0 1.511.529 1.511 1.588v1.415a5.79 5.79 0 0 0 .056.917l-.77-.001zm-.118-1.913c-.949 0-1.425.23-1.425.774a.543.543 0 0 0 .586.6.818.818 0 0 0 .841-.78l-.002-.594zm4.982 1.913-.04-.617h-.024a1.288 1.288 0 0 1-1.234.704c-.927 0-1.614-.814-1.614-1.96 0-1.201.712-2.049 1.683-2.049a1.157 1.157 0 0 1 1.084.523h.017V5.35h.856v4.57c0 .372.009.72.031 1.036h-.76zm-.126-2.259a.93.93 0 0 0-.9-.998c-.631 0-1.021.561-1.021 1.351 0 .775.402 1.305 1.003 1.305a.96.96 0 0 0 .914-1.019v-.639h.004zm6.277 2.347a1.831 1.831 0 0 1-1.85-1.975 1.87 1.87 0 0 1 1.913-2.031 1.816 1.816 0 0 1 1.852 1.968 1.88 1.88 0 0 1-1.916 2.038zm.031-3.382c-.616 0-1.011.577-1.011 1.383 0 .79.403 1.365 1.003 1.365.6 0 1.005-.616 1.005-1.383 0-.782-.394-1.366-1-1.366h.003zm6.478 3.296h-.857V8.753c0-.68-.263-1.02-.775-1.02a.888.888 0 0 0-.854.94v2.285h-.855V8.215c0-.34-.009-.704-.032-1.099h.752l.04.593h.023a1.38 1.38 0 0 1 1.218-.671c.807 0 1.338.616 1.338 1.62l.002 2.3zm5.749-3.2h-.94v1.864c0 .473.165.712.497.712.128 0 .255-.013.38-.04l.023.648c-.213.07-.438.103-.663.095-.673 0-1.076-.372-1.076-1.344V7.758h-.56v-.64h.56v-.704l.841-.254v.956h.94v.641l-.002.001zm4.52 3.2h-.853v-2.19c0-.687-.26-1.035-.775-1.035a.838.838 0 0 0-.856.909v2.315h-.851V5.355h.854v2.307h.017a1.296 1.296 0 0 1 1.156-.624c.814 0 1.312.63 1.312 1.636l-.003 2.285zm4.635-1.715H96.72a1.102 1.102 0 0 0 1.21 1.137c.353.004.704-.058 1.035-.181l.133.593a3.212 3.212 0 0 1-1.29.237 1.789 1.789 0 0 1-1.913-1.936c0-1.178.728-2.063 1.818-2.063.982 0 1.598.728 1.598 1.826.006.13-.004.26-.03.387h.003zm-.783-.609c0-.593-.3-1.011-.846-1.011a1.014 1.014 0 0 0-.934 1.011h1.78z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="uavr3vx5ga">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

">%0D%0A <path d="M106.426 32.584H4.574a4.037 4.037 0 0 1-3.775-2.507 4.029 4.029 0 0 1-.3-1.564V4.09A4.028 4.028 0 0 1 3.01.318a4.038 4.038 0 0 1 1.565-.3h101.852a4.039 4.039 0 0 1 3.774 2.507c.203.496.305 1.028.3 1.564v24.424a4.032 4.032 0 0 1-4.074 4.071z" fill="%23000"/>%0D%0A <path d="M106.426.67a3.445 3.445 0 0 1 3.422 3.42v24.424a3.444 3.444 0 0 1-3.422 3.42H4.574a3.444 3.444 0 0 1-3.422-3.42V4.089A3.438 3.438 0 0 1 4.574.67h101.852zm0-.651H4.574A4.088 4.088 0 0 0 .5 4.089v24.425a4.029 4.029 0 0 0 2.508 3.771 4.039 4.039 0 0 0 1.566.3h101.852a4.04 4.04 0 0 0 2.892-1.181 4.023 4.023 0 0 0 1.182-2.89V4.089a4.082 4.082 0 0 0-4.074-4.07z" fill="%23A6A6A6"/>%0D%0A <path d="M39.122 8.323a2.216 2.216 0 0 1-.57 1.628 2.558 2.558 0 0 1-3.585 0 2.393 2.393 0 0 1-.734-1.794 2.394 2.394 0 0 1 .734-1.785 2.395 2.395 0 0 1 1.792-.736c.34.004.676.087.978.244.292.122.546.318.736.57l-.407.407a1.52 1.52 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57 1.677 1.677 0 0 0-.573 1.384 1.675 1.675 0 0 0 .57 1.384c.355.336.817.538 1.304.57a1.789 1.789 0 0 0 1.386-.57 1.347 1.347 0 0 0 .407-.976h-1.793v-.652h2.366v.326h-.003zm3.748-2.036h-2.2v1.547h2.038v.57H40.67v1.547h2.2v.651h-2.854V5.718h2.855v.57zm2.69 