Quick Links

Williams Companies' $5.5B Momentum Midstream Bid: Leverage Scenarios & LNG Pipeline Repricing

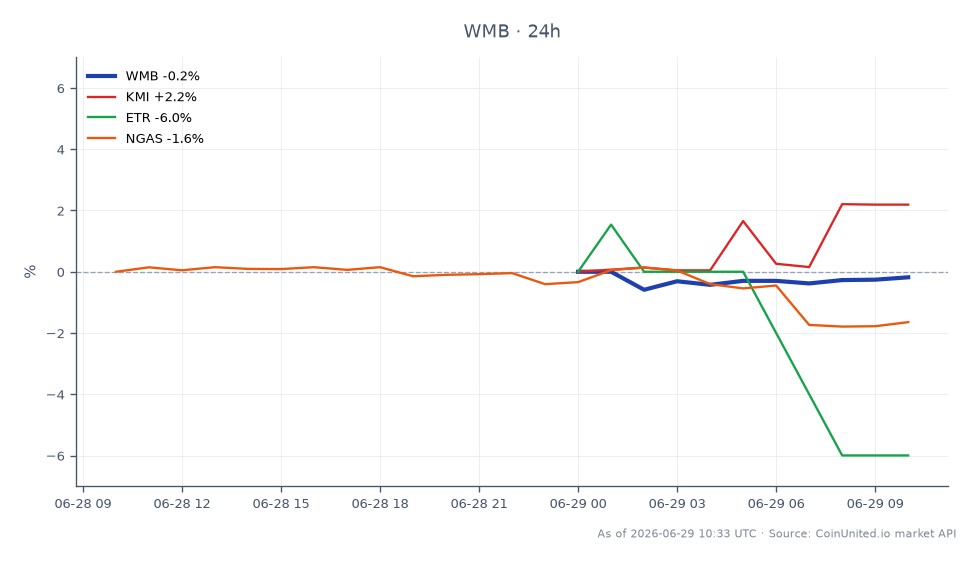

Data Snapshot

Key Takeaways

- •A 50x long WMB CFD at $77.31 gains ~250% on margin with a 5% deal-confirmation rally, but a 2% drop to ~$75.77 triggers liquidation — size positions with financing risk in mind.

- •Deal financing structure is the swing factor: equity issuance pressures WMB stock; debt-funded deal supports a re-rating toward LNG-growth peers.

- •Cheniere Energy and Gulf Coast LNG operators benefit from expanded dedicated pipeline capacity, creating positive read-through across the LNG value chain.

- •Energy Transfer's simultaneous pivot away from new LNG terminals creates a relative value opportunity: long WMB vs. short/underweight ET within midstream.

- •U.S. natural gas CFDs face a structural long-term bullish bias as Haynesville-to-LNG capacity expands, but this plays out over quarters, not days.

According to Bloomberg, as relayed via Seeking Alpha, Williams Companies, Inc. (WMB) is close to finalizing a $5.5 billion acquisition of privately held Momentum Midstream — described as one of the la

Event Summary

According to Bloomberg, as relayed via Seeking Alpha, Williams Companies, Inc. (WMB) is close to finalizing a $5.5 billion acquisition of privately held Momentum Midstream — described as one of the largest deals in WMB's corporate history. The transaction would expand Williams' Gulf Coast LNG-linked pipeline footprint and increase access to the Haynesville shale, a critical natural gas production corridor feeding U.S. LNG export terminals. The deal is not yet legally closed; it remains a credible, price-moving near-term event subject to final agreement and regulatory review. WMB is currently trading at $77.31, down 0.79% on the day, with a 24-hour range of $76.69–$78.86.

Leverage Impact Analysis

This energy sector acquisition creates asymmetric risk for leveraged WMB CFD positions on CoinUnited.io, where up to 2000x leverage is available.

Long scenario: A trader opening a 50x long WMB CFD at $77.31 controls $3,865 of notional exposure per $77.31 margin. If deal confirmation lifts WMB 5% to ~$81.18 (a plausible re-rating toward peers with LNG growth premiums), the position gains ~250% on margin. However, a 2% adverse move to ~$75.77 — triggered by overpayment concerns or equity issuance to fund the $5.5B deal — wipes the position at 50x.

Key leverage risk: Funding details matter enormously. If Williams raises equity to finance the acquisition, dilution pressure could push WMB toward the $76.69 intraday low and potentially lower. Traders holding leveraged longs should watch for any equity offering announcement as a near-term liquidation catalyst. Monitor open interest on CoinUnited.io for confirmation signals before sizing positions aggressively.

This deal fits the broader M&A acquisition wave repricing dynamic — initial volatility on announcement, followed by re-rating if accretion is confirmed.

Cross-Market Impact

The WMB deal has meaningful ripple effects across the energy sector acquisitions landscape:

- -Natural Gas (Henry Hub): Expanded Haynesville-to-Gulf Coast pipeline capacity is structurally bullish for long-dated U.S. gas contracts. Greater LNG export throughput tightens domestic balances over time.

- -Kinder Morgan (KMI): Sector read-through is mixed — WMB's aggressive LNG expansion may pressure peers to respond with their own M&A or capital deployment, but also confirms midstream infrastructure valuations are rising.

- -Cheniere Energy (LNG): More dedicated pipeline capacity feeding Gulf Coast liquefaction terminals is operationally positive, supporting utilization and long-term offtake contract visibility.

- -Entergy Corporation (ETR): Gulf Coast power and gas infrastructure operators benefit from increased pipeline reliability and supply security.

- -Energy Select Sector SPDR ETF (XLE): WMB is a constituent; a material re-rating flows into energy ETF NAV.

This deal also illustrates a strategic divergence from Energy Transfer, which is explicitly pivoting *away* from new LNG terminals toward Permian Basin infrastructure — a useful relative value lens for cross-sector acquisition repricing trades.

Trading Considerations

Key levels to watch: WMB's intraday low of $76.69 acts as immediate support; a confirmed deal announcement with accretive multiples could target the $78.86 intraday high and beyond. Resistance emerges near the 52-week range highs — check live charts on CoinUnited.io for current context. The critical unknown is financing structure: debt-funded deals are less dilutive to equity; equity issuance at current prices would pressure WMB shares. Watch for S&P/Moody's commentary on leverage ratios post-announcement.

For natural gas CFDs, the structural bullish thesis builds on a multi-quarter horizon — not an immediate trade — as pipeline capacity additions take time to affect physical balances.

Trade The Williams Companies, Inc. on CoinUnited.io

Trade WMB with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

If Williams issues new shares to fund part of the $5.5B acquisition, dilution pressure could push WMB below the $76.69 intraday low, triggering liquidations on leveraged longs above 20x. Traders should watch for any equity offering announcement as an immediate exit signal.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.