Quick Links

South Korea's Canadian Crude Pivot: WTI at $97.16 and the Leverage Map for Energy Traders

Data Snapshot

Key Takeaways

- •HD Hyundai Oilbank's 548,000-barrel pilot cargo at ~$69.77/bbl — a $6–10/bbl discount to U.S. and Saudi grades — confirms Korean refiner economics heavily favor Canadian supply scale-up.

- •Leverage risk: A 100x long WTI CFD opened at $97.16 faces liquidation near the 24h low of $95.48 — this event provides no short-term WTI spot catalyst, making high-leverage longs vulnerable to mean-reversion.

- •USD/CAD is the cleaner cross-market trade: sustained Korean offtake at 16M bbl/year scale structurally improves Canada's trade balance and reduces CAD's U.S. demand dependency.

- •The Vancouver-to-Busan route bypasses Hormuz, Red Sea, and Suez entirely — in any Middle East escalation, Canadian barrel premiums widen sharply versus Middle Eastern grades, a key divergence trade.

- •WTI faces mild long-term relative pressure as Korean demand shifts from U.S. Gulf Coast barrels, potentially redirecting U.S. crude to Europe and compressing Brent-WTI spreads.

South Korea is executing a structural overhaul of its hydrocarbon sourcing, pivoting toward Canadian crude and prospective LNG supply. According to S&P Global and trade press reports, HD Hyundai Oilba

Event Summary

South Korea is executing a structural overhaul of its hydrocarbon sourcing, pivoting toward Canadian crude and prospective LNG supply. According to S&P Global and trade press reports, HD Hyundai Oilbank took delivery of a 548,000-barrel pilot cargo of Canadian heavy crude valued at C$82.3 million — the first such purchase since 2024. South Korea is now exploring scaling imports to up to 16 million barrels annually, which would more than triple current volumes and position Canada among Korea's top offshore suppliers.

The structural enabler is the Trans Mountain Expansion (TMX), which lifted Canadian pipeline export capacity from ~300,000 bpd to ~890,000 bpd, opening direct Pacific coast shipment routes to Asia. Canadian crude reached Korean refiners at approximately $69.77/bbl versus $77.50/bbl for U.S. crude and $75.96/bbl for Saudi barrels — a $6–10/bbl discount that makes the economics compelling. Shipments from Vancouver also bypass the Hormuz Strait energy supply shock risk corridor entirely, adding a geopolitical security premium.

