Quick Links

TransAlta's $1B Colorado Peaker Deal: Gas Capacity Gets a Premium in the AI Power Era

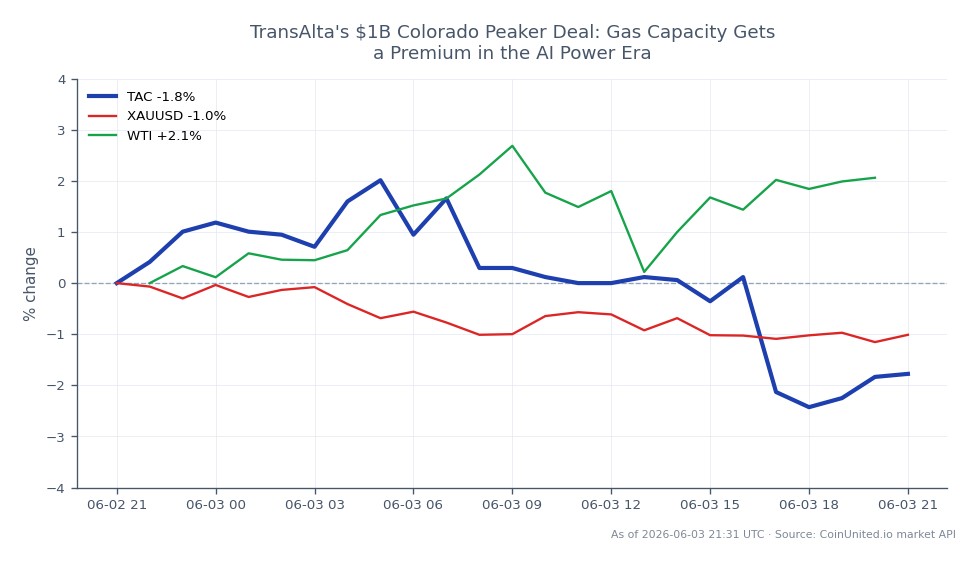

Data Snapshot

Key Takeaways

- •TransAlta is acquiring Blackstone-backed Colorado peaking plants for ~$1B, materially expanding its U.S. gas generation footprint and exposure to AI/data-center-driven power demand.

- •Deal financing structure is the critical variable — accretive contracted cash flows support equity re-rating; heavy debt funding risks credit spread widening.

- •The transaction establishes a fresh EV/MW comparable for U.S. gas peakers, potentially lifting valuations for peer IPPs (NRG, Vistra, AES) holding similar assets.

- •Blackstone's clean exit reinforces that gas peaker assets clear at strong multiples, validating NAV marks for infrastructure and energy transition PE funds.

- •TAC equity (current price $0.0166 per live data) is the primary tradeable; watch financing disclosures and rating-agency commentary as secondary catalysts after announcement.

TransAlta Corporation has agreed to acquire a portfolio of Blackstone-backed Colorado peaking plants for approximately $1 billion, marking one of the largest gas-fired asset acquisitions by a Canadian

Event Analysis

TransAlta Corporation has agreed to acquire a portfolio of Blackstone-backed Colorado peaking plants for approximately $1 billion, marking one of the largest gas-fired asset acquisitions by a Canadian independent power producer (IPP) in recent years. According to the research report, the seller is a Blackstone Energy Transition Partners vehicle — consistent with Blackstone's documented capital-recycling strategy in U.S. gas generation, which has included comparable ~$1B deals such as its Hill Top Energy Center acquisition in Pennsylvania. For TransAlta, this deal materially expands its U.S. footprint with flexible, dispatchable peaking capacity in the Western grid.

What makes this deal strategically significant is the macro context driving it. As reported across energy trade press, Blackstone has explicitly framed its gas plant transactions as a direct response to surging AI and data-center power demand — a theme now reshaping valuations for flexible generation assets across North America. Colorado peakers, positioned to serve load centers amid rising renewables intermittency, carry strategic optionality that pure baseload assets lack. This deal fits squarely into the mega-deal cross-sector acquisition wave reshaping energy infrastructure ownership.

At $1 billion, the transaction is material relative to TransAlta's balance sheet. The funding mix — debt, equity issuance, or asset rotation — will determine whether rating agencies view this as leverage-neutral or a credit event. A strongly contracted peaker portfolio could support an EBITDA re-rating; heavily merchant exposure funded by debt risks spread widening. This is also a clean capital recycling exit for Blackstone, validating that energy, pharma & tech M&A deal flow remains robust even as rate environments stay elevated. Closing will require FERC and state regulatory approvals, with timelines typically ranging from several months to approximately one year.

The transaction establishes a fresh comparable for U.S. gas peaker valuation — implied EV/MW metrics from this deal can be applied to peers holding similar fleets, potentially triggering a broader cross-sector acquisition repricing across listed IPPs and infrastructure funds. For the AI datacenter energy capital raise theme specifically, this deal confirms that private capital continues to monetize grid-reliability assets at strong exit multiples.

What This Means for Traders

The primary trade is in TransAlta equity (TAC on NYSE-listed equivalent). According to live market data, TAC is currently priced at $0.0166, down 1.89% on the day, with a 24-hour range of $0.0163–$0.0173. Announcement-day reactions for acquisition targets in this sector typically hinge on perceived accretion: if the deal is seen as FCF/FFO-accretive with contracted cash flows, expect upside re-rating; if markets focus on leverage risk or dilutive equity issuance, the initial reaction may be muted or negative. Traders should watch for financing structure disclosures and any rating-agency commentary as secondary catalysts. This is a situation where the acquisition arbitrage playbook applies — monitor deal milestones rather than treating announcement as a one-time event.

For sector read-through, North American IPPs and utilities with significant gas peaking exposure (NRG, Vistra, AES) may see modest valuation support as the deal implies continued buyer appetite at premium multiples. Infrastructure and energy transition funds holding similar assets benefit from NAV mark validation. The global acquisition consolidation wave in power generation remains a live theme — flexible gas capacity is being repriced as a scarcity asset, not a stranded one. Direct commodity impact on WTI crude or natural gas is negligible since no new supply is added; existing plants simply change ownership.

Trade TAC on CoinUnited.io

Trade TAC with up to 2000xx leverage → | Create Free Account

Frequently Asked Questions

Accretion depends on the contracted vs. merchant revenue split and funding mix — if peakers carry long-term capacity payments and are funded with modest leverage, the deal likely adds to FFO/share. Traders should wait for management guidance on EBITDA contribution and financing terms.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.