Quick Links

TD Cowen Lifts MasTec Target as $1.65B Superior Group Acquisition Reshapes Growth Outlook

Data Snapshot

Key Takeaways

- •TD Cowen lifted MasTec's price target to $445 from $320, maintaining Buy; consensus average sits near $465–$467 across multiple firms.

- •MasTec's $1.65B Superior Group acquisition adds data-center exposure and is seen as accretive to revenue, EBITDA, EPS, and cash flow.

- •Record backlog of $20.3 billion provides multi-year revenue visibility, the key metric driving analyst confidence in multiple expansion.

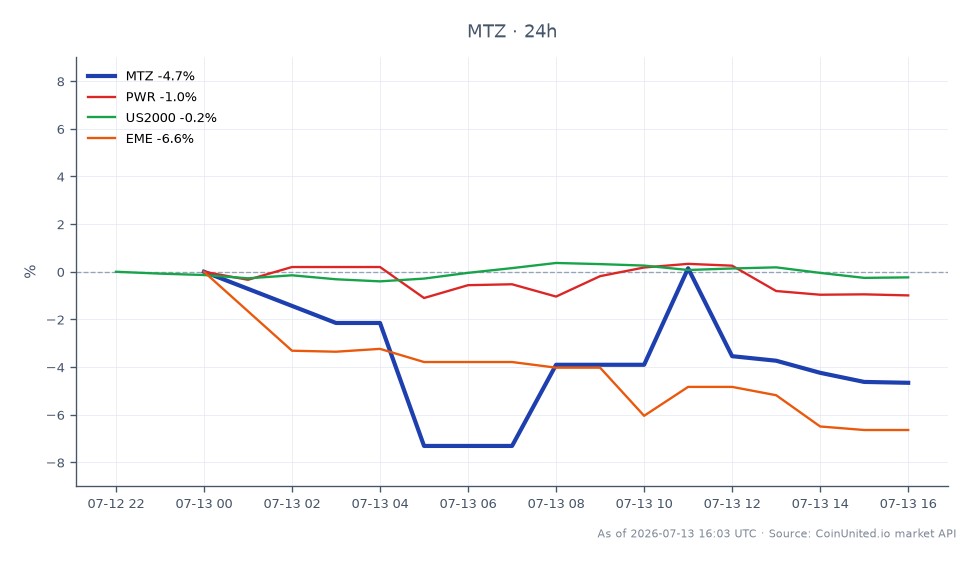

- •MTZ trades at $365.10 — a material discount to the $440–$493 analyst target range — with a 4.41% intraday pullback creating a potential entry window pending confirmation.

- •Sector peers Quanta Services (PWR) and EMCOR Group (EME) may reprice in sympathy as MasTec's backlog signals strong end-market demand.

TD Cowen raised its price target on MasTec, Inc. (NYSE: MTZ) and maintained a Buy rating, according to Investing.com, citing backlog growth and acquisition-driven expansion. While the headline referen

Event Analysis

TD Cowen raised its price target on MasTec, Inc. (NYSE: MTZ) and maintained a Buy rating, according to Investing.com, citing backlog growth and acquisition-driven expansion. While the headline referenced a $470 target, verified search data places TD Cowen's revised target at $445 from $320 — still a substantial 39% lift. The broader analyst community has aligned around similar conviction: Jefferies sits at $493, Clear Street at $440, and the consensus average clusters near $465–$467, per Fintel and Stock Analysis data.

The core catalyst is MasTec's acquisition of The Superior Group, which is being interpreted as immediately accretive to revenue, EBITDA, EPS, and operating cash flow. Superior Group brings deep data-center exposure — a strategically significant detail given the AI infrastructure buildout driving capital allocation across the utility, telecom, and power transmission sectors. This isn't a routine tuck-in; it expands MasTec's addressable market into one of the highest-growth verticals in industrial services.

What makes this moment distinct from typical analyst upgrades is the combination of scale and timing. MasTec reported a record backlog of $20.3 billion, according to company filings, providing revenue visibility that underpins multiple expansion. In a market where infrastructure spending is being pulled forward by AI power demand and grid modernization, MasTec is positioning as a direct pick-and-shovel beneficiary — and analyst targets are catching up to that narrative. This fits squarely within the broader M&A Acquisition Wave reshaping the industrials sector, and specifically the cross-sector acquisition repricing dynamic seen across infrastructure peers.

What This Means for Traders

The primary tradeable event is MTZ itself. Current live price is $365.10 (24h range: $352.30–$384.38, down 4.41%), meaning the stock is trading at a significant discount to even the most conservative analyst target of $440. That gap represents a potential re-rating runway, though it also reflects near-term execution risk from integrating a large acquisition. Traders should watch for post-announcement price confirmation — the intraday pullback may reflect profit-taking or broader market risk-off rather than fundamental deterioration.

Sector read-through is meaningful. Peers like Quanta Services, Inc. (PWR) and EMCOR Group, Inc. (EME) operate in overlapping end-markets — utility construction, electrical contracting, and data-center infrastructure — and may reprice in sympathy if investors treat MasTec's backlog growth as a demand signal for the whole sector. For a broader market lens, the S&P 500 Index and Russell 2000 Index exposures matter less here; this is a stock-specific and sector-specific story. Traders interested in the acquisition dynamics driving industrial valuations can explore our guide on acquisition-driven stock moves.

