Quick Links

Esquire Financial's $348M Signature Bancorporation Merger: What It Means for Regional Bank Traders

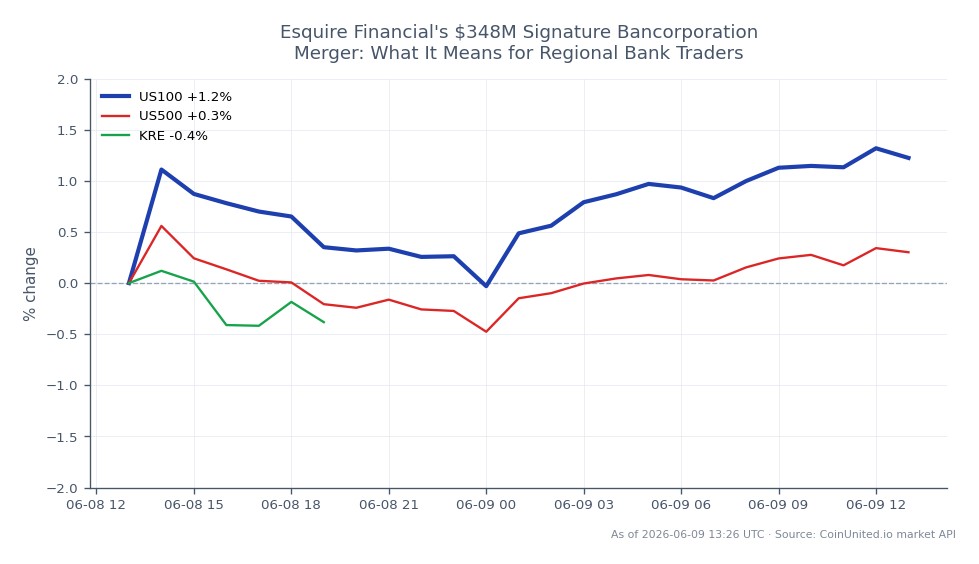

Data Snapshot

Key Takeaways

- •Esquire Financial is acquiring Signature Bancorporation for ~$348.4M (~$60/share implied), with Q3 2026 closing targeted pending regulatory and shareholder approvals.

- •The combined ~$4.8B-asset bank projects ~2% ROA, ~18% ROE, and ~5.25% NIM — materially above regional bank peer averages, supporting ESQ multiple expansion.

- •Esquire's litigation finance vertical (~67% of loans) is the core differentiation driver; successful integration could set a new profitability benchmark for small-cap banks.

- •Regulatory approval progress is the primary catalyst path — each milestone narrows deal-break risk and supports ESQ re-rating toward guided metrics.

- •The deal reinforces the broader niche-bank consolidation narrative; specialty lenders with strong NIM and low efficiency ratios may attract increased M&A attention from acquirers.

Esquire Financial Holdings (ESQ) has signed a definitive merger agreement to acquire Signature Bancorporation, Inc. — a Chicago-based bank holding company — in a deal valued at approximately $348.4 mi

Event Analysis

Esquire Financial Holdings (ESQ) has signed a definitive merger agreement to acquire Signature Bancorporation, Inc. — a Chicago-based bank holding company — in a deal valued at approximately $348.4 million, implying roughly $60 per Signature share, according to a PR Newswire release and SEC filings. Both boards unanimously approved the transaction, with closing targeted for Q3 2026, subject to regulatory approvals, shareholder votes, and SEC effectiveness of a Form S-4 registration statement. Post-merger, Esquire shareholders will hold approximately 72% of the combined entity, with Signature shareholders retaining around 28%.

What makes this deal strategically significant is the projected financial profile of the combined institution. Management guided for approximately 2% return on assets, 18% return on equity, a ~5.25% net interest margin, and a ~46% efficiency ratio — metrics that would place the combined ~$4.8 billion-asset bank well above most regional and community bank peers. Esquire's core differentiation is its litigation finance vertical, which accounts for roughly 67% of loans (~$1.2 billion) and 77% of deposits (~$1.6 billion), a high-margin niche that sets it apart from generic commercial lenders.

This deal fits squarely within the ongoing M&A acquisition wave reshaping U.S. community banking. Regulatory clearance for a deal of this structure signals that banking authorities remain open to consolidation, even after the regional bank stress events of recent years. The Signature brand will be retained as a "Signature Division of Esquire Bank" in Chicago — a deliberate brand preservation strategy that reduces deposit attrition risk during integration. For the broader cross-sector acquisition repricing trend, this adds another data point that well-capitalized niche banks can command significant M&A premiums.

What This Means for Traders

For ESQ equity traders, each regulatory milestone toward the Q3 2026 close represents a re-rating catalyst. The projected profitability metrics — if credible — support a premium price-to-tangible-book and price-to-earnings multiple relative to the State Street SPDR S&P Regional Banking ETF peer basket. A long ESQ vs. regional bank ETF pairs trade is the most natural expression of the thesis: ESQ outperforms if the combined entity delivers on its guided ROA/ROE, while the ETF provides a hedge against sector-wide weakness. Traders should monitor integration commentary, deposit retention data, and any regulatory conditions attached to approvals as key thesis checkpoints.