4.315h-.653V6.287h-1.385v-.57h3.422v.57H45.56v4.315zm3.747 0V5.718h.652v4.884h-.652zm3.423 0h-.652V6.287h-1.385v-.57h3.34v.57h-1.385v4.315h.082zm7.74-.65a2.559 2.559 0 0 1-3.585 0 2.394 2.394 0 0 1-.736-1.792 2.393 2.393 0 0 1 .736-1.791 2.558 2.558 0 0 1 3.586 0 2.395 2.395 0 0 1 .735 1.791 2.391 2.391 0 0 1-.736 1.791zm-3.096-.408c.346.35.812.554 1.304.57a1.623 1.623 0 0 0 1.304-.57c.366-.369.57-.867.57-1.387a1.675 1.675 0 0 0-.57-1.381 1.924 1.924 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57c-.365.367-.57.864-.57 1.381a1.676 1.676 0 0 0 .57 1.387zm4.726 1.058V5.718h.736l2.366 3.826V5.718h.651v4.884h-.657l-2.523-3.989v3.99H62.1z" fill="%23fff" stroke="%23fff" stroke-width=".2" stroke-miterlimit="10"/>%0D%0A <path d="M55.989 17.767a3.43 3.43 0 0 0-3.258 2.149c-.173.43-.256.89-.246 1.352a3.47 3.47 0 0 0 2.159 3.241c.427.175.884.263 1.345.26a3.432 3.432 0 0 0 3.258-2.15c.172-.429.256-.889.245-1.351a3.376 3.376 0 0 0-3.503-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-7.578-5.536a3.431 3.431 0 0 0-3.258 2.149c-.172.43-.256.89-.246 1.352a3.472 3.472 0 0 0 2.16 3.241c.426.175.883.263 1.344.26a3.432 3.432 0 0 0 3.258-2.15c.173-.429.256-.889.246-1.351a3.376 3.376 0 0 0-3.504-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-9.044-4.478v1.466h3.503a3.077 3.077 0 0 1-.815 1.872 3.607 3.607 0 0 1-2.688 1.059 3.796 3.796 0 0 1-3.83-3.908 3.838 3.838 0 0 1 2.347-3.605c.47-.198.973-.301 1.483-.303a4.041 4.041 0 0 1 2.688 1.056l1.06-1.056a5.223 5.223 0 0 0-3.667-1.466 5.49 5.49 0 0 0-5.46 5.373 5.49 5.49 0 0 0 5.46 5.374 4.693 4.693 0 0 0 3.748-1.547 4.9 4.9 0 0 0 1.304-3.42c.017-.3-.01-.6-.082-.892h-5.051v-.003zm36.992 1.14a3.163 3.163 0 0 0-2.933-2.198c-1.793 0-3.26 1.384-3.26 3.5a3.406 3.406 0 0 0 3.423 3.502 3.345 3.345 0 0 0 2.852-1.547l-1.141-.814a1.986 1.986 0 0 1-1.711.976 1.769 1.769 0 0 1-1.711-1.058l4.644-1.954-.163-.407zm-4.726 1.14a1.977 1.977 0 0 1 1.793-2.035 1.441 1.441 0 0 1 1.303.732l-3.096 1.303zm-3.83 3.34h1.549V14.267h-1.548v10.18zm-2.444-5.943a2.682 2.682 0 0 0-1.874-.814 3.502 3.502 0 0 0-3.34 3.501 3.369 3.369 0 0 0 2.048 3.149c.409.174.848.266 1.292.27a2.34 2.34 0 0 0 1.793-.814h.081v.489c0 1.302-.736 2.035-1.874 2.035a1.81 1.81 0 0 1-1.711-1.221l-1.304.57a3.36 3.36 0 0 0 3.096 2.035c1.793 0 3.26-1.058 3.26-3.582v-6.19h-1.467v.572zm-1.792 4.804a2.025 2.025 0 0 1-1.956-2.117 2.02 2.02 0 0 1 1.956-2.117 1.961 1.961 0 0 1 1.874 2.117 1.957 1.957 0 0 1-1.875 2.114v.003zm19.881-9.035h-3.667v10.175h1.548v-3.83h2.119a3.185 3.185 0 0 0 3.087-1.92 3.177 3.177 0 0 0-1.82-4.237 3.185 3.185 0 0 0-1.267-.193v.005zm.082 4.885h-2.2V15.65h2.2a1.788 1.788 0 0 1 1.792 1.71 1.862 1.862 0 0 1-1.793 1.791v.005zm9.37-1.465c-1.14 0-2.282.488-2.689 1.547l1.385.57a1.438 1.438 0 0 1 1.385-.736 1.532 1.532 0 0 1 1.63 1.303v.079a3.236 3.236 0 0 0-1.548-.407c-1.467 0-2.934.814-2.934 2.28a2.386 2.386 0 0 0 2.524 2.279 2.294 2.294 0 0 0 