Trade MasTec, Inc. on CoinUnited.io

Trade MTZ with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

Analyst target raises are forward-looking and don't prevent near-term selling pressure from profit-taking or broader market risk-off. The gap between current price ($365) and analyst targets ($440–$493) represents the market's pending verification of acquisition integration and backlog execution.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.

">%0D%0A <path d="m65.883 9.018.032 5.181h-1.223c-.773-3.733-2.671-5.73-5.797-5.73-4.441 0-6.5 4.442-6.5 9.913 0 5.985 2.38 10.588 6.79 10.588 3.024 0 5.084-1.898 6.211-6.597h1.287l-.482 6.05a13.606 13.606 0 0 1-7.434 1.93c-7.016 0-11.36-4.409-11.36-11.071 0-7.467 4.989-12.166 11.36-12.166a12.961 12.961 0 0 1 7.112 1.899M68.714 21.89c0-5.47 3.572-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.573 9.205-8.367 9.205a7.908 7.908 0 0 1-8.271-8.464zm11.876.354c0-4.762-1.095-8.406-3.669-8.406-2.38 0-3.478 2.703-3.478 6.92 0 4.762 1.126 8.431 3.701 8.431 2.382 0 3.444-2.735 3.444-6.956M93.236 27.555c0 1.126.515 1.318 2.03 1.416v1.062h-8.497V28.97c1.514-.097 2.03-.29 2.03-1.415V16.16l-1.93-1.126v-.611l5.663-1.77h.709l-.005 14.9zM88.345 8.18a2.625 2.625 0 0 1 5.246 0 2.625 2.625 0 0 1-5.246 0zM109.007 18.157c0-1.867-.709-2.8-2.479-2.8a6.474 6.474 0 0 0-3.604 1.319v10.877c0 1.126.482 1.319 1.962 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.93-1.126v-.612l5.76-1.77h.741l-.129 3.154a7.735 7.735 0 0 1 5.954-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.995 1.416v1.062h-8.432V28.97c1.48-.097 1.963-.29 1.963-1.416v-9.396zM123.52 21.851c0 3.927 1.706 6.308 5.247 6.308 3.54 0 5.985-1.867 5.985-6.5V10.82c0-1.74-.419-2.03-3.058-2.253V7.442h7.37v1.126c-2.252.258-2.574.515-2.574 2.253v11.425c0 5.535-3.797 8.116-8.561 8.116-5.697 0-9.108-2.64-9.108-8.174v-11.4c0-1.77-.321-1.965-2.574-2.221V7.44h9.849v1.126c-2.253.258-2.574.45-2.574 2.22l-.002 11.064zM152.26 18.157c0-1.867-.707-2.8-2.478-2.8a6.484 6.484 0 0 0-3.605 1.319v10.877c0 1.126.483 1.319 1.964 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.931-1.126v-.612l5.761-1.77h.74l-.129 3.154a7.731 7.731 0 0 1 5.953-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.996 1.416v1.062h-8.432V28.97c1.479-.097 1.962-.29 1.962-1.416v-9.396zM166.259 27.555c0 1.126.515 1.318 2.029 1.416v1.062h-8.496V28.97c1.512-.097 2.029-.29 2.029-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.709l-.003 14.9zM161.368 8.18a2.62 2.62 0 0 1 2.622-2.518 2.625 2.625 0 0 1 2.623 2.518 2.626 2.626 0 0 1-4.441 1.786 2.62 2.62 0 0 1-.804-1.786zM175.33 12.976h4.183v1.48h-4.183v10.652c0 1.964.741 2.8 2.253 2.8a3.755 3.755 0 0 0 2.414-.901l.387.58a5.65 5.65 0 0 1-4.956 2.768c-2.64 0-4.57-1.384-4.57-4.989v-10.91h-1.996v-.741a13.265 13.265 0 0 0 5.508-4.928h.965l-.005 4.189zM195.514 19.38v.741h-10.492c-.129 4.506 2.189 7.177 5.342 7.177a5.427 5.427 0 0 0 4.796-2.609l.515.29a6.75 6.75 0 0 1-6.888 5.374c-4.665 0-7.787-3.443-7.787-8.406 0-5.507 3.539-9.3 7.948-9.3 4.313 0 6.566 2.864 6.566 6.726m-10.427-.45h6.437c0-3.025-.805-5.085-2.899-5.085-2.125 0-3.283 2.125-3.541 5.084M207.001 7.054v-.676l5.696-1.545h.707v21.788c0 1.094.064 1.45 1.287 1.545l.805.064v.965l-5.857 1.16h-.838l.129-2.993a6.145 6.145 0 0 1-5.181 2.993c-3.895 0-6.5-3.154-6.5-8.046 0-6.087 3.604-9.59 8.206-9.59a5.117 5.117 0 0 1 3.478 1.126V8.048l-1.932-.994zm-5.342 13.709c0 3.926 1.609 6.855 4.538 6.855a3.901 3.901 0 0 0 2.736-1.03v-8.496c0-2.51-1.062-3.99-2.993-3.99-2.703 0-4.28 2.64-4.28 6.667M219.683 24.754a2.796 2.796 0 0 1 2.587 1.729 2.8 2.8 0 1 1-5.387 1.072 2.75 2.75 0 0 1 1.721-2.6 2.753 2.753 0 0 1 1.079-.2zM230.592 27.555c0 1.126.516 1.318 2.029 1.416v1.062h-8.501V28.97c1.512-.097 2.03-.29 2.03-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.708l.002 14.9zM225.7 8.18a2.626 2.626 0 0 1 4.441-1.787c.488.47.777 1.11.804 1.787a2.625 2.625 0 0 1-5.245 0zM233.842 21.89c0-5.47 3.573-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.572 9.205-8.366 9.205a7.904 7.904 0 0 1-7.809-5.179 7.904 7.904 0 0 1-.463-3.285zm11.876.354c0-4.762-1.094-8.406-3.669-8.406-2.382 0-3.479 2.703-3.479 6.92 0 4.762 1.126 8.431 3.7 8.431 2.382 0 3.444-2.735 3.444-6.956M18.386.684a17.469 17.469 0 1 0 0 34.937 17.469 17.469 0 0 0 0-34.937zm0 31.74a14.277 14.277 0 1 1 0-28.554 14.277 14.277 0 0 1 0 28.554z" fill="%23fff"/>%0D%0A <path d="M18.393 36.019a17.868 17.868 0 1 1 17.86-17.868 17.887 17.887 0 0 1-17.86 17.868zm0-34.938a17.07 17.07 0 1 0 17.063 17.07 17.089 17.089 0 0 0-17.063-17.07zm0 31.74a14.675 14.675 0 1 1 10.366-4.297 14.691 14.691 0 0 1-10.373 4.303m0-28.552a13.877 13.877 0 1 0 13.879 13.878A13.893 13.893 0 0 0 18.386 4.275z" fill="%23fff"/>%0D%0A <path d="M17.42 8.46a8.46 8.46 0 1 1-16.923 0 8.46 8.46 0 0 1 16.924 0" fill="%23E48A22"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="sy6kzo59ya">%0D%0A <path fill="%23fff" transform="translate(.5)" d="M0 0h250v36.019H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

