Quick Links

KKR's $7.6B DCC Buyout: Merger-Arb Spreads, Leverage Scenarios & PE Sector Read-Through

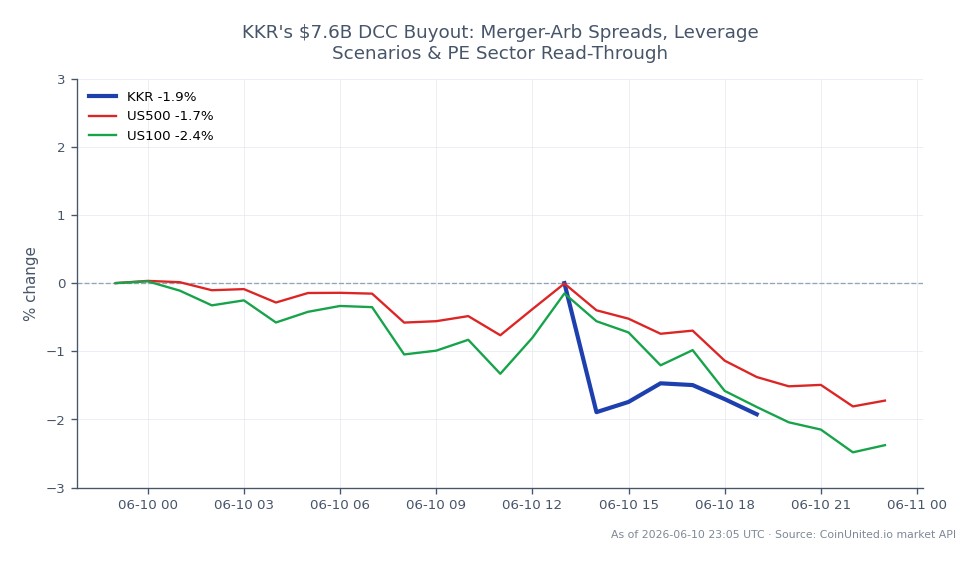

Data Snapshot

Key Takeaways

- •DCC shares will trade in a tight band near the $7.6B offer-implied price — realized volatility compresses, making high-leverage directional longs on DCC a spread-capture trade with discrete deal-break tail risk.

- •A 20x long DCC CFD captures the ~3% arb spread amplified to ~60% if the deal closes; a deal break could erase multiples of that gain — position sizing around approval milestones is critical.

- •KKR and listed PE peers (Blackstone, Apollo, Carlyle) receive a bullish sentiment read-through as active $7B+ deal flow signals LBO financing markets remain open.

- •The LBO's leveraged loan and HY bond supply is a credit market signal to watch — easy absorption is risk-on; difficult placement flags tightening conditions with broader equity implications.

- •Index deletion of DCC upon deal close will force passive-fund rebalancing; anticipating the replacement stock receiving incremental passive demand is a secondary trade opportunity.

DCC plc has publicly stated it supports a revised $7.6 billion buyout proposal from a KKR & Co.-led consortium, marking a significant escalation in what appears to be an iterative negotiation. The rev

Event Summary

DCC plc has publicly stated it supports a revised $7.6 billion buyout proposal from a KKR & Co.-led consortium, marking a significant escalation in what appears to be an iterative negotiation. The revised nature of the offer — implying prior terms were insufficient — typically signals the bid is approaching final, reducing the probability of further material price bumps. KKR, a global private equity heavyweight, would finance the transaction via a leveraged buyout structure drawing on syndicated loans and/or high-yield bonds or private credit. Final deal closure remains subject to shareholder vote and regulatory clearance in relevant jurisdictions (UK, EU). Investors should verify terms via DCC's official regulatory news releases.

The deal fits squarely within the broader global acquisition & consolidation wave sweeping distribution and B2B services sectors, and reinforces the cross-sector acquisition repricing thesis as private equity signals continued confidence in energy logistics and stable cash-flow businesses.

Leverage Impact Analysis

For leveraged traders on DCC stock CFDs, the post-announcement dynamic shifts the risk profile materially. Once a board-supported offer is public, DCC's share price anchors near the offer price — realized volatility typically compresses, and the stock trades in a tight merger-arb band.

Worked example — Merger-Arb long: If DCC trades at a ~3% discount to the $7.6B implied offer price (a typical arb spread for a supported LBO with regulatory risk), a 20x long DCC CFD captures that spread amplified 20x — roughly 60% return if the deal closes on schedule. However, a deal break could trigger a sharp mean-reversion toward pre-announcement levels, and a 20x position would face severe drawdown. Position sizing must account for deal-break tail risk.

KKR CFD angle: A 50x long KKR & Co CFD is a purer play on the PE deployment narrative. If KKR's stock re-rates +2% on deal-flow momentum, a 50x position returns ~100% on margin — but reverses sharply if financing conditions deteriorate or the deal signals capital overextension. Monitor LBO credit spread widening as an early warning.

Volatility on DCC compresses post-announcement for directional traders but event risk (shareholder vote, regulatory review) creates discrete gap scenarios. Reduce leverage heading into approval milestones.

Cross-Market Impact

Private equity sector: The deal reinforces bullish sentiment for listed PE names. KKR peers — Blackstone, Apollo, Carlyle — may see sympathetic re-rating as active deal flow signals LBO financing markets remain open. The M&A acquisition wave theme benefits broadly.

Indices: If DCC holds index weight in FTSE or European sector benchmarks, a confirmed take-private triggers eventual index deletion, creating passive-fund rebalancing flows. The S&P 500 Index and NASDAQ 100 Index see indirect support via improved risk appetite — large PE buyout activity historically correlates with broader equity risk-on sentiment.

Credit markets: A $7.6B LBO adds leveraged loan and high-yield bond supply. Easy absorption reinforces the narrative that credit conditions remain supportive; difficult placement would signal tightening — a negative read-through for risk assets broadly. Watch investment-grade and HY spreads post-syndication launch.

FX: Cross-border capital flows (USD/GBP or USD/EUR) are a minor factor at this deal size and unlikely to move major pairs independently.

Trading Considerations

Key levels to watch: DCC's share price relative to the implied offer value sets the arb spread — tightening spread signals market confidence in deal completion; widening signals rising break risk. For KKR CFDs, watch whether the stock holds post-announcement gains or fades as financing details emerge. The acquisition arbitrage guide provides deeper framework on spread dynamics. For broader context on how PE-driven deals move markets, see the mega-deal M&A wave analysis.

Primary risks: regulatory objection (energy distribution market share review), financing difficulty at current credit spreads, or a macro shock making LBO leverage unattractive. Any of these widens the arb spread sharply — critical to monitor before adding leverage.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

Post-announcement, DCC trades in a tight range near the offer price — high leverage amplifies the small arb spread but deal-break risk (regulatory block, financing failure) can cause sharp mean-reversion. Keep leverage moderate (10–20x maximum) and reduce further ahead of shareholder vote and regulatory decision dates.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.