The sector read-through is modestly bullish for small- and mid-cap bank M&A sentiment. The deal reinforces that niche lending franchises — particularly those with specialty commercial verticals — can attract meaningful acquisition premiums, which may prompt re-evaluation of similar sub-$10B asset banks as potential targets. Those tracking the regional bank and financial earnings surge theme should note that high-quality consolidators like ESQ could become benchmark comparables that reprice peers upward. Volatility risk is primarily deal-execution-driven: regulatory delays, integration friction between New York and Chicago operations, or credit quality deterioration in litigation finance lending would be the key downside catalysts to monitor through the close timeline.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

The transaction is structured as a stock-based bank holding company merger, with Signature shareholders receiving ESQ shares at an implied value of approximately $60 per Signature share. No cash component has been publicly specified in the filings.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.

">%0D%0A <path d="m65.883 9.018.032 5.181h-1.223c-.773-3.733-2.671-5.73-5.797-5.73-4.441 0-6.5 4.442-6.5 9.913 0 5.985 2.38 10.588 6.79 10.588 3.024 0 5.084-1.898 6.211-6.597h1.287l-.482 6.05a13.606 13.606 0 0 1-7.434 1.93c-7.016 0-11.36-4.409-11.36-11.071 0-7.467 4.989-12.166 11.36-12.166a12.961 12.961 0 0 1 7.112 1.899M68.714 21.89c0-5.47 3.572-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.573 9.205-8.367 9.205a7.908 7.908 0 0 1-8.271-8.464zm11.876.354c0-4.762-1.095-8.406-3.669-8.406-2.38 0-3.478 2.703-3.478 6.92 0 4.762 1.126 8.431 3.701 8.431 2.382 0 3.444-2.735 3.444-6.956M93.236 27.555c0 1.126.515 1.318 2.03 1.416v1.062h-8.497V28.97c1.514-.097 2.03-.29 2.03-1.415V16.16l-1.93-1.126v-.611l5.663-1.77h.709l-.005 14.9zM88.345 8.18a2.625 2.625 0 0 1 5.246 0 2.625 2.625 0 0 1-5.246 0zM109.007 18.157c0-1.867-.709-2.8-2.479-2.8a6.474 6.474 0 0 0-3.604 1.319v10.877c0 1.126.482 1.319 1.962 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.93-1.126v-.612l5.76-1.77h.741l-.129 3.154a7.735 7.735 0 0 1 5.954-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.995 1.416v1.062h-8.432V28.97c1.48-.097 1.963-.29 1.963-1.416v-9.396zM123.52 21.851c0 3.927 1.706 6.308 5.247 6.308 3.54 0 5.985-1.867 5.985-6.5V10.82c0-1.74-.419-2.03-3.058-2.253V7.442h7.37v1.126c-2.252.258-2.574.515-2.574 2.253v11.425c0 5.535-3.797 8.116-8.561 8.116-5.697 0-9.108-2.64-9.108-8.174v-11.4c0-1.77-.321-1.965-2.574-2.221V7.44h9.849v1.126c-2.253.258-2.574.45-2.574 2.22l-.002 11.064zM152.26 18.157c0-1.867-.707-2.8-2.478-2.8a6.484 6.484 0 0 0-3.605 1.319v10.877c0 1.126.483 1.319 1.964 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.931-1.126v-.612l5.761-1.77h.74l-.129 3.154a7.731 