"><path fill="%23fff" transform="scale(1.9886)" d="M27.72,2.61a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-30.14,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-32.16,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-34.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-40.2,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-58.29,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-62.32,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m30.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m22.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m34.16,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m18.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.27,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-56.29,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-48.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2"/><path d="M123.088,117.106a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M123.088,133.085a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M91.095,145.087a1.987,1.987,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989,2.01,2.01,0,0,1,1.989-1.988zM107.109,145.087a1.988,1.988,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989c-.035-1.081.872-1.988,1.989-1.988zM115.098,145.087a1.987,1.987,0,1,1,0,3.977,1.987,1.987,0,0,1-1.988-1.989c-.035-1.081.872-1.988,1.988-1.988zM123.088,145.087a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M151.069,149.064a1.988,1.988,0,1,1-1.989,1.989c-.035-1.082.872-1.989,1.989-1.989zM25.271,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491c0-1.575,1.277-2.852,2.83-2.852h6.492a2.852,2.852,0,0,1,2.852,2.852v6.49h.021z" fill="%23fff"/><path d="M33.38,30.568a2.852,2.852,0,0,1-2.852,2.851H7.798a2.852,2.852,0,0,1-2.851-2.851V7.817a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.75h-.021zM29.315,11.86a2.852,2.852,0,0,0-2.852-2.852H11.842A2.852,2.852,0,0,0,8.99,11.86v14.642a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852V11.86h-.021zM25.271,142.338a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491a2.852,2.852,0,0,1,2.852-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.491z" fill="%23fff"/><path d="M33.38,150.468a2.852,2.852,0,0,1-2.852,2.852H7.798a2.852,2.852,0,0,1-2.851-2.852v-22.751a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.751h-.021zm-4.065-18.686a2.852,2.852,0,0,0-2.852-2.852H11.842a2.852,2.852,0,0,0-2.852,2.852v14.621a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852v-14.621h-.021zM145.171,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.491a2.851,2.851,0,0,1-2.851-2.852v-6.491a2.851,2.851,0,0,1,2.851-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.49z" fill="%23fff"/><path d="M153.301,30.568a2.852,2.852,0,0,1-2.852,2.851h-22.75a2.852,2.852,0,0,1-2.852-2.851V7.817a2.852,2.852,0,0,1,2.852-2.852h22.75a2.852,2.852,0,0,1,2.852,2.852v22.75zm-4.065-18.707a2.852,2.852,0,0,0-2.852-2.852h-14.621a2.852,2.852,0,0,0-2.851,2.852v14.642a2.852,2.852,0,0,0,2.851,2.852h14.621a2.852,2.852,0,0,0,2.852-2.852V11.86zM78.535,62.051c-9.176,0-16.607,7.431-16.607,16.607,0,9.176,7.431,16.607,16.607,16.607,9.176,0,16.607-7.431,16.607-16.607,0-9.176-7.431-16.607-16.607-16.607zm0,30.214c-7.501,0-13.572-6.07-13.572-13.572,0-7.501,6.07-13.572,13.572-13.572,7.501,0,13.572,6.07,13.572,13.572,0,7.501-6.071,13.572-13.572,13.572z" fill="%23fff"/><path d="M78.535,95.649c-9.385,0-16.991-7.64-16.991-16.99,0-9.386,7.64-16.992,16.99-16.992,9.386,0,16.992,7.64,16.992,16.991,0,9.35-7.64,16.991-16.991,16.991zm0-33.214c-8.966,0-16.258,7.292-16.258,16.258s7.291,16.258,16.258,16.258c8.966,0,16.258-7.291,16.258-16.258-.035-8.966-7.292-16.258-16.258-16.258zm0,30.214c-7.71,0-13.956-6.28-13.956-13.956,0-7.71,6.28-13.956,13.956-13.956,7.71,0,13.956,6.28,13.956,13.956,0,7.676-6.28,13.956-13.956,13.956zm0-27.179c-7.292,0-13.223,5.931-13.223,13.223,0,7.292,5.931,13.223,13.223,13.223,7.292,0,13.223-5.931,13.223-13.223-.035-7.292-5.966-13.223-13.223-13.223z" fill="%23fff"/><path d="M69.569,77.507a8.06,8.06,0,1,0,0-16.119,8.06,8.06,0,0,0,0,16.119z" fill="%23E48A22"/></g><defs><clipPath id="arusb4546a"><path fill="%23fff" transform="translate(0 .019)" d="M0,0h157v157H0z"/></clipPath></defs></svg>)

