Quick Links

Berkshire Hathaway's $8.5B Taylor Morrison Buyout: Leverage Scenarios & Homebuilder Sector Repricing

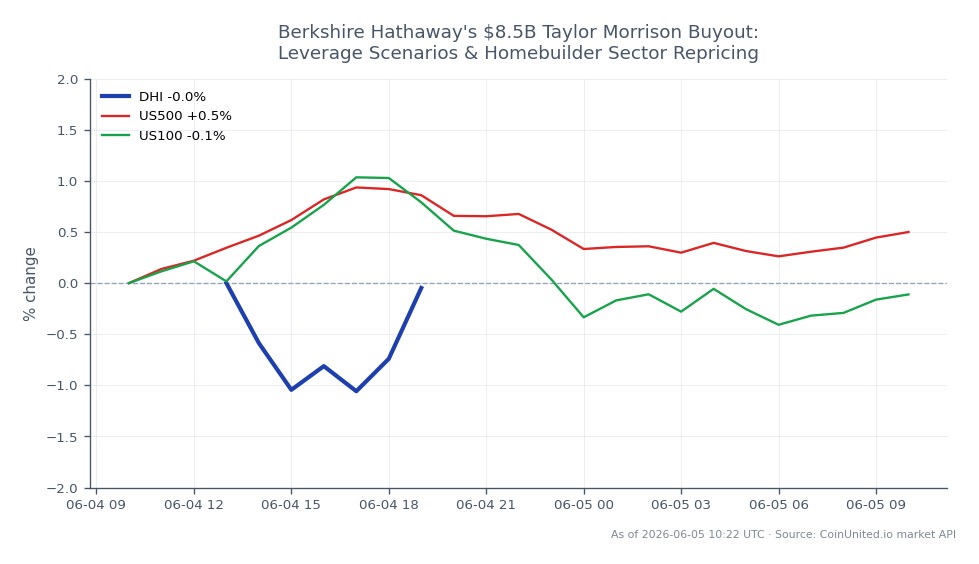

Data Snapshot

Key Takeaways

- •TMHC reprices to a merger-arb spread capped at $72.50 — leveraged longs near the offer price face asymmetric risk (minimal upside, sharp downside on deal break).

- •The 24% takeout premium validates private-market homebuilder valuations, creating re-rating potential for DHI, LEN, and PHM as uncapped leverage plays.

- •Greg Abel's first major Berkshire acquisition signals long-duration conviction in U.S. housing demand and structural undersupply.

- •A $221.6M termination fee materially reduces the probability of a competing bid, anchoring TMHC's trading range tightly to deal timeline and regulatory risk.

- •Cross-market impact is limited — no immediate commodity or FX spillover, but the deal reinforces the broader M&A acquisition wave theme in U.S. equities.

Berkshire Hathaway and Taylor Morrison Home Corporation (NYSE: TMHC) jointly announced a definitive all-cash acquisition agreement, according to the official Taylor Morrison investor relations release

Event Summary

Berkshire Hathaway and Taylor Morrison Home Corporation (NYSE: TMHC) jointly announced a definitive all-cash acquisition agreement, according to the official Taylor Morrison investor relations release. Berkshire will pay $72.50 per share, implying an equity value of approximately $6.8 billion and an enterprise value of $8.5 billion — a 24% premium to TMHC's $58.50 closing price on May 29, 2026. The deal was unanimously approved by TMHC's board and is expected to close in H2 2026, pending shareholder vote and Hart-Scott-Rodino antitrust clearance. Upon close, TMHC will be delisted and become a wholly owned Berkshire subsidiary. The transaction carries a ~$221.6 million termination fee, limiting the likelihood of a competing bid.

This marks one of the first major acquisitions under new Berkshire CEO Greg Abel, with Berkshire signaling plans to unify its site-built homebuilding operations into a single scaled platform — a long-duration bet on U.S. housing demand.

Leverage Impact Analysis

For leveraged traders on CoinUnited.io, TMHC has structurally transformed from a cyclical homebuilder into a merger-arbitrage instrument — and that changes the leverage calculus entirely.

TMHC long scenario: A trader holding a 50x long TMHC CFD opened near the pre-announcement $58.50 price now sees the stock repricing toward the $72.50 offer — roughly a 24% move. At 50x leverage, that translates to an approximate 1,200% gain on margin. However, the upside is now hard-capped at $72.50; TMHC will not trade significantly above the offer price unless a competing bid emerges (deterred by the $221.6M breakup fee).

Key risk for leveraged longs at current levels: If TMHC is already trading near $72.50, the remaining spread to close is thin — perhaps 1–3% annualized for a H2 2026 close. High-leverage longs initiated near the offer price face asymmetric risk: minimal upside, but a deal-break scenario (regulatory block or shareholder rejection) could cause a 15–20% gap down, wiping leveraged positions rapidly.

Peer homebuilder CFD plays: The more asymmetric leverage opportunity may lie in D.R. Horton, Inc., Lennar (LEN), and PulteGroup (PHM). These names carry full M&A optionality — no cap on upside — and Berkshire's 24% takeout multiple provides a re-rating floor. A 20x long DHI CFD, for example, participates in any sector re-rating without the spread compression inherent in the TMHC arb. Monitor open interest and funding rates on CoinUnited.io for confirmation signals.

Cross-Market Impact

This deal is part of the broader M&A Acquisition Wave reshaping U.S. equities and fits squarely within the media & homebuilder acquisition surge theme. The primary impact is sector-specific with limited direct macro spillover.

Homebuilder peers (DHI, LEN, PHM): Berkshire's willingness to pay 24x for a homebuilder platform validates private-market valuations above current public multiples, creating re-rating pressure across the group. Traders should watch homebuilder ETFs (XHB, ITB) for near-term sentiment tailwinds.

Berkshire Hathaway (BRK.B): Capital deployment at this scale is a signal rather than a P&L mover for Berkshire given its size. BRK.B may see modest selling pressure from investors questioning capital allocation into a rate-sensitive sector, but the structural read is constructive.

S&P 500 Index / NASDAQ 100 Index: Broad indices see minimal direct impact. The deal reinforces a risk-on narrative around U.S. housing resilience, which is incrementally positive for the cross-sector acquisition repricing theme but won't move index needles independently.

Commodities: No immediate mechanical impact on lumber or construction materials. Berkshire's stated intention to scale operations is a long-term demand signal, not a near-term supply shock.

Trading Considerations

TMHC is now a spread trade anchored at $72.50, with deal-break risk the primary variable. Per our acquisition arbitrage guide, the key levels to watch are: (1) TMHC trading at a persistent discount wider than 3% to $72.50 — signals rising deal-break concern; (2) any Hart-Scott-Rodino second request — low probability given sector fragmentation but would push the close timeline and widen the spread. For sector rotation plays, watch DHI, LEN, and PHM relative to pre-announcement multiples as the market reprices M&A optionality. The broader mega-deal cross-sector acquisition wave context suggests this deal could catalyze additional consolidation bids in mid-cap homebuilders over the next 6–12 months.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

TMHC is now capped at the $72.50 offer price, so leveraged longs initiated near that level carry near-zero upside with meaningful downside if the deal breaks — the risk/reward is unfavorable for high leverage. The arb spread (TMHC vs. $72.50) is the only remaining trade, best suited for low-leverage positions sized for a H2 2026 close timeline.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.