7.731 0 0 1 5.953-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.996 1.416v1.062h-8.432V28.97c1.479-.097 1.962-.29 1.962-1.416v-9.396zM166.259 27.555c0 1.126.515 1.318 2.029 1.416v1.062h-8.496V28.97c1.512-.097 2.029-.29 2.029-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.709l-.003 14.9zM161.368 8.18a2.62 2.62 0 0 1 2.622-2.518 2.625 2.625 0 0 1 2.623 2.518 2.626 2.626 0 0 1-4.441 1.786 2.62 2.62 0 0 1-.804-1.786zM175.33 12.976h4.183v1.48h-4.183v10.652c0 1.964.741 2.8 2.253 2.8a3.755 3.755 0 0 0 2.414-.901l.387.58a5.65 5.65 0 0 1-4.956 2.768c-2.64 0-4.57-1.384-4.57-4.989v-10.91h-1.996v-.741a13.265 13.265 0 0 0 5.508-4.928h.965l-.005 4.189zM195.514 19.38v.741h-10.492c-.129 4.506 2.189 7.177 5.342 7.177a5.427 5.427 0 0 0 4.796-2.609l.515.29a6.75 6.75 0 0 1-6.888 5.374c-4.665 0-7.787-3.443-7.787-8.406 0-5.507 3.539-9.3 7.948-9.3 4.313 0 6.566 2.864 6.566 6.726m-10.427-.45h6.437c0-3.025-.805-5.085-2.899-5.085-2.125 0-3.283 2.125-3.541 5.084M207.001 7.054v-.676l5.696-1.545h.707v21.788c0 1.094.064 1.45 1.287 1.545l.805.064v.965l-5.857 1.16h-.838l.129-2.993a6.145 6.145 0 0 1-5.181 2.993c-3.895 0-6.5-3.154-6.5-8.046 0-6.087 3.604-9.59 8.206-9.59a5.117 5.117 0 0 1 3.478 1.126V8.048l-1.932-.994zm-5.342 13.709c0 3.926 1.609 6.855 4.538 6.855a3.901 3.901 0 0 0 2.736-1.03v-8.496c0-2.51-1.062-3.99-2.993-3.99-2.703 0-4.28 2.64-4.28 6.667M219.683 24.754a2.796 2.796 0 0 1 2.587 1.729 2.8 2.8 0 1 1-5.387 1.072 2.75 2.75 0 0 1 1.721-2.6 2.753 2.753 0 0 1 1.079-.2zM230.592 27.555c0 1.126.516 1.318 2.029 1.416v1.062h-8.501V28.97c1.512-.097 2.03-.29 2.03-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.708l.002 14.9zM225.7 8.18a2.626 2.626 0 0 1 4.441-1.787c.488.47.777 1.11.804 1.787a2.625 2.625 0 0 1-5.245 0zM233.842 21.89c0-5.47 3.573-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.572 9.205-8.366 9.205a7.904 7.904 0 0 1-7.809-5.179 7.904 7.904 0 0 1-.463-3.285zm11.876.354c0-4.762-1.094-8.406-3.669-8.406-2.382 0-3.479 2.703-3.479 6.92 0 4.762 1.126 8.431 3.7 8.431 2.382 0 3.444-2.735 3.444-6.956M18.386.684a17.469 17.469 0 1 0 0 34.937 17.469 17.469 0 0 0 0-34.937zm0 31.74a14.277 14.277 0 1 1 0-28.554 14.277 14.277 0 0 1 0 28.554z" fill="%23fff"/>%0D%0A <path d="M18.393 36.019a17.868 17.868 0 1 1 17.86-17.868 17.887 17.887 0 0 1-17.86 17.868zm0-34.938a17.07 17.07 0 1 0 17.063 17.07 17.089 17.089 0 0 0-17.063-17.07zm0 31.74a14.675 14.675 0 1 1 10.366-4.297 14.691 14.691 0 0 1-10.373 4.303m0-28.552a13.877 13.877 0 1 0 13.879 13.878A13.893 13.893 0 0 0 18.386 4.275z" fill="%23fff"/>%0D%0A <path d="M17.42 8.46a8.46 8.46 0 1 1-16.923 0 8.46 8.46 0 0 1 16.924 0" fill="%23E48A22"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="sy6kzo59ya">%0D%0A <path fill="%23fff" transform="translate(.5)" d="M0 0h250v36.019H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