">%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23fff"/>%0D%0A <path d="M106.646 32.584H4.356A3.857 3.857 0 0 1 .5 28.741V3.867A3.853 3.853 0 0 1 4.355.02h102.29a3.86 3.86 0 0 1 3.855 3.848V28.74a3.853 3.853 0 0 1-3.854 3.845z" fill="%23A6A6A6"/>%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23000"/>%0D%0A <path d="M25.063 16.13a4.717 4.717 0 0 1 2.25-3.961 4.84 4.84 0 0 0-3.812-2.059c-1.603-.168-3.159.959-3.976.959-.833 0-2.09-.942-3.447-.915a5.079 5.079 0 0 0-4.271 2.603c-1.848 3.195-.47 7.89 1.3 10.472.886 1.265 1.92 2.679 3.274 2.626 1.325-.052 1.82-.84 3.417-.84 1.584 0 2.05.84 3.43.81 1.42-.021 2.317-1.27 3.171-2.546a10.434 10.434 0 0 0 1.452-2.952 4.572 4.572 0 0 1-2.786-4.197h-.003zm-2.61-7.718a4.643 4.643 0 0 0 1.065-3.33 4.74 4.74 0 0 0-3.064 1.583 4.42 4.42 0 0 0-1.092 3.207 3.917 3.917 0 0 0 3.091-1.46zM44.25 25.674H42.4l-1.015-3.183H37.86l-.966 3.183H35.09l3.493-10.838h2.156l3.509 10.838h.002zm-3.17-4.517-.918-2.83c-.097-.29-.28-.97-.547-2.042h-.033c-.108.461-.28 1.142-.515 2.042l-.902 2.83h2.914zm12.137.515a4.422 4.422 0 0 1-1.085 3.152 3.178 3.178 0 0 1-2.41 1.03 2.415 2.415 0 0 1-2.235-1.109v4.1H45.75v-8.417c0-.835-.021-1.691-.064-2.569h1.529l.097 1.239h.032a3.09 3.09 0 0 1 2.398-1.395 3.095 3.095 0 0 1 2.552 1.088c.645.817.973 1.84.925 2.88l-.001.001zm-1.77.064a3.22 3.22 0 0 0-.516-1.882 1.781 1.781 0 0 0-1.513-.771c-.427 0-.84.15-1.166.426-.349.284-.59.678-.684 1.118a2.26 2.26 0 0 0-.08.528v1.302a2.09 2.09 0 0 0 .525 1.44 1.737 1.737 0 0 0 1.36.587 1.783 1.783 0 0 0 1.529-.755c.389-.59.58-1.29.544-1.995v.002zm10.768-.064a4.422 4.422 0 0 1-1.084 3.152 3.182 3.182 0 0 1-2.413 1.03 2.415 2.415 0 0 1-2.233-1.109v4.1h-1.739v-8.417c0-.835-.021-1.691-.065-2.569h1.53l.096 1.239h.033a3.092 3.092 0 0 1 3.803-1.153c.443.189.836.478 1.148.846.645.817.973 1.84.924 2.88v.001zm-1.771.064a3.22 3.22 0 0 0-.517-1.882 1.778 1.778 0 0 0-1.511-.771c-.427 0-.841.15-1.168.426-.349.284-.59.678-.683 1.118-.048.172-.075.35-.082.528v1.302a2.097 2.097 0 0 0 .523 1.44 1.74 1.74 0 0 0 1.361.587 1.781 1.781 0 0 0 1.53-.755c.39-.59.581-1.289.547-1.995v.002zm11.831.9a2.893 2.893 0 0 1-.964 2.251 4.278 4.278 0 0 1-2.956.949 5.163 5.163 0 0 1-2.809-.675l.402-1.447a4.84 4.84 0 0 0 2.511.676 2.371 2.371 0 0 0 1.53-.442 1.444 1.444 0 0 0 .548-1.181 1.511 1.511 0 0 0-.452-1.11 4.188 4.188 0 0 0-1.496-.836c-1.9-.707-2.85-1.742-2.85-3.104a2.737 2.737 0 0 1 1.006-2.187 3.981 3.981 0 0 1 2.664-.852 5.27 5.27 0 0 1 2.463.515l-.437 1.415a4.31 