Quick Links

Goldman's 130k June NFP Call: Strip Out the 40k World Cup Distortion Before Trading the Print

Data Snapshot

Key Takeaways

- •Goldman Sachs forecasts ~130k June NFP, but ~40k is World Cup-related hiring — the underlying labor trend is closer to ~90k, a meaningfully softer read.

- •Leveraged USD longs (DXY, USDJPY) face fade risk if markets correctly price the distortion post-print; a knee-jerk USD bid on the headline is the tactical fade setup.

- •US02Y yield at $4.11 is the primary rates expression — softer underlying NFP pressures front-end yields lower and adds to Fed cut-path pricing.

- •Gold benefits via lower real rates from the dovish re-pricing; the +0.03-0.04pp CPI/PCE bump is transient and insufficient to materially shift breakevens.

- •The August reversal (−15k below trend) creates a multi-week tail risk for USD bulls and a second-order fade opportunity in leisure/hospitality/transport sector strength.

According to Goldman Sachs research, the 2026 FIFA World Cup is expected to inflate U.S. nonfarm payrolls (NFP) by approximately 40,000 jobs in June, concentrated in leisure & hospitality, retail trad

Event Summary

According to Goldman Sachs research, the 2026 FIFA World Cup is expected to inflate U.S. nonfarm payrolls (NFP) by approximately 40,000 jobs in June, concentrated in leisure & hospitality, retail trade, and transportation. Goldman's resulting June NFP forecast sits at ~130,000 — implying underlying labor demand of only ~90,000 once the event boost is stripped out. The distortion then unwinds: Goldman models +10,000 above trend in July and −15,000 below trend in August, with inflation effects equally transient (core CPI +0.03pp June, core PCE +0.04pp June, then reversing from August onward).

This is a sell-side research call, not official government data. The alpha lies in understanding the distortion before the print lands.

Leverage Impact Analysis

The headline danger for leveraged traders: markets that naively trade a 130k print as strong are mispricing the underlying signal. The true labor trend reads closer to ~90k — consistent with a gradually cooling market and a more dovish Fed path per the Fed macro policy crossroads theme.

USD short scenario (EURUSD): A trader holding a 100x long EURUSD CFD at 1.0850 faces a squeeze risk if the 130k headline initially triggers a knee-jerk USD bid. That initial spike — if driven by consensus ignoring the 40k distortion — could represent a fade opportunity rather than a trend entry. At 100x leverage, a 30-pip adverse move represents ~2.75% of position notional; tight stops are essential around the NFP release window.

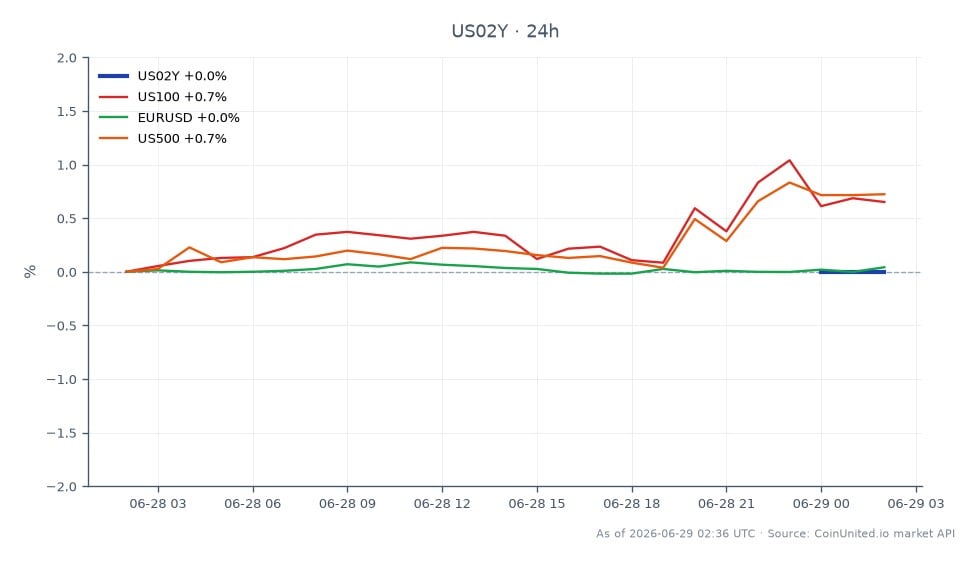

US02Y rates: Live data shows the 2-Year Treasury yield at $4.11 (+0.32% on the day). A softer underlying payrolls narrative (90k trend) would pressure front-end yields lower. A 50x long US02Y position opened at current levels carries meaningful reversion risk if markets correctly price the distortion as dovish. Monitor whether the post-print yield move aligns with the 130k headline or the 90k underlying read.

Liquidation watch: High-leverage USD longs (DXY, USDJPY) are most exposed to a post-print fade if the dovish interpretation dominates. The August reversal (-15k below trend) adds a multi-week tail risk for structural USD bulls — positions held through summer data releases face compounding drawdown.

Cross-Market Impact

The Fed & ECB policy divergence repricing theme intensifies here. A soft underlying NFP reinforces the case for ECB-Fed divergence narrowing, supporting Euro / US Dollar upside and capping US Dollar / Japanese Yen if BoJ remains on its hawkish path.

Gold: A dovish Fed re-pricing on softer underlying labor data supports Gold / US Dollar via lower real rates. The small, transient inflation bump (+0.03-0.04pp) is insufficient to shift medium-term breakevens materially — so gold's inflation-hedge bid doesn't activate, but the rate-cut repricing channel does.

Equities: The S&P 500 Index and NASDAQ 100 Index stand to benefit if the soft-landing narrative firms — growth holding, labor cooling, inflation non-persistent. Leisure, hospitality, and transport stocks may print temporarily strong employment metrics through July; avoid extrapolating sector strength as structural.

BTC: Risk sentiment and rate expectations are the primary transmission channel. A dovish re-pricing on underlying 90k trend data supports easier financial conditions, which is incrementally constructive for crypto risk proxies.

Trading Considerations

The key framework: adjust your NFP reaction by −40k before trading the print. A 130k headline is functionally a 90k print for Fed-path purposes. Front-end yields (US02Y currently at $4.11) and USD crosses are the primary tradeable expressions. Watch whether initial post-print moves reflect the distorted headline or the underlying signal — divergences create the tactical entry.

The August reversal (−15k below trend) sets up a second-order trade: any summer strength in leisure/hospitality/transport sector data should be faded. For rates and FX, the Fed & ECB rate patience macro repricing backdrop means each data point that undershoots on underlying strength incrementally adds to cut-pricing momentum.

Trade United States 2 Year Yield on CoinUnited.io

Trade US02Y with up to 2000xx leverage → | Create Free Account

Frequently Asked Questions

A 130k headline may trigger an initial USD bid, but traders who adjust for the ~40k event boost see the underlying print as a soft ~90k — a dovish signal. High-leverage USD longs should set tight stops around the release and watch for a fade opportunity if the initial spike lacks follow-through.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.