"><path fill="%23fff" transform="scale(1.9886)" d="M27.72,2.61a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-30.14,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-32.16,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-34.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-40.2,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-58.29,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-62.32,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m30.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m22.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m34.16,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m18.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.27,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-56.29,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-48.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2"/><path d="M123.088,117.106a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M123.088,133.085a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M91.095,145.087a1.987,1.987,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989,2.01,2.01,0,0,1,1.989-1.988zM107.109,145.087a1.988,1.988,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989c-.035-1.081.872-1.988,1.989-1.988zM115.098,145.087a1.987,1.987,0,1,1,0,3.977,1.987,1.987,0,0,1-1.988-1.989c-.035-1.081.872-1.988,1.988-1.988zM123.088,145.087a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M151.069,149.064a1.988,1.988,0,1,1-1.989,1.989c-.035-1.082.872-1.989,1.989-1.989zM25.271,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491c0-1.575,1.277-2.852,2.83-2.852h6.492a2.852,2.852,0,0,1,2.852,2.852v6.49h.021z" fill="%23fff"/><path d="M33.38,30.568a2.852,2.852,0,0,1-2.852,2.851H7.798a2.852,2.852,0,0,1-2.851-2.851V7.817a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.75h-.021zM29.315,11.86a2.852,2.852,0,0,0-2.852-2.852H11.842A2.852,2.852,0,0,0,8.99,11.86v14.642a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852V11.86h-.021zM25.271,142.338a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491a2.852,2.852,0,0,1,2.852-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.491z" fill="%23fff"/><path d="M33.38,150.468a2.852,2.852,0,0,1-2.852,2.852H7.798a2.852,2.852,0,0,1-2.851-2.852v-22.751a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.751h-.021zm-4.065-18.686a2.852,2.852,0,0,0-2.852-2.852H11.842a2.852,2.852,0,0,0-2.852,2.852v14.621a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852v-14.621h-.021zM145.171,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.491a2.851,2.851,0,0,1-2.851-2.852v-6.491a2.851,2.851,0,0,1,2.851-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.49z" fill="%23fff"/><path d="M153.301,30.568a2.852,2.852,0,0,1-2.852,2.851h-22.75a2.852,2.852,0,0,1-2.852-2.851V7.817a2.852,2.852,0,0,1,2.852-2.852h22.75a2.852,2.852,0,0,1,2.852,2.852v22.75zm-4.065-18.707a2.852,2.852,0,0,0-2.852-2.852h-14.621a2.852,2.852,0,0,0-2.851,2.852v14.642a2.852,2.852,0,0,0,2.851,2.852h14.621a2.852,2.852,0,0,0,2.852-2.852V11.86zM78.535,62.051c-9.176,0-16.607,7.431-16.607,16.607,0,9.176,7.431,16.607,16.607,16.607,9.176,0,16.607-7.431,16.607-16.607,0-9.176-7.431-16.607-16.607-16.607zm0,30.214c-7.501,0-13.572-6.07-13.572-13.572,0-7.501,6.07-13.572,13.572-13.572,7.501,0,13.572,6.07,13.572,13.572,0,7.501-6.071,13.572-13.572,13.572z" fill="%23fff"/><path d="M78.535,95.649c-9.385,0-16.991-7.64-16.991-16.99,0-9.386,7.64-16.992,16.99-16.992,9.386,0,16.992,7.64,16.992,16.991,0,9.35-7.64,16.991-16.991,16.991zm0-33.214c-8.966,0-16.258,7.292-16.258,16.258s7.291,16.258,16.258,16.258c8.966,0,16.258-7.291,16.258-16.258-.035-8.966-7.292-16.258-16.258-16.258zm0,30.214c-7.71,0-13.956-6.28-13.956-13.956,0-7.71,6.28-13.956,13.956-13.956,7.71,0,13.956,6.28,13.956,13.956,0,7.676-6.28,13.956-13.956,13.956zm0-27.179c-7.292,0-13.223,5.931-13.223,13.223,0,7.292,5.931,13.223,13.223,13.223,7.292,0,13.223-5.931,13.223-13.223-.035-7.292-5.966-13.223-13.223-13.223z" fill="%23fff"/><path d="M69.569,77.507a8.06,8.06,0,1,0,0-16.119,8.06,8.06,0,0,0,0,16.119z" fill="%23E48A22"/></g><defs><clipPath id="arusb4546a"><path fill="%23fff" transform="translate(0 .019)" d="M0,0h157v157H0z"/></clipPath></defs></svg>)