4.31 0 0 0-2.084-.498 2.121 2.121 0 0 0-1.438.45 1.289 1.289 0 0 0-.437.982 1.327 1.327 0 0 0 .5 1.061 5.63 5.63 0 0 0 1.577.836c.78.274 1.485.725 2.06 1.318.45.521.686 1.192.663 1.88v-.002zm5.762-3.472H76.12v3.794c0 .965.338 1.447 1.014 1.447.26.006.52-.021.773-.08l.048 1.318a3.942 3.942 0 0 1-1.352.192 2.085 2.085 0 0 1-1.61-.63 3.077 3.077 0 0 1-.578-2.107v-3.94h-1.141v-1.302h1.141v-1.43l1.707-.515v1.943h1.915l-.001 1.31zm8.627 2.54a4.284 4.284 0 0 1-1.03 2.959 3.674 3.674 0 0 1-2.865 1.19 3.504 3.504 0 0 1-2.746-1.14 4.154 4.154 0 0 1-1.022-2.879 4.249 4.249 0 0 1 1.054-2.974 3.655 3.655 0 0 1 2.842-1.155 3.577 3.577 0 0 1 2.768 1.142 4.1 4.1 0 0 1 1 2.856v.001zm-1.802.04a3.496 3.496 0 0 0-.465-1.843 1.72 1.72 0 0 0-1.562-.931 1.746 1.746 0 0 0-1.594.93 3.554 3.554 0 0 0-.466 1.877 3.485 3.485 0 0 0 .466 1.844 1.782 1.782 0 0 0 3.141-.015 3.51 3.51 0 0 0 .48-1.863v.001zm7.454-2.356a3.03 3.03 0 0 0-.547-.047 1.641 1.641 0 0 0-1.42.692 2.605 2.605 0 0 0-.434 1.543v4.1H88.18v-5.355c0-.82-.017-1.64-.052-2.46h1.514l.063 1.495h.049c.164-.488.466-.918.868-1.239.363-.271.804-.419 1.257-.42.145 0 .29.01.435.032v1.656l.002.003zm7.774 2.011c.004.264-.017.528-.064.788h-5.214a2.262 2.262 0 0 0 .756 1.77 2.59 2.59 0 0 0 1.707.544c.72.01 1.435-.115 2.11-.368l.272 1.204a6.527 6.527 0 0 1-2.623.483 3.805 3.805 0 0 1-2.86-1.067 3.95 3.95 0 0 1-1.039-2.87 4.473 4.473 0 0 1 .967-2.942 3.331 3.331 0 0 1 2.734-1.253 2.916 2.916 0 0 1 2.56 1.253c.48.728.722 1.586.694 2.456v.002zm-1.658-.45a2.348 2.348 0 0 0-.337-1.335 1.518 1.518 0 0 0-1.384-.725 1.648 1.648 0 0 0-1.381.706c-.297.392-.475.86-.515 1.35h3.62l-.003.004zM37.359 11.005a11.12 11.12 0 0 1-1.25-.063v-5.24c.487-.075.98-.112 1.472-.11 1.994 0 2.912.98 2.912 2.576 0 1.842-1.085 2.837-3.134 2.837zm.292-4.742a3.49 3.49 0 0 0-.688.055v3.984c.192.02.385.028.578.023 1.306 0 2.05-.743 2.05-2.133-.002-1.24-.674-1.929-1.94-1.929zm5.702 4.78a1.832 1.832 0 0 1-1.755-1.225 1.826 1.826 0 0 1-.097-.75 1.87 1.87 0 0 1 1.916-2.031 1.817 1.817 0 0 1 1.851 1.968 1.881 1.881 0 0 1-1.915 2.04v-.002zm.032-3.382c-.617 0-1.012.577-1.012 1.383 0 .79.404 1.365 1.005 1.365.6 0 1.004-.616 1.004-1.383 0-.779-.396-1.363-.996-1.363V7.66zm8.29-.545-1.203 3.84h-.784L49.19 9.29a12.619 12.619 0 0 1-.309-1.24h-.016c-.07.42-.174.835-.308 1.24l-.53 1.668h-.792l-1.132-3.841h.878l.435 1.826c.103.435.19.845.263 1.232h.017c.062-.323.165-.727.315-1.225l.546-1.833h.696l.523 1.795c.126.435.229.861.309 