Quick Links

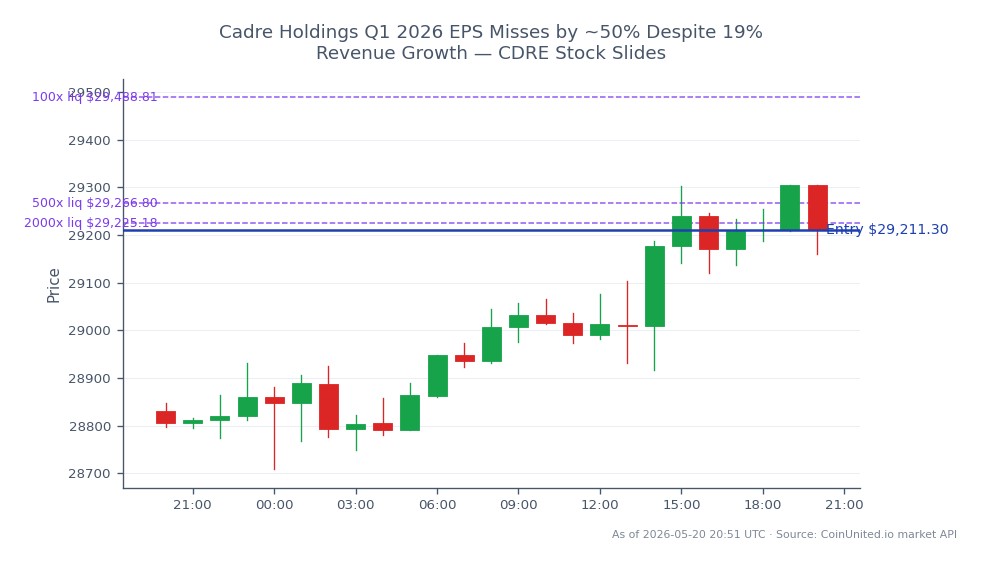

Cadre Holdings Q1 2026 EPS Misses by ~50% Despite 19% Revenue Growth — CDRE Stock Slides

Data Snapshot

Key Takeaways

- •CDRE reported Q1 2026 EPS of $0.05 vs. consensus of $0.09–$0.10 — a ~44–50% miss, according to Investing.com.

- •Net sales grew 19% YoY, creating a sharp revenue-earnings divergence that points to margin compression, not demand weakness.

- •The most likely drivers of the miss are acquisition integration costs, input cost inflation, or unfavorable product mix — all potentially multi-quarter headwinds.

- •Broader index impact (S&P 500, Nasdaq 100) is negligible given CDRE's small-cap status, but specialty industrial peers may face sentiment spillover.

- •Forward guidance on FY2026 margins and EPS is the key variable — a reaffirmation could limit the stock's downside; a cut would deepen the selloff.

Cadre Holdings, Inc. (NYSE: CDRE) reported Q1 2026 earnings on May 11–12, 2026, delivering a significant bottom-line disappointment. According to Investing.com, the company posted EPS of $0.05 against

Event Analysis

Cadre Holdings, Inc. (NYSE: CDRE) reported Q1 2026 earnings on May 11–12, 2026, delivering a significant bottom-line disappointment. According to Investing.com, the company posted EPS of $0.05 against a consensus estimate of $0.09–$0.10, representing a miss of roughly 44–50%. The stock slid in response, a textbook reaction to a surprise of this magnitude.

What makes this result particularly striking is the disconnect between the top and bottom lines. Net sales reportedly increased 19% year-over-year — a strong growth print for a specialty industrials name in the public safety and protective equipment space. Yet that revenue expansion failed to translate into earnings, pointing to a margin compression story: rising input costs, acquisition integration friction, unfavorable product mix, or elevated interest expense are the most likely culprits. This kind of revenue-earnings divergence is a hallmark of the earnings miss revenue shock dynamic — where headline growth masks deteriorating unit economics.

Cadre Holdings operates in the defense-adjacent public safety equipment market, supplying law enforcement and first-responder gear. This niche means the company is exposed to procurement cycles, government budget timelines, and post-acquisition cost absorption. The 19% sales growth likely reflects recent M&A activity flowing through the revenue line, while integration costs weigh on margins — a pattern that can persist across multiple quarters before normalizing.

For the broader specialty industrials and small-cap industrial sector, this result introduces a caution flag. If investors read Cadre's margin compression as a sector-wide signal — rather than a company-specific issue — peer names in safety equipment and defense supply chains could face valuation re-rating pressure.

What This Means for Traders

The immediate signal is bearish for CDRE. A ~50% EPS miss with no apparent catalyst for rapid recovery tends to produce sustained selling pressure, particularly if management's forward guidance on margins and FY2026 EPS fails to reassure the market. Traders should watch closely for commentary on whether the margin miss is structural or transitory — that distinction will determine whether this is a one-quarter reset or a multi-quarter re-rating. For guidance on structuring positions around events like this, see how to trade earnings misses.

Sentiment impact on broader indices like the S&P 500 Index and NASDAQ 100 Index is negligible — CDRE is a small-cap name without systemic weight. However, traders positioned in specialty industrials or public safety peers should monitor whether the selloff spreads via sector sentiment. The earnings miss recovery plays framework becomes relevant if the stock overshoots to the downside relative to intrinsic value — particularly if management reaffirms full-year revenue guidance. Monitor open interest and volume on CoinUnited.io for confirmation signals before positioning for a mean-reversion trade.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

Strong revenue growth and weak EPS typically reflect margin compression — likely from acquisition integration costs, higher input prices, or elevated interest expense. The top-line growth may be M&A-driven, while costs haven't yet normalized.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.