">%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23fff"/>%0D%0A <path d="M106.646 32.584H4.356A3.857 3.857 0 0 1 .5 28.741V3.867A3.853 3.853 0 0 1 4.355.02h102.29a3.86 3.86 0 0 1 3.855 3.848V28.74a3.853 3.853 0 0 1-3.854 3.845z" fill="%23A6A6A6"/>%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23000"/>%0D%0A <path d="M25.063 16.13a4.717 4.717 0 0 1 2.25-3.961 4.84 4.84 0 0 0-3.812-2.059c-1.603-.168-3.159.959-3.976.959-.833 0-2.09-.942-3.447-.915a5.079 5.079 0 0 0-4.271 2.603c-1.848 3.195-.47 7.89 1.3 10.472.886 1.265 1.92 2.679 3.274 2.626 1.325-.052 1.82-.84 3.417-.84 1.584 0 2.05.84 3.43.81 1.42-.021 2.317-1.27 3.171-2.546a10.434 10.434 0 0 0 1.452-2.952 4.572 4.572 0 0 1-2.786-4.197h-.003zm-2.61-7.718a4.643 4.643 0 0 0 1.065-3.33 4.74 4.74 0 0 0-3.064 1.583 4.42 4.42 0 0 0-1.092 3.207 3.917 3.917 0 0 0 3.091-1.46zM44.25 25.674H42.4l-1.015-3.183H37.86l-.966 3.183H35.09l3.493-10.838h2.156l3.509 10.838h.002zm-3.17-4.517-.918-2.83c-.097-.29-.28-.97-.547-2.042h-.033c-.108.461-.28 1.142-.515 2.042l-.902 2.83h2.914zm12.137.515a4.422 4.422 0 0 1-1.085 3.152 3.178 3.178 0 0 1-2.41 1.03 2.415 2.415 0 0 1-2.235-1.109v4.1H45.75v-8.417c0-.835-.021-1.691-.064-2.569h1.529l.097 1.239h.032a3.09 3.09 0 0 1 2.398-1.395 3.095 3.095 0 0 1 2.552 1.088c.645.817.973 1.84.925 2.88l-.001.001zm-1.77.064a3.22 3.22 0 0 0-.516-1.882 1.781 1.781 0 0 0-1.513-.771c-.427 0-.84.15-1.166.426-.349.284-.59.678-.684 1.118a2.26 2.26 0 0 0-.08.528v1.302a2.09 2.09 0 0 0 .525 1.44 1.737 1.737 0 0 0 1.36.587 1.783 1.783 0 0 0 1.529-.755c.389-.59.58-1.29.544-1.995v.002zm10.768-.064a4.422 4.422 0 0 1-1.084 3.152 3.182 3.182 0 0 1-2.413 1.03 2.415 2.415 0 0 1-2.233-1.109v4.1h-1.739v-8.417c0-.835-.021-1.691-.065-2.569h1.53l.096 1.239h.033a3.092 3.092 0 0 1 3.803-1.153c.443.189.836.478 1.148.846.645.817.973 1.84.924 2.88v.001zm-1.771.064a3.22 3.22 0 0 0-.517-1.882 1.778 1.778 0 0 0-1.511-.771c-.427 0-.841.15-1.168.426-.349.284-.59.678-.683 1.118-.048.172-.075.35-.082.528v1.302a2.097 2.097 0 0 0 .523 1.44 1.74 1.74 0 0 0 1.361.587 1.781 1.781 0 0 0 1.53-.755c.39-.59.581-1.289.547-1.995v.002zm11.831.9a2.893 2.893 0 0 1-.964 2.251 4.278 4.278 0 0 1-2.956.949 5.163 5.163 0 0 1-2.809-.675l.402-1.447a4.84 4.84 0 0 0 2.511.676 2.371 2.371 0 0 0 1.53-.442 1.444 1.444 0 0 0 .548-1.181 1.511 1.511 0 0 0-.452-1.11 4.188 4.188 0 0 0-1.496-.836c-1.9-.707-2.85-1.742-2.85-3.104a2.737 2.737 0 0 1 1.006-2.187 3.981 3.981 0 0 1 2.664-.852 5.27 5.27 0 0 1 2.463.515l-.437 1.415a4.31 4.31 0 0 0-2.084-.498 2.121 2.121 0 0 0-1.438.45 1.289 1.289 0 0 0-.437.982 1.327 1.327 0 0 0 .5 1.061 5.63 5.63 0 0 0 1.577.836c.78.274 1.485.725 2.06 1.318.45.521.686 1.192.663 1.88v-.002zm5.762-3.472H76.12v3.794c0 .965.338 1.447 1.014 1.447.26.006.52-.021.773-.08l.048 1.318a3.942 3.942 0 0 1-1.352.192 2.085 2.085 0 0 1-1.61-.63 3.077 3.077 0 0 1-.578-2.107v-3.94h-1.141v-1.302h1.141v-1.43l1.707-.515v1.943h1.915l-.001 1.31zm8.627 2.54a4.284 4.284 0 0 1-1.03 2.959 3.674 3.674 0 0 1-2.865 1.19 3.504 3.504 0 0 1-2.746-1.14 4.154 4.154 0 0 1-1.022-2.879 4.249 4.249 0 0 1 1.054-2.974 3.655 3.655 0 0 1 2.842-1.155 3.577 3.577 0 0 1 2.768 1.142 4.1 4.1 0 0 1 1 2.856v.001zm-1.802.04a3.496 3.496 0 0 0-.465-1.843 1.72 1.72 0 0 0-1.562-.931 1.746 1.746 0 0 0-1.594.93 3.554 3.554 0 0 0-.466 1.877 3.485 3.485 0 0 0 .466 1.844 1.782 1.782 0 0 0 3.141-.015 3.51 3.51 0 0 0 .48-1.863v.001zm7.454-2.356a3.03 3.03 0 0 0-.547-.047 1.641 1.641 0 0 0-1.42.692 2.605 2.605 0 0 0-.434 1.543v4.1H88.18v-5.355c0-.82-.017-1.64-.052-2.46h1.514l.063 1.495h.049c.164-.488.466-.918.868-1.239.363-.271.804-.419 1.257-.42.145 0 .29.01.435.032v1.656l.002.003zm7.774 2.011c.004.264-.017.528-.064.788h-5.214a2.262 2.262 0 0 0 .756 1.77 2.59 2.59 0 0 0 