1.264h.023c.062-.426.15-.848.262-1.264l.468-1.795h.84-.004zm4.426 3.84h-.854V8.75c0-.679-.263-1.02-.776-1.02a.888.888 0 0 0-.854.942v2.284h-.854v-2.74c0-.34-.009-.705-.032-1.1h.751l.04.593h.024a1.38 1.38 0 0 1 1.219-.67c.806 0 1.336.616 1.336 1.619v2.3-.002zm2.356 0h-.855v-5.6h.855v5.6zm3.115.088a1.832 1.832 0 0 1-1.851-1.976 1.87 1.87 0 0 1 1.914-2.031 1.816 1.816 0 0 1 1.851 1.968 1.88 1.88 0 0 1-1.914 2.04v-.001zm.032-3.383c-.617 0-1.012.578-1.012 1.383 0 .79.404 1.366 1.003 1.366.6 0 1.005-.617 1.005-1.384 0-.779-.394-1.363-.998-1.363l.002-.002zm5.252 3.296-.063-.442h-.022a1.314 1.314 0 0 1-1.125.53 1.118 1.118 0 0 1-1.178-1.131c0-.946.823-1.438 2.247-1.438v-.071c0-.506-.268-.76-.798-.76a1.8 1.8 0 0 0-1.004.286l-.174-.561a2.46 2.46 0 0 1 1.32-.332c1.005 0 1.511.529 1.511 1.588v1.415a5.79 5.79 0 0 0 .056.917l-.77-.001zm-.118-1.913c-.949 0-1.425.23-1.425.774a.543.543 0 0 0 .586.6.818.818 0 0 0 .841-.78l-.002-.594zm4.982 1.913-.04-.617h-.024a1.288 1.288 0 0 1-1.234.704c-.927 0-1.614-.814-1.614-1.96 0-1.201.712-2.049 1.683-2.049a1.157 1.157 0 0 1 1.084.523h.017V5.35h.856v4.57c0 .372.009.72.031 1.036h-.76zm-.126-2.259a.93.93 0 0 0-.9-.998c-.631 0-1.021.561-1.021 1.351 0 .775.402 1.305 1.003 1.305a.96.96 0 0 0 .914-1.019v-.639h.004zm6.277 2.347a1.831 1.831 0 0 1-1.85-1.975 1.87 1.87 0 0 1 1.913-2.031 1.816 1.816 0 0 1 1.852 1.968 1.88 1.88 0 0 1-1.916 2.038zm.031-3.382c-.616 0-1.011.577-1.011 1.383 0 .79.403 1.365 1.003 1.365.6 0 1.005-.616 1.005-1.383 0-.782-.394-1.366-1-1.366h.003zm6.478 3.296h-.857V8.753c0-.68-.263-1.02-.775-1.02a.888.888 0 0 0-.854.94v2.285h-.855V8.215c0-.34-.009-.704-.032-1.099h.752l.04.593h.023a1.38 1.38 0 0 1 1.218-.671c.807 0 1.338.616 1.338 1.62l.002 2.3zm5.749-3.2h-.94v1.864c0 .473.165.712.497.712.128 0 .255-.013.38-.04l.023.648c-.213.07-.438.103-.663.095-.673 0-1.076-.372-1.076-1.344V7.758h-.56v-.64h.56v-.704l.841-.254v.956h.94v.641l-.002.001zm4.52 3.2h-.853v-2.19c0-.687-.26-1.035-.775-1.035a.838.838 0 0 0-.856.909v2.315h-.851V5.355h.854v2.307h.017a1.296 1.296 0 0 1 1.156-.624c.814 0 1.312.63 1.312 1.636l-.003 2.285zm4.635-1.715H96.72a1.102 1.102 0 0 0 1.21 1.137c.353.004.704-.058 1.035-.181l.133.593a3.212 3.212 0 0 1-1.29.237 1.789 1.789 0 0 1-1.913-1.936c0-1.178.728-2.063 1.818-2.063.982 0 1.598.728 1.598 1.826.006.13-.004.26-.03.387h.003zm-.783-.609c0-.593-.3-1.011-.846-1.011a1.014 1.014 0 0 0-.934 1.011h1.78z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="uavr3vx5ga">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

