Быстрые ссылки

Poland's Fuel Windfall Tax: Leverage Map for WTI at $77.12, PLN Cross-Rates, and European Energy Equity Repricing

Снимок данных

Основные выводы

- •Leveraged WTI CFD traders face heightened liquidation risk: a 100x long at $77.12 has a ~$0.77 buffer to liquidation, well within the 24h range of $74.09–$78.63.

- •Orlen fell up to 6.6% intraday on a policy announcement alone — final legislative text (windfall formula, duration, gas inclusion) is the next binary repricing event for European energy equity CFDs.

- •Cross-market: PLN rates and Polish 10-year yields are the cleanest instruments to monitor for fiscal stress if windfall tax revenues underperform the ~1.5–1.6bn PLN monthly shortfall.

- •Copycat windfall tax risk across CEE and broader Europe adds a regulatory risk premium overhang to BP, Shell, and other downstream European energy names.

- •Gold's inflation hedge bid is reinforced by activist fiscal responses to Iran war energy shocks — a secondary but real tailwind within the broader risk-off repricing.

As reported by Reuters (citing State Secretary Wojciech Wrochna, ~May 20), Poland's government under Prime Minister Donald Tusk has announced a two-pronged fiscal response to Iran war–driven fuel pric

Event Summary

As reported by Reuters (citing State Secretary Wojciech Wrochna, ~May 20), Poland's government under Prime Minister Donald Tusk has announced a two-pronged fiscal response to Iran war–driven fuel price spikes: deep cuts to VAT on fuel (from 23% to 8%) and excise duties (to EU-minimum levels), combined with daily maximum retail price caps — and critically, a windfall profit levy on oil and gas companies to fund the ~1.5–1.6 billion PLN (~€350–360m) monthly revenue shortfall. Orlen, Poland's state-controlled refiner, fell up to 6.6% intraday on the announcement before closing down 2.2%. The full legislative text — including the exact windfall profit definition, reference period, and tax rate — is still being finalized, with ministry initiatives expected "next week" per Wrochna.

The package is designed to cut pump prices by approximately 1.2 PLN per litre (~$0.32), offsetting Polish gasoline prices up +22% and diesel up +40% versus pre-war levels — both outpacing EU averages.

Leverage Impact Analysis

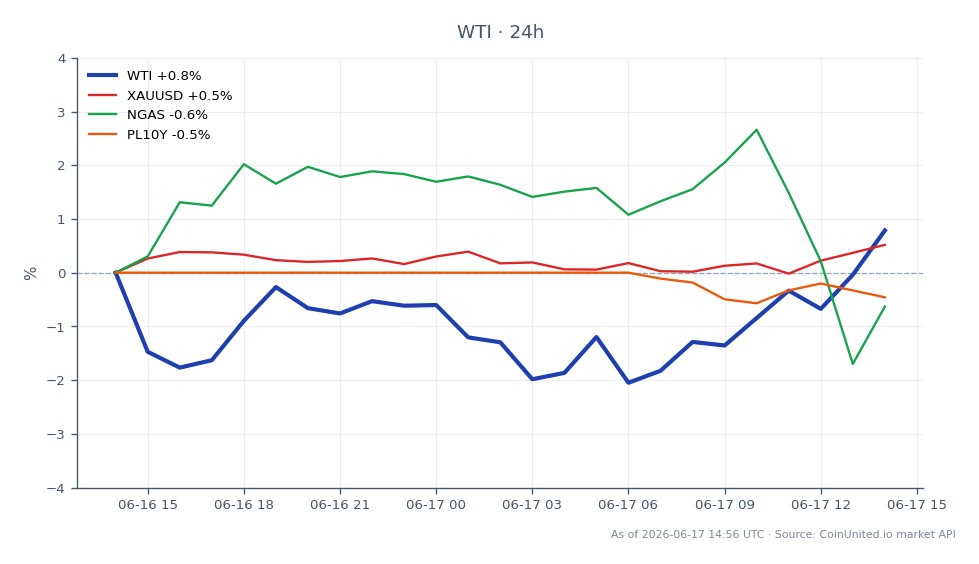

WTI currently trades at $77.12 (+1.79% on the day, 24h range $74.09–$78.63). Poland alone cannot move global crude benchmarks, but the policy adds a new macro inflation risk-off repricing signal that leveraged energy traders must model.