1.955-.977h.082v.817h1.466v-3.908a3.08 3.08 0 0 0-3.259-2.85l.003.003zm-.163 5.617c-.489 0-1.222-.244-1.222-.893 0-.814.896-1.058 1.63-1.058.48.002.954.113 1.385.326a1.895 1.895 0 0 1-1.793 1.62v.005zm8.555-5.373-1.71 4.396H99.5l-1.793-4.396h-1.63l2.69 6.188-1.549 3.419h1.548l4.153-9.607h-1.629.002zm-13.688 6.51h1.548V14.267h-1.548v10.18z" fill="%23fff"/>%0D%0A <path d="M8.974 6.125a1.59 1.59 0 0 0-.326 1.14v17.992a1.61 1.61 0 0 0 .408 1.14l.081.081 10.104-10.095v-.163L8.974 6.125z" fill="url(%23nqixmws78b)"/>%0D%0A <path d="m22.5 19.802-3.34-3.338v-.244l3.34-3.338.081.082 3.99 2.28c1.141.65 1.141 1.709 0 2.36L22.5 19.802z" fill="url(%23euwe5vohvc)"/>%0D%0A <path d="m22.581 19.72-3.422-3.418L8.974 26.477c.408.407.978.407 1.711.082l11.896-6.84z" fill="url(%23wso0uh08dd)"/>%0D%0A <path d="M22.581 12.882 10.685 6.125c-.736-.407-1.303-.326-1.71.081l10.184 10.096 3.422-3.42z" fill="url(%23mrdt54dj1e)"/>%0D%0A <path opacity=".2" d="m22.5 19.64-11.815 6.675a1.334 1.334 0 0 1-1.63 0l-.08.082.08.081a1.333 1.333 0 0 0 1.63 0L22.5 19.64z" fill="%23000"/>%0D%0A <path opacity=".12" d="M8.974 26.316a1.59 1.59 0 0 1-.326-1.14v.081a1.61 1.61 0 0 0 .408 1.14v-.081h-.082zm17.6-8.956L22.5 19.64l.081.08 3.993-2.279a1.355 1.355 0 0 0 .815-1.14c0 .408-.326.733-.815 1.059z" fill="%23000"/>%0D%0A <path opacity=".25" d="m10.685 6.206 15.89 9.037c.488.326.814.651.814 1.059a1.352 1.352 0 0 0-.815-1.14L10.685 6.125c-1.143-.652-2.037-.163-2.037 1.14v.08c0-1.22.894-1.79 2.037-1.139z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <linearGradient id="nqixmws78b" x1="18.265" y1="27.13" x2="2.062" y2="22.737" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2300A0FF"/>%0D%0A <stop offset=".007" stop-color="%2300A1FF"/>%0D%0A <stop offset=".26" stop-color="%2300BEFF"/>%0D%0A <stop offset=".512" stop-color="%2300D2FF"/>%0D%0A <stop offset=".76" stop-color="%2300DFFF"/>%0D%0A <stop offset="1" stop-color="%2300E3FF"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="euwe5vohvc" x1="28.064" y1="17.927" x2="8.353" y2="17.927" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FFE000"/>%0D%0A <stop offset=".409" stop-color="%23FFBD00"/>%0D%0A <stop offset=".775" stop-color="orange"/>%0D%0A <stop offset="1" stop-color="%23FF9C00"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="wso0uh08dd" x1="20.731" y1="16.06" x2="7.736" y2="-5.775" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FF3A44"/>%0D%0A <stop offset="1" stop-color="%23C31162"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="mrdt54dj1e" x1="6.443" y1="34.068" x2="12.205" y2="24.305" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2332A071"/>%0D%0A <stop offset=".069" stop-color="%232DA771"/>%0D%0A <stop offset=".476" stop-color="%2315CF74"/>%0D%0A <stop offset=".801" stop-color="%2306E775"/>%0D%0A <stop offset="1" stop-color="%2300F076"/>%0D%0A </linearGradient>%0D%0A <clipPath id="oefv1zwvza">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)