Quick Links

Morgan Stanley Cuts Shake Shack Price Target as Guidance Misses Weigh on Growth Thesis

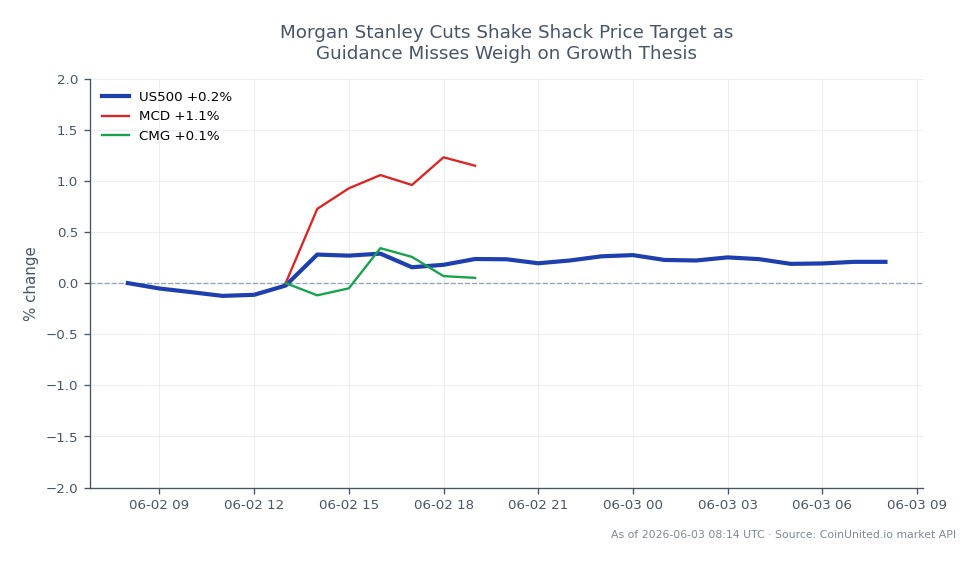

Data Snapshot

Key Takeaways

- •Morgan Stanley reduced its SHAK price target by ~9% to $115 from $126, citing guidance disappointment while maintaining Overweight — a signal of reduced conviction, not a full reversal.

- •DA Davidson's concurrent target cut on margin miss suggests this is a multi-broker reassessment, not a lone-wolf call.

- •SHAK's high-multiple, high-beta profile amplifies downside risk when guidance misses: premium fast-casual names de-rate faster than defensive QSR peers.

- •Peer read-through is limited but watch Chipotle for sympathy moves; McDonald's may benefit from defensive rotation within restaurants.

- •No macro, FX, or crypto implications — this is a single-name, micro-level equity event with sector-level sentiment relevance.

Morgan Stanley has lowered its price target on Shake Shack Inc. (NYSE: SHAK) to $115 from $126, maintaining an Overweight rating while signaling reduced confidence in the company's forward earnings tr

Event Analysis

Morgan Stanley has lowered its price target on Shake Shack Inc. (NYSE: SHAK) to $115 from $126, maintaining an Overweight rating while signaling reduced confidence in the company's forward earnings trajectory. According to MarketScreener, the revision reflects cautious commentary tied to guidance disappointments — a pattern echoed across the Street, with DA Davidson also cutting its target on SHAK citing a margin miss. The ~9% reduction in Morgan Stanley's target is meaningful even without a formal rating downgrade: when a Tier-1 broker lowers assumptions while keeping a bullish label, it typically signals that the bull case has narrowed, not strengthened.

What makes this notable is the broader analyst reassessment underway. According to StockAnalysis and Benzinga, the consensus rating on SHAK has drifted toward Hold, with a 12-month average target in the $113–$119 range. Shake Shack trades at premium multiples relative to mature quick-service restaurant peers — a valuation that depends heavily on sustained same-store sales growth and margin expansion. When guidance misses that narrative, earnings miss revenue shock dynamics tend to hit high-multiple names disproportionately hard.

This is part of a broader theme in the fast-casual space: labor costs, food inflation, and occupancy pressures are compressing restaurant-level margins across the sector. Fox Business has previously documented SHAK sliding more than 10% on negative Morgan Stanley commentary. The current revision, combined with peer-level caution, suggests the Street is recalibrating expectations for the premium burger concept's ability to sustain its growth premium. For traders who understand how to trade earnings misses, this type of coordinated downward revision is a well-defined setup.

What This Means for Traders

The immediate trading implication is directional pressure on SHAK equity. A 9% target cut tied explicitly to guidance disappointment — compounded by DA Davidson's margin-miss commentary — creates a negative sentiment overhang. Fast-money funds and systematic strategies that respond to analyst sentiment shifts may amplify near-term downside, particularly given SHAK's high-beta profile in the consumer discretionary space. Traders should monitor whether the stock finds support near prior technical levels or whether selling pressure accelerates on any further guidance-related headlines.

The sector read-through is more muted but worth watching. Chipotle Mexican Grill and other premium fast-casual names could face sympathy pressure if the market interprets SHAK's guidance miss as a consumer demand signal rather than a company-specific issue. McDonald's Corporation, as a more defensive value-oriented QSR, may actually benefit from a risk rotation within the restaurant space. The S&P 500 Index impact is negligible given SHAK's mid-cap size. For a deeper framework on navigating these situations, see our guide on earnings miss recovery plays.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

According to MarketScreener, Morgan Stanley cut its price target to $115 from $126 but maintained its Overweight rating — so no formal rating downgrade. However, the target reduction and cautious guidance commentary are still price-negative signals.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.