Quick Links

Yen at 40-Year Low: Carry Trade Blowup Risk and Leverage Flashpoints in USD/JPY

Data Snapshot

Key Takeaways

- •The yen has hit a ~40-year low vs. USD, driven by a wide US–Japan yield spread with Japan's 10Y JGB yield at ~2.67%, per Trading Economics.

- •Leveraged long USD/JPY positions face asymmetric intervention risk — historical MOF actions have produced 300–500 pip reversals; at 100x leverage, a 200-pip reversal equals a 20% margin hit.

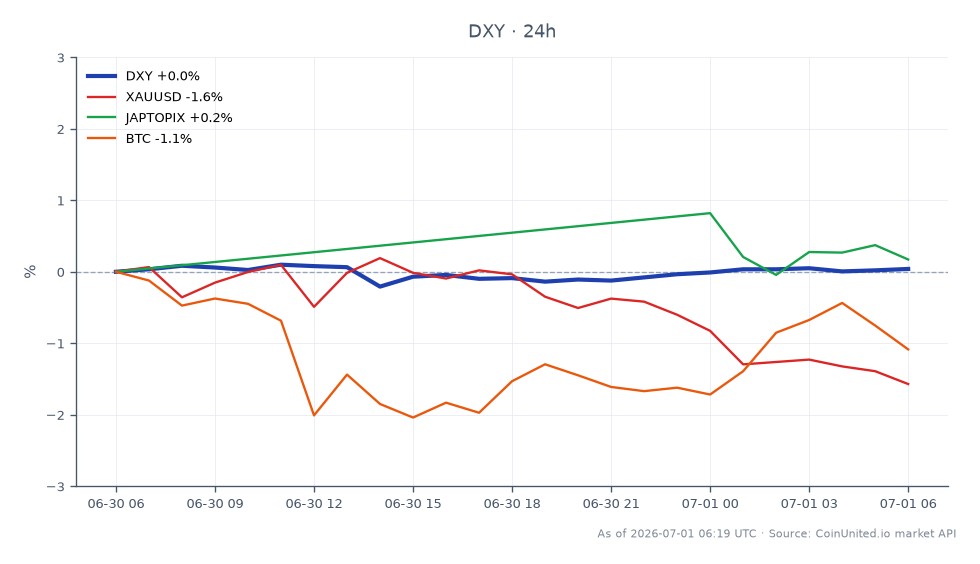

- •DXY is holding at $101.31, near session highs — sustained yen weakness reinforces dollar strength and applies indirect downward pressure on gold (XAU/USD).

- •Japanese equities face a split: yen weakness supports exporters but rising long-end JGB yields compress valuations for domestic and rate-sensitive sectors.

- •A sudden BoJ pivot or MOF intervention could trigger a global carry-trade unwind — watch for cascading risk-off effects in EM FX, high-beta equities, and crypto.

The Japanese yen has fallen to its weakest level against the US dollar in approximately four decades, according to Trading Economics and Yahoo Finance. The move is being driven by a widening US–Japan

Event Summary

The Japanese yen has fallen to its weakest level against the US dollar in approximately four decades, according to Trading Economics and Yahoo Finance. The move is being driven by a widening US–Japan yield differential, with Japan's 10-year government bond yield climbing to around 2.67% while US Treasury yields remain elevated — a spread dynamic that MacroMicro directly correlates with USD/JPY direction. Japan's 40-year JGB yields have simultaneously reached multi-decade highs, signaling structural stress across the entire Japanese rates complex. Market participants are actively speculating about potential Ministry of Finance (MOF) intervention to stem the yen's slide, creating a distinctly two-sided risk environment.

This is not a one-day event. As detailed in our USD/JPY & BoJ Policy Trader's Guide, the yen's trajectory reflects a persistent macro regime: high US yields sustaining carry-trade flows out of JPY and into dollar-denominated assets. Rising Japanese yields simultaneously point to mounting pressure on the Bank of Japan (BoJ) to abandon or modify its yield-curve control framework — a shift that could reverse the yen's slide violently and without much warning.

Leverage Impact Analysis

USD/JPY at a 40-year high is a high-voltage environment for leveraged forex positions. Consider the asymmetric risk profile:

Long USD/JPY (trend-following carry): A trader holding a 100x long USD/JPY CFD on CoinUnited.io benefits from every pip of yen weakness — but faces catastrophic drawdown if MOF intervention hits. Historical Japanese FX interventions (2022) produced 300–500 pip reversals in hours. At 100x leverage, a 200-pip adverse move against a long position equates to a 20% margin hit. Traders should monitor position sizing carefully relative to available margin.

Short USD/JPY (intervention play): Traders anticipating a BoJ policy shift or MOF intervention face the opposite problem — the trend has been brutal for shorts. At 50x leverage, every 100 pips of additional yen weakness produces a 5% margin loss. Tight stop placement above recent highs is essential.

Funding rate watch: The BOJ CPI Shock & Global Carry Unwind theme is directly relevant here. If the BoJ surprises hawkishly, carry unwind can cascade rapidly — impacting not just USD/JPY but also leveraged positions in EM FX, high-yield bonds, and risk assets broadly. Monitor funding rates on CoinUnited.io for positioning signals.

Cross-Market Impact

DXY: Live data shows DXY at $101.31 (+0.16%), near its 24h high of $101.35. A persistently weak yen structurally supports dollar strength, reinforcing the Fed & ECB Policy Divergence Repricing theme. The gold vs. US dollar inverse relationship means continued dollar strength applies pressure to XAU/USD — gold traders should treat yen weakness as a dollar-strength proxy signal.

Japanese Equities: The Nikkei 225 and Japan TOPIX Index face a classic split: yen weakness boosts exporter earnings (autos, industrials, electronics) in JPY terms, but rising JGB yields at the long end compress equity valuations and raise funding costs for domestic sectors. Net: exporters outperform domestics in this regime.

Crypto: Indirect but real. Yen weakness sustains global carry-trade flows into risk assets, providing a liquidity tailwind for Bitcoin and broader crypto. However, a sudden yen reversal (intervention or BoJ pivot) historically triggers a sharp risk-off unwind — the August 2024 carry unwind remains the clearest recent precedent.

EURUSD / GBPUSD: EUR and GBP benefit modestly as the dollar's strength is concentrated against low-yielders like JPY. The Fed & ECB Policy Divergence dynamic keeps EUR/USD under structural pressure regardless.

Trading Considerations

The primary risk in USD/JPY at 40-year highs is not the trend — it is the intervention tail. Japanese authorities have historically acted without warning when moves are described as "excessive" or "one-sided." Leveraged long positions should treat current levels as high-intervention-risk territory, not a free continuation trade. Reducing position size relative to normal is prudent risk management at these extremes.

For the broader Fed Macro Policy Crossroads context: the US–Japan yield spread remains the primary driver of USD/JPY. Watch US 10Y Treasury moves as the lead indicator — any softening in US yields (soft data, Fed dovish pivot) would be the most likely non-intervention catalyst for yen strength. Confirm open interest trends on CoinUnited.io before adding directional exposure.

Trade U.S. Dollar Currency Index on CoinUnited.io

Trade DXY with up to 2000xx leverage → | Create Free Account

Frequently Asked Questions

At high leverage levels (50x–100x), even a 100–200 pip adverse move can liquidate a significant portion of margin — at 100x, a 200-pip reversal from intervention represents a ~20% margin drawdown. Reduce position size and set stops above recent structural highs if holding longs.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.