1.707.544c.72.01 1.435-.115 2.11-.368l.272 1.204a6.527 6.527 0 0 1-2.623.483 3.805 3.805 0 0 1-2.86-1.067 3.95 3.95 0 0 1-1.039-2.87 4.473 4.473 0 0 1 .967-2.942 3.331 3.331 0 0 1 2.734-1.253 2.916 2.916 0 0 1 2.56 1.253c.48.728.722 1.586.694 2.456v.002zm-1.658-.45a2.348 2.348 0 0 0-.337-1.335 1.518 1.518 0 0 0-1.384-.725 1.648 1.648 0 0 0-1.381.706c-.297.392-.475.86-.515 1.35h3.62l-.003.004zM37.359 11.005a11.12 11.12 0 0 1-1.25-.063v-5.24c.487-.075.98-.112 1.472-.11 1.994 0 2.912.98 2.912 2.576 0 1.842-1.085 2.837-3.134 2.837zm.292-4.742a3.49 3.49 0 0 0-.688.055v3.984c.192.02.385.028.578.023 1.306 0 2.05-.743 2.05-2.133-.002-1.24-.674-1.929-1.94-1.929zm5.702 4.78a1.832 1.832 0 0 1-1.755-1.225 1.826 1.826 0 0 1-.097-.75 1.87 1.87 0 0 1 1.916-2.031 1.817 1.817 0 0 1 1.851 1.968 1.881 1.881 0 0 1-1.915 2.04v-.002zm.032-3.382c-.617 0-1.012.577-1.012 1.383 0 .79.404 1.365 1.005 1.365.6 0 1.004-.616 1.004-1.383 0-.779-.396-1.363-.996-1.363V7.66zm8.29-.545-1.203 3.84h-.784L49.19 9.29a12.619 12.619 0 0 1-.309-1.24h-.016c-.07.42-.174.835-.308 1.24l-.53 1.668h-.792l-1.132-3.841h.878l.435 1.826c.103.435.19.845.263 1.232h.017c.062-.323.165-.727.315-1.225l.546-1.833h.696l.523 1.795c.126.435.229.861.309 1.264h.023c.062-.426.15-.848.262-1.264l.468-1.795h.84-.004zm4.426 3.84h-.854V8.75c0-.679-.263-1.02-.776-1.02a.888.888 0 0 0-.854.942v2.284h-.854v-2.74c0-.34-.009-.705-.032-1.1h.751l.04.593h.024a1.38 1.38 0 0 1 1.219-.67c.806 0 1.336.616 1.336 1.619v2.3-.002zm2.356 0h-.855v-5.6h.855v5.6zm3.115.088a1.832 1.832 0 0 1-1.851-1.976 1.87 1.87 0 0 1 1.914-2.031 1.816 1.816 0 0 1 1.851 1.968 1.88 1.88 0 0 1-1.914 2.04v-.001zm.032-3.383c-.617 0-1.012.578-1.012 1.383 0 .79.404 1.366 1.003 1.366.6 0 1.005-.617 1.005-1.384 0-.779-.394-1.363-.998-1.363l.002-.002zm5.252 3.296-.063-.442h-.022a1.314 1.314 0 0 1-1.125.53 1.118 1.118 0 0 1-1.178-1.131c0-.946.823-1.438 2.247-1.438v-.071c0-.506-.268-.76-.798-.76a1.8 1.8 0 0 0-1.004.286l-.174-.561a2.46 2.46 0 0 1 1.32-.332c1.005 0 1.511.529 1.511 1.588v1.415a5.79 5.79 0 0 0 .056.917l-.77-.001zm-.118-1.913c-.949 0-1.425.23-1.425.774a.543.543 0 0 0 .586.6.818.818 0 0 0 .841-.78l-.002-.594zm4.982 1.913-.04-.617h-.024a1.288 1.288 0 0 1-1.234.704c-.927 0-1.614-.814-1.614-1.96 0-1.201.712-2.049 1.683-2.049a1.157 1.157 0 0 1 1.084.523h.017V5.35h.856v4.57c0 .372.009.72.031 1.036h-.76zm-.126-2.259a.93.93 0 0 0-.9-.998c-.631 0-1.021.561-1.021 1.351 0 .775.402 1.305 1.003 1.305a.96.96 0 0 0 .914-1.019v-.639h.004zm6.277 2.347a1.831 1.831 0 0 1-1.85-1.975 1.87 1.87 0 0 1 1.913-2.031 1.816 1.816 0 0 1 1.852 1.968 1.88 1.88 0 0 1-1.916 2.038zm.031-3.382c-.616 0-1.011.577-1.011 1.383 0 .79.403 1.365 1.003 1.365.6 0 1.005-.616 1.005-1.383 0-.782-.394-1.366-1-1.366h.003zm6.478 3.296h-.857V8.753c0-.68-.263-1.02-.775-1.02a.888.888 0 0 0-.854.94v2.285h-.855V8.215c0-.34-.009-.704-.032-1.099h.752l.04.593h.023a1.38 1.38 0 0 1 1.218-.671c.807 0 1.338.616 1.338 1.62l.002 2.3zm5.749-3.2h-.94v1.864c0 .473.165.712.497.712.128 0 .255-.013.38-.04l.023.648c-.213.07-.438.103-.663.095-.673 0-1.076-.372-1.076-1.344V7.758h-.56v-.64h.56v-.704l.841-.254v.956h.94v.641l-.002.001zm4.52 3.2h-.853v-2.19c0-.687-.26-1.035-.775-1.035a.838.838 0 0 0-.856.909v2.315h-.851V5.355h.854v2.307h.017a1.296 1.296 0 0 1 1.156-.624c.814 0 1.312.63 1.312 1.636l-.003 2.285zm4.635-1.715H96.72a1.102 1.102 0 0 0 1.21 1.137c.353.004.704-.058 1.035-.181l.133.593a3.212 3.212 0 0 1-1.29.237 1.789 1.789 0 0 1-1.913-1.936c0-1.178.728-2.063 1.818-2.063.982 0 1.598.728 1.598 1.826.006.13-.004.26-.03.387h.003zm-.783-.609c0-.593-.3-1.011-.846-1.011a1.014 1.014 0 0 0-.934 1.011h1.78z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="uavr3vx5ga">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