WTI Commodity CFD scenarios:

- -A 50x long WTI CFD entered at $77.12 faces liquidation if price drops ~2% to ~$75.57 (assuming 1% margin buffer). Given the 24h low of $74.09, that level was tested intraday — a stark reminder of how quickly leverage amplifies policy-driven volatility.

- -A 100x long WTI CFD at $77.12 has a liquidation threshold roughly $0.77 below entry (~$76.35), well within normal intraday range. Position sizing must account for the policy uncertainty premium embedded in European energy markets right now.

For European energy equity CFDs (BP p.l.c., Shell PLC): windfall tax contagion risk is the key lever. A 20x long BP CFD held through a 3–4% regulatory repricing move would see ~60–80% of margin eroded. Watch for legislative text details — the exact windfall formula is the binary event.

Volatility implication: Orlen's 6.6% intraday swing on a *policy announcement* (not law) signals that final legislative text could produce a comparable or larger move. Traders holding high-leverage energy positions should monitor the Polish energy ministry's weekly schedule closely.

Cross-Market Impact

Energy Equities (CFDs): The direct hit is on Polish refining margins, but the broader signal is regulatory risk premium expansion across European downstream energy. BP p.l.c. and Shell PLC have limited direct Polish exposure, but the copycat-policy risk — seen in prior EU windfall tax cycles — adds a valuation overhang. US majors (XOM, CVX, COP, OXY) are more insulated but not immune to sentiment-driven sector rotation.

PLN Forex: The policy is net-ambiguous for USD/PLN and EUR/PLN. Lower CPI from capped fuel prices could reduce NBP hawkishness, softening PLN carry support. Conversely, fiscal uncertainty (will windfall tax revenues cover the 1.5–1.6bn PLN monthly gap?) could widen Polish risk premia. The Poland 10-Year Yield is the cleanest instrument to monitor for sovereign stress signals.

Natural Gas & Gasoil: The windfall scope may extend to natural gas and low sulphur gasoil — watch legislative text for explicit inclusion. If confirmed, crack spread compression becomes a cross-commodity trade.

Gold: As part of the broader oil shock and geopolitical risk-off backdrop, gold's safe-haven bid remains supported. Activist fiscal responses to Iran war energy shocks reinforce the inflation hedge thesis.

Trading Considerations

WTI's current range ($74.09–$78.63 over 24h) reflects broader Iran war uncertainty; Poland's windfall tax is a secondary, regional signal rather than a crude-moving catalyst on its own. Key levels to watch: $74.00 (24h low / near-term support), $78.63 (24h high / resistance). For context on how the broader Iran conflict continues to drive energy market structure, see the Hormuz Strait energy supply shock theme and the WTI Light Crude Oil deep-dive.

The primary binary risk event is legislative text publication (expected within days per Reuters). Exact windfall profit definition, duration, and whether gas is included will reprice Orlen and European energy equity CFDs. Monitor Polish energy ministry announcements and Orlen guidance revisions as the key near-term catalysts.

Trade WTI Light Crude Oil on CoinUnited.io

Trade WTI with up to 1000xx leverage → | Create Free Account

Часто задаваемые вопросы

Poland alone cannot shift global crude prices, but the policy adds volatility risk to energy positions — WTI's 24h range of $74.09–$78.63 means a 100x long at $77.12 has less than $1 of buffer before liquidation. Reduce position size or widen stops around legislative announcement dates.

Продолжить исследование

Отказ от ответственности: Этот бриф предназначен только для образовательных целей и не является инвестиционной рекомендацией.