">%0D%0A <path d="M106.426 32.584H4.574a4.037 4.037 0 0 1-3.775-2.507 4.029 4.029 0 0 1-.3-1.564V4.09A4.028 4.028 0 0 1 3.01.318a4.038 4.038 0 0 1 1.565-.3h101.852a4.039 4.039 0 0 1 3.774 2.507c.203.496.305 1.028.3 1.564v24.424a4.032 4.032 0 0 1-4.074 4.071z" fill="%23000"/>%0D%0A <path d="M106.426.67a3.445 3.445 0 0 1 3.422 3.42v24.424a3.444 3.444 0 0 1-3.422 3.42H4.574a3.444 3.444 0 0 1-3.422-3.42V4.089A3.438 3.438 0 0 1 4.574.67h101.852zm0-.651H4.574A4.088 4.088 0 0 0 .5 4.089v24.425a4.029 4.029 0 0 0 2.508 3.771 4.039 4.039 0 0 0 1.566.3h101.852a4.04 4.04 0 0 0 2.892-1.181 4.023 4.023 0 0 0 1.182-2.89V4.089a4.082 4.082 0 0 0-4.074-4.07z" fill="%23A6A6A6"/>%0D%0A <path d="M39.122 8.323a2.216 2.216 0 0 1-.57 1.628 2.558 2.558 0 0 1-3.585 0 2.393 2.393 0 0 1-.734-1.794 2.394 2.394 0 0 1 .734-1.785 2.395 2.395 0 0 1 1.792-.736c.34.004.676.087.978.244.292.122.546.318.736.57l-.407.407a1.52 1.52 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57 1.677 1.677 0 0 0-.573 1.384 1.675 1.675 0 0 0 .57 1.384c.355.336.817.538 1.304.57a1.789 1.789 0 0 0 1.386-.57 1.347 1.347 0 0 0 .407-.976h-1.793v-.652h2.366v.326h-.003zm3.748-2.036h-2.2v1.547h2.038v.57H40.67v1.547h2.2v.651h-2.854V5.718h2.855v.57zm2.69 4.315h-.653V6.287h-1.385v-.57h3.422v.57H45.56v4.315zm3.747 0V5.718h.652v4.884h-.652zm3.423 0h-.652V6.287h-1.385v-.57h3.34v.57h-1.385v4.315h.082zm7.74-.65a2.559 2.559 0 0 1-3.585 0 2.394 2.394 0 0 1-.736-1.792 2.393 2.393 0 0 1 .736-1.791 2.558 2.558 0 0 1 3.586 0 2.395 2.395 0 0 1 .735 1.791 2.391 2.391 0 0 1-.736 1.791zm-3.096-.408c.346.35.812.554 1.304.57a1.623 1.623 0 0 0 1.304-.57c.366-.369.57-.867.57-1.387a1.675 1.675 0 0 0-.57-1.381 1.924 1.924 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57c-.365.367-.57.864-.57 1.381a1.676 1.676 0 0 0 .57 1.387zm4.726 1.058V5.718h.736l2.366 3.826V5.718h.651v4.884h-.657l-2.523-3.989v3.99H62.1z" fill="%23fff" stroke="%23fff" stroke-width=".2" stroke-miterlimit="10"/>%0D%0A <path d="M55.989 17.767a3.43 3.43 0 0 0-3.258 2.149c-.173.43-.256.89-.246 1.352a3.47 3.47 0 0 0 2.159 3.241c.427.175.884.263 1.345.26a3.432 3.432 0 0 0 3.258-2.15c.172-.429.256-.889.245-1.351a3.376 3.376 0 0 0-3.503-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-7.578-5.536a3.431 3.431 0 0 0-3.258 2.149c-.172.43-.256.89-.246 1.352a3.472 3.472 0 0 0 2.16 3.241c.426.175.883.263 1.344.26a3.432 3.432 0 0 0 3.258-2.15c.173-.429.256-.889.246-1.351a3.376 3.376 0 0 0-3.504-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-9.044-4.478v1.466h3.503a3.077 3.077 0 0 1-.815 1.872 3.607 3.607 0 0 1-2.688 1.059 3.796 3.796 0 0 1-3.83-3.908 3.838 3.838 0 0 1 2.347-3.605c.47-.198.973-.301 1.483-.303a4.041 4.041 0 0 1 2.688 1.056l1.06-1.056a5.223 5.223 0 0 0-3.667-1.466 5.49 5.49 0 0 0-5.46 5.373 5.49 5.49 0 0 0 5.46 5.374 4.693 4.693 0 0 0 3.748-1.547 4.9 4.9 0 0 0 1.304-3.42c.017-.3-.01-.6-.082-.892h-5.051v-.003zm36.992 1.14a3.163 3.163 0 0 0-2.933-2.198c-1.793 0-3.26 1.384-3.26 3.5a3.406 3.406 0 0 0 3.423 3.502 3.345 3.345 0 0 0 2.852-1.547l-1.141-.814a1.986 1.986 0 0 1-1.711.976 1.769 1.769 0 0 1-1.711-1.058l4.644-1.954-.163-.407zm-4.726 1.14a1.977 1.977 0 0 1 1.793-2.035 1.441 1.441 0 0 1 1.303.732l-3.096 1.303zm-3.83 3.34h1.549V14.267h-1.548v10.18zm-2.444-5.943a2.682 2.682 0 0 0-1.874-.814 3.502 3.502 0 0 0-3.34 3.501 3.369 3.369 0 0 0 2.048 3.149c.409.174.848.266 1.292.27a2.34 2.34 0 0 0 1.793-.814h.081v.489c0 1.302-.736 2.035-1.874 2.035a1.81 1.81 0 0 1-1.711-1.221l-1.304.57a3.36 3.36 0 0 0 3.096 2.035c1.793 0 3.26-1.058 3.26-3.582v-6.19h-1.467v.572zm-1.792 