">%0D%0A <path d="M106.426 32.584H4.574a4.037 4.037 0 0 1-3.775-2.507 4.029 4.029 0 0 1-.3-1.564V4.09A4.028 4.028 0 0 1 3.01.318a4.038 4.038 0 0 1 1.565-.3h101.852a4.039 4.039 0 0 1 3.774 2.507c.203.496.305 1.028.3 1.564v24.424a4.032 4.032 0 0 1-4.074 4.071z" fill="%23000"/>%0D%0A <path d="M106.426.67a3.445 3.445 0 0 1 3.422 3.42v24.424a3.444 3.444 0 0 1-3.422 3.42H4.574a3.444 3.444 0 0 1-3.422-3.42V4.089A3.438 3.438 0 0 1 4.574.67h101.852zm0-.651H4.574A4.088 4.088 0 0 0 .5 4.089v24.425a4.029 4.029 0 0 0 2.508 3.771 4.039 4.039 0 0 0 1.566.3h101.852a4.04 4.04 0 0 0 2.892-1.181 4.023 4.023 0 0 0 1.182-2.89V4.089a4.082 4.082 0 0 0-4.074-4.07z" fill="%23A6A6A6"/>%0D%0A <path d="M39.122 8.323a2.216 2.216 0 0 1-.57 1.628 2.558 2.558 0 0 1-3.585 0 2.393 2.393 0 0 1-.734-1.794 2.394 2.394 0 0 1 .734-1.785 2.395 2.395 0 0 1 1.792-.736c.34.004.676.087.978.244.292.122.546.318.736.57l-.407.407a1.52 1.52 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57 1.677 1.677 0 0 0-.573 1.384 1.675 1.675 0 0 0 .57 1.384c.355.336.817.538 1.304.57a1.789 1.789 0 0 0 1.386-.57 1.347 1.347 0 0 0 .407-.976h-1.793v-.652h2.366v.326h-.003zm3.748-2.036h-2.2v1.547h2.038v.57H40.67v1.547h2.2v.651h-2.854V5.718h2.855v.57zm2.69 4.315h-.653V6.287h-1.385v-.57h3.422v.57H45.56v4.315zm3.747 0V5.718h.652v4.884h-.652zm3.423 0h-.652V6.287h-1.385v-.57h3.34v.57h-1.385v4.315h.082zm7.74-.65a2.559 2.559 0 0 1-3.585 0 2.394 2.394 0 0 1-.736-1.792 2.393 2.393 0 0 1 .736-1.791 2.558 2.558 0 0 1 3.586 0 2.395 2.395 0 0 1 .735 1.791 2.391 2.391 0 0 1-.736 1.791zm-3.096-.408c.346.35.812.554 1.304.57a1.623 1.623 0 0 0 1.304-.57c.366-.369.57-.867.57-1.387a1.675 1.675 0 0 0-.57-1.381 1.924 1.924 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57c-.365.367-.57.864-.57 1.381a1.676 1.676 0 0 0 .57 1.387zm4.726 1.058V5.718h.736l2.366 3.826V5.718h.651v4.884h-.657l-2.523-3.989v3.99H62.1z" fill="%23fff" stroke="%23fff" stroke-width=".2" stroke-miterlimit="10"/>%0D%0A <path d="M55.989 17.767a3.43 3.43 0 0 0-3.258 2.149c-.173.43-.256.89-.246 1.352a3.47 3.47 0 0 0 2.159 3.241c.427.175.884.263 1.345.26a3.432 3.432 0 0 0 3.258-2.15c.172-.429.256-.889.245-1.351a3.376 3.376 0 0 0-3.503-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-7.578-5.536a3.431 3.431 0 0 0-3.258 2.149c-.172.43-.256.89-.246 1.352a3.472 3.472 0 0 0 2.16 3.241c.426.175.883.263 1.344.26a3.432 3.432 0 0 0 3.258-2.15c.173-.429.256-.889.246-1.351a3.376 3.376 0 0 0-3.504-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-9.044-4.478v1.466h3.503a3.077 3.077 0 0 1-.815 1.872 3.607 3.607 0 0 1-2.688 1.059 3.796 3.796 0 0 1-3.83-3.908 3.838 3.838 0 0 1 2.347-3.605c.47-.198.973-.301 1.483-.303a4.041 4.041 0 0 1 2.688 1.056l1.06-1.056a5.223 5.223 0 0 0-3.667-1.466 5.49 5.49 0 0 0-5.46 5.373 5.49 5.49 0 0 0 5.46 5.374 4.693 4.693 0 0 0 3.748-1.547 4.9 4.9 0 0 0 1.304-3.42c.017-.3-.01-.6-.082-.892h-5.051v-.003zm36.992 1.14a3.163 3.163 0 0 0-2.933-2.198c-1.793 0-3.26 1.384-3.26 3.5a3.406 3.406 0 0 0 3.423 3.502 3.345 3.345 0 0 0 2.852-1.547l-1.141-.814a1.986 1.986 0 0 1-1.711.976 1.769 1.769 0 0 1-1.711-1.058l4.644-1.954-.163-.407zm-4.726 1.14a1.977 1.977 0 0 1 1.793-2.035 1.441 1.441 0 0 1 1.303.732l-3.096 1.303zm-3.83 3.34h1.549V14.267h-1.548v10.18zm-2.444-5.943a2.682 2.682 0 0 0-1.874-.814 3.502 3.502 0 0 0-3.34 3.501 3.369 3.369 0 0 0 2.048 3.149c.409.174.848.266 1.292.27a2.34 2.34 0 0 0 1.793-.814h.081v.489c0 1.302-.736 2.035-1.874 2.035a1.81 1.81 0 0 1-1.711-1.221l-1.304.57a3.36 3.36 0 0 0 3.096 2.035c1.793 0 3.26-1.058 3.26-3.582v-6.19h-1.467v.572zm-1.792 