Leverage Impact Analysis

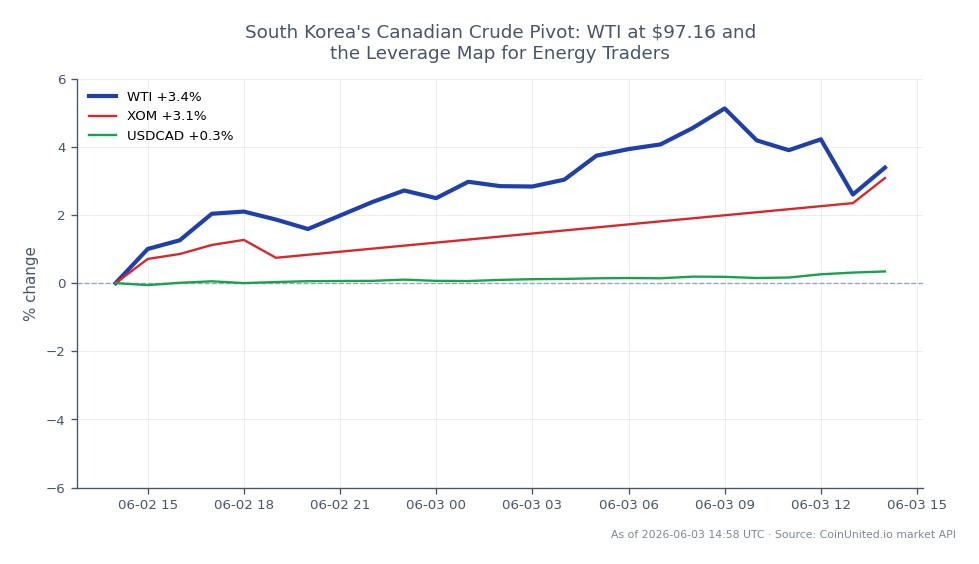

WTI Light Crude Oil is trading at $97.16 (+1.95%), with a 24h range of $95.48–$98.75. This event is a medium-term structural bullish signal for Canadian differentials and a mild relative headwind for WTI's premium to Canadian grades — but short-term WTI itself trades on supply/demand balances, not bilateral trade agreements.

Worked Example — 50x Long WTI CFD: A trader opening a 50x long WTI CFD at $97.16 controls $4,858 of exposure per $100 margin. Each $1.00 move in WTI = ~1.03% P&L on the position. If WTI tests the 24h high at $98.75, that's a +$1.59 move, generating ~+1.6% on the underlying or +82% on 50x margin. Conversely, a pullback to the 24h low of $95.48 produces a -86% margin drawdown — near-liquidation territory at 50x.

At 100x leverage, the $95.48 low would breach a typical liquidation threshold for a position opened at $97.16. The key risk here is that this story is medium-term bullish on Canadian differentials but provides no immediate catalyst for WTI spot prices to break higher — news-driven long entries at current levels carry asymmetric downside if WTI mean-reverts. Monitor open interest on CoinUnited.io for confirmation of directional conviction before sizing up.

Cross-Market Impact

USD/CAD: Stronger Pacific hydrocarbon export diversification is structurally CAD-positive. As reported in the research, TMX's first year saw Canadian non-U.S. exports rise ~60% to ~183,000 bpd. Sustained Korean offtake — particularly at 16M bbl/year scale — improves Canada's trade balance and reduces CAD's historical sensitivity to U.S. demand shocks. Watch USD/CAD for softening on confirmed term-contract announcements.

Energy Majors: Exxon Mobil and Chevron face indirect competition as Korean refiners structurally divert demand away from U.S. Gulf Coast barrels. This could redirect U.S. crude into European markets, subtly compressing Brent-WTI spreads. Refer to our Brent crude trading guide for spread mechanics.

Gold/Commodities: The Korea-Canada corridor reduces Korea's Hormuz Strait exposure. In a Middle East escalation scenario, this supply-security premium diverges — Canadian route barrels hold value while Middle Eastern-dependent importers face a cost shock, supporting gold as an inflation hedge. This aligns with the cross-sector liquidity alliance wave theme.

Natural Gas / LNG: Korea's LNG demand is structurally declining per the research, but portfolio diversification toward Canadian LNG (targeting 56 mtpa export capacity) pressures JKM–Henry Hub spreads medium-term. Watch natural gas for any term-deal confirmation catalysts.

Trading Considerations

WTI's current $97.16 print sits mid-range between the 24h low ($95.48) and high ($98.75). The Korea-Canada story provides no immediate supply-disruption catalyst to drive WTI meaningfully above $98.75 in the short term — it's a demand-reallocation story, not a supply shock. Key levels to watch: $95.48 as near-term support (24h low), $98.75 as resistance (24h high). A sustained break above $98.75 on volume would validate broader energy risk-on sentiment.

The asymmetric trade here sits in Canadian differential instruments and CAD pairs on confirmed volume scale-up announcements, rather than directional WTI spot. Traders with access to energy equity CFDs should monitor HD Hyundai Oilbank parent exposure and Canadian integrated producers for margin expansion catalysts.

Trade WTI Light Crude Oil on CoinUnited.io

Trade WTI with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

The Korea-Canada deal is a demand-reallocation story, not a supply shock — it provides no immediate catalyst for WTI to break above the $98.75 24h high. High-leverage WTI longs (100x+) opened at $97.16 face liquidation near $95.48, so position sizing must account for mean-reversion risk before any structural repricing materializes.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.