4.804a2.025 2.025 0 0 1-1.956-2.117 2.02 2.02 0 0 1 1.956-2.117 1.961 1.961 0 0 1 1.874 2.117 1.957 1.957 0 0 1-1.875 2.114v.003zm19.881-9.035h-3.667v10.175h1.548v-3.83h2.119a3.185 3.185 0 0 0 3.087-1.92 3.177 3.177 0 0 0-1.82-4.237 3.185 3.185 0 0 0-1.267-.193v.005zm.082 4.885h-2.2V15.65h2.2a1.788 1.788 0 0 1 1.792 1.71 1.862 1.862 0 0 1-1.793 1.791v.005zm9.37-1.465c-1.14 0-2.282.488-2.689 1.547l1.385.57a1.438 1.438 0 0 1 1.385-.736 1.532 1.532 0 0 1 1.63 1.303v.079a3.236 3.236 0 0 0-1.548-.407c-1.467 0-2.934.814-2.934 2.28a2.386 2.386 0 0 0 2.524 2.279 2.294 2.294 0 0 0 1.955-.977h.082v.817h1.466v-3.908a3.08 3.08 0 0 0-3.259-2.85l.003.003zm-.163 5.617c-.489 0-1.222-.244-1.222-.893 0-.814.896-1.058 1.63-1.058.48.002.954.113 1.385.326a1.895 1.895 0 0 1-1.793 1.62v.005zm8.555-5.373-1.71 4.396H99.5l-1.793-4.396h-1.63l2.69 6.188-1.549 3.419h1.548l4.153-9.607h-1.629.002zm-13.688 6.51h1.548V14.267h-1.548v10.18z" fill="%23fff"/>%0D%0A <path d="M8.974 6.125a1.59 1.59 0 0 0-.326 1.14v17.992a1.61 1.61 0 0 0 .408 1.14l.081.081 10.104-10.095v-.163L8.974 6.125z" fill="url(%23nqixmws78b)"/>%0D%0A <path d="m22.5 19.802-3.34-3.338v-.244l3.34-3.338.081.082 3.99 2.28c1.141.65 1.141 1.709 0 2.36L22.5 19.802z" fill="url(%23euwe5vohvc)"/>%0D%0A <path d="m22.581 19.72-3.422-3.418L8.974 26.477c.408.407.978.407 1.711.082l11.896-6.84z" fill="url(%23wso0uh08dd)"/>%0D%0A <path d="M22.581 12.882 10.685 6.125c-.736-.407-1.303-.326-1.71.081l10.184 10.096 3.422-3.42z" fill="url(%23mrdt54dj1e)"/>%0D%0A <path opacity=".2" d="m22.5 19.64-11.815 6.675a1.334 1.334 0 0 1-1.63 0l-.08.082.08.081a1.333 1.333 0 0 0 1.63 0L22.5 19.64z" fill="%23000"/>%0D%0A <path opacity=".12" d="M8.974 26.316a1.59 1.59 0 0 1-.326-1.14v.081a1.61 1.61 0 0 0 .408 1.14v-.081h-.082zm17.6-8.956L22.5 19.64l.081.08 3.993-2.279a1.355 1.355 0 0 0 .815-1.14c0 .408-.326.733-.815 1.059z" fill="%23000"/>%0D%0A <path opacity=".25" d="m10.685 6.206 15.89 9.037c.488.326.814.651.814 1.059a1.352 1.352 0 0 0-.815-1.14L10.685 6.125c-1.143-.652-2.037-.163-2.037 1.14v.08c0-1.22.894-1.79 2.037-1.139z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <linearGradient id="nqixmws78b" x1="18.265" y1="27.13" x2="2.062" y2="22.737" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2300A0FF"/>%0D%0A <stop offset=".007" stop-color="%2300A1FF"/>%0D%0A <stop offset=".26" stop-color="%2300BEFF"/>%0D%0A <stop offset=".512" stop-color="%2300D2FF"/>%0D%0A <stop offset=".76" stop-color="%2300DFFF"/>%0D%0A <stop offset="1" stop-color="%2300E3FF"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="euwe5vohvc" x1="28.064" y1="17.927" x2="8.353" y2="17.927" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FFE000"/>%0D%0A <stop offset=".409" stop-color="%23FFBD00"/>%0D%0A <stop offset=".775" stop-color="orange"/>%0D%0A <stop offset="1" stop-color="%23FF9C00"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="wso0uh08dd" x1="20.731" y1="16.06" x2="7.736" y2="-5.775" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FF3A44"/>%0D%0A <stop offset="1" stop-color="%23C31162"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="mrdt54dj1e" x1="6.443" y1="34.068" x2="12.205" y2="24.305" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2332A071"/>%0D%0A <stop offset=".069" stop-color="%232DA771"/>%0D%0A <stop offset=".476" stop-color="%2315CF74"/>%0D%0A <stop offset=".801" stop-color="%2306E775"/>%0D%0A <stop offset="1" stop-color="%2300F076"/>%0D%0A </linearGradient>%0D%0A <clipPath id="oefv1zwvza">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)