Quick Links

SandRidge Energy's $65M Mid-Continent Deal: Small Acquisition, Big M&A Signal

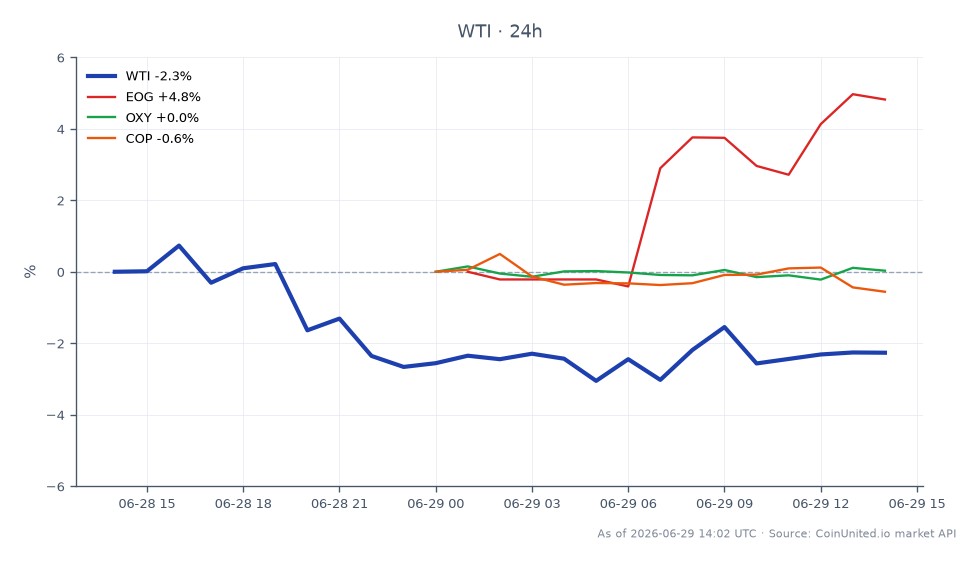

Data Snapshot

Key Takeaways

- •SandRidge's $65M Mid-Continent deal reflects a late-cycle E&P consolidation pattern spreading below mega-cap operators.

- •Mid-Continent assets offer low breakeven costs — strategically sound in a range-bound WTI environment.

- •Larger peers like ConocoPhillips, EOG, and Occidental may face acreage competition or divest non-core Mid-Continent positions in response.

- •The deal is WTI-neutral in isolation but reinforces U.S. operator confidence in current price levels — mild bullish read for domestic E&P sentiment.

- •Watch for follow-on Mid-Continent deal announcements from peers within the next 30–60 days as consolidation momentum builds.

SandRidge Energy has announced a $65 million acquisition of Mid-Continent assets, adding acreage in one of the U.S.'s most mature but cost-efficient onshore oil and gas basins. While the deal is modes

Event Analysis

SandRidge Energy has announced a $65 million acquisition of Mid-Continent assets, adding acreage in one of the U.S.'s most mature but cost-efficient onshore oil and gas basins. While the deal is modest in absolute dollar terms, it reflects a deliberate bolt-on consolidation strategy increasingly favored by smaller independents who lack the capital to compete in marquee shale plays like the Permian or Eagle Ford. SandRidge, which emerged from bankruptcy in 2016, has been methodically rebuilding its asset base — this acquisition fits squarely within that playbook.

What makes this deal noteworthy is the broader context: the M&A acquisition wave sweeping U.S. energy is no longer exclusively a mega-cap phenomenon. After ConocoPhillips, Occidental Petroleum, and EOG Resources dominated 2023–2024 deal headlines with multi-billion-dollar transactions, mid-tier and small-cap operators are now following suit with targeted acreage grabs. This signals that consolidation has moved beyond the top tier — a classic late-cycle M&A pattern where smaller players race to lock in assets before valuations reprice higher. SandRidge's move fits the global acquisition consolidation wave now filtering down the market-cap spectrum.

The Mid-Continent region — spanning Oklahoma, Kansas, and parts of the Texas Panhandle — offers relatively low breakeven costs and established infrastructure, making it attractive when WTI trades in ranges that compress margins elsewhere. This deal is less about growth optionality and more about low-cost production base-building, which is strategically sound if oil prices remain range-bound. Traders should note that energy sector acquisitions of this type often precede further deal activity as peers respond competitively.

What This Means for Traders

For equity traders, SandRidge itself is the most direct play, but its market cap and liquidity are limited. The more actionable signal lies in sector read-through: when sub-scale operators begin acquiring Mid-Continent assets, it suggests that larger players like ConocoPhillips, EOG Resources, and Occidental Petroleum may face incremental competition for remaining quality acreage — or conversely, may look to divest non-core Mid-Continent positions to fund higher-return projects. Both scenarios can create price catalysts in those names.

On the commodity side, this deal type is generally WTI neutral in isolation — a $65M acreage deal doesn't move supply curves. However, it reinforces the narrative that U.S. operators view current oil prices as sufficient to justify locking in production capacity, which is a mild bullish signal for sentiment around domestic supply discipline. The cross-sector acquisition repricing theme suggests watching for peer announcements in the Mid-Continent space over the next 30–60 days as deal momentum builds.

Volatility expectations for SandRidge's stock may spike near any formal announcement or closing date confirmation. Broader E&P sector sentiment remains tied to WTI direction and any macro risk-off shifts that could dampen acquisition appetites sector-wide.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

SandRidge Energy is a small-cap stock with limited CFD availability on most platforms — check CoinUnited.io's full asset list. Larger E&P names like ConocoPhillips and Occidental Petroleum are more likely to be available as stock CFDs.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.