4.804a2.025 2.025 0 0 1-1.956-2.117 2.02 2.02 0 0 1 1.956-2.117 1.961 1.961 0 0 1 1.874 2.117 1.957 1.957 0 0 1-1.875 2.114v.003zm19.881-9.035h-3.667v10.175h1.548v-3.83h2.119a3.185 3.185 0 0 0 3.087-1.92 3.177 3.177 0 0 0-1.82-4.237 3.185 3.185 0 0 0-1.267-.193v.005zm.082 4.885h-2.2V15.65h2.2a1.788 1.788 0 0 1 1.792 1.71 1.862 1.862 0 0 1-1.793 1.791v.005zm9.37-1.465c-1.14 0-2.282.488-2.689 1.547l1.385.57a1.438 1.438 0 0 1 1.385-.736 1.532 1.532 0 0 1 1.63 1.303v.079a3.236 3.236 0 0 0-1.548-.407c-1.467 0-2.934.814-2.934 2.28a2.386 2.386 0 0 0 2.524 2.279 2.294 2.294 0 0 0 1.955-.977h.082v.817h1.466v-3.908a3.08 3.08 0 0 0-3.259-2.85l.003.003zm-.163 5.617c-.489 0-1.222-.244-1.222-.893 0-.814.896-1.058 1.63-1.058.48.002.954.113 1.385.326a1.895 1.895 0 0 1-1.793 1.62v.005zm8.555-5.373-1.71 4.396H99.5l-1.793-4.396h-1.63l2.69 6.188-1.549 3.419h1.548l4.153-9.607h-1.629.002zm-13.688 6.51h1.548V14.267h-1.548v10.18z" fill="%23fff"/>%0D%0A <path d="M8.974 6.125a1.59 1.59 0 0 0-.326 1.14v17.992a1.61 1.61 0 0 0 .408 1.14l.081.081 10.104-10.095v-.163L8.974 6.125z" fill="url(%23nqixmws78b)"/>%0D%0A <path d="m22.5 19.802-3.34-3.338v-.244l3.34-3.338.081.082 3.99 2.28c1.141.65 1.141 1.709 0 2.36L22.5 19.802z" fill="url(%23euwe5vohvc)"/>%0D%0A <path d="m22.581 19.72-3.422-3.418L8.974 26.477c.408.407.978.407 1.711.082l11.896-6.84z" fill="url(%23wso0uh08dd)"/>%0D%0A <path d="M22.581 12.882 10.685 6.125c-.736-.407-1.303-.326-1.71.081l10.184 10.096 3.422-3.42z" fill="url(%23mrdt54dj1e)"/>%0D%0A <path opacity=".2" d="m22.5 19.64-11.815 6.675a1.334 1.334 0 0 1-1.63 0l-.08.082.08.081a1.333 1.333 0 0 0 1.63 0L22.5 19.64z" fill="%23000"/>%0D%0A <path opacity=".12" d="M8.974 26.316a1.59 1.59 0 0 1-.326-1.14v.081a1.61 1.61 0 0 0 .408 1.14v-.081h-.082zm17.6-8.956L22.5 19.64l.081.08 3.993-2.279a1.355 1.355 0 0 0 .815-1.14c0 .408-.326.733-.815 1.059z" fill="%23000"/>%0D%0A <path opacity=".25" d="m10.685 6.206 15.89 9.037c.488.326.814.651.814 1.059a1.352 1.352 0 0 0-.815-1.14L10.685 6.125c-1.143-.652-2.037-.163-2.037 1.14v.08c0-1.22.894-1.79 2.037-1.139z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <linearGradient id="nqixmws78b" x1="18.265" y1="27.13" x2="2.062" y2="22.737" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2300A0FF"/>%0D%0A <stop offset=".007" stop-color="%2300A1FF"/>%0D%0A <stop offset=".26" stop-color="%2300BEFF"/>%0D%0A <stop offset=".512" stop-color="%2300D2FF"/>%0D%0A <stop offset=".76" stop-color="%2300DFFF"/>%0D%0A <stop offset="1" stop-color="%2300E3FF"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="euwe5vohvc" x1="28.064" y1="17.927" x2="8.353" y2="17.927" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FFE000"/>%0D%0A <stop offset=".409" stop-color="%23FFBD00"/>%0D%0A <stop offset=".775" stop-color="orange"/>%0D%0A <stop offset="1" stop-color="%23FF9C00"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="wso0uh08dd" x1="20.731" y1="16.06" x2="7.736" y2="-5.775" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FF3A44"/>%0D%0A <stop offset="1" stop-color="%23C31162"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="mrdt54dj1e" x1="6.443" y1="34.068" x2="12.205" y2="24.305" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2332A071"/>%0D%0A <stop offset=".069" stop-color="%232DA771"/>%0D%0A <stop offset=".476" stop-color="%2315CF74"/>%0D%0A <stop offset=".801" stop-color="%2306E775"/>%0D%0A <stop offset="1" stop-color="%2300F076"/>%0D%0A </linearGradient>%0D%0A <clipPath id="oefv1zwvza">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)