クイックリンク

Banca Ifis Craters 24%: What a 40–45% Profit Guidance Cut Means for Leveraged Italian Bank Traders

データスナップショット

重要なポイント

- •Banca Ifis slashed 2026 net profit guidance by ~40–45% to €100–110m (from €170–190m), triggering a ~24% single-session collapse.

- •Leverage wipeout threshold: any long CFD position above approximately 4x leverage on BIT:IF would have been liquidated by the 24% move alone.

- •€70m in fresh provisions and a competitive sale of a €1.5bn NPL portfolio introduce additional unquantified downside not yet reflected in revised guidance.

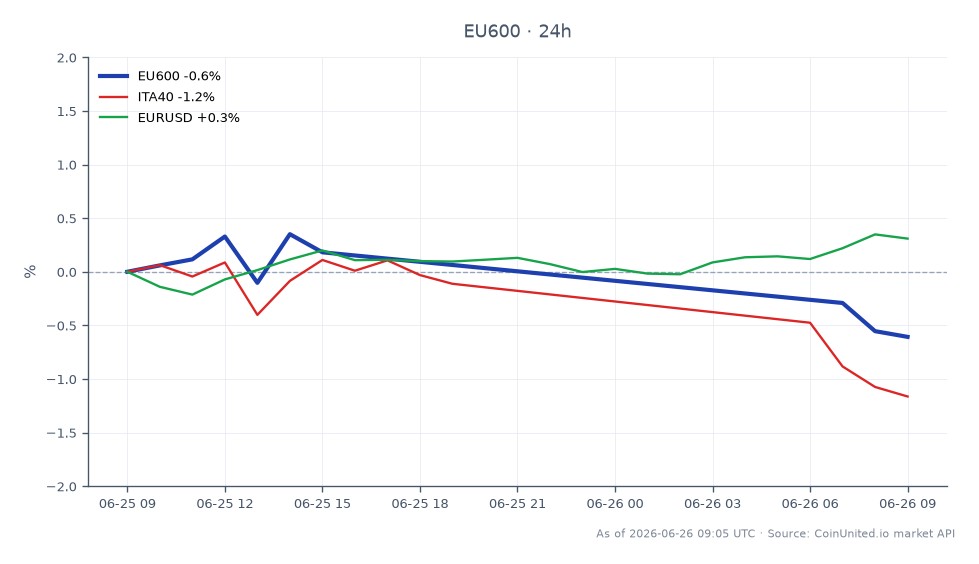

- •Cross-market spillover is limited but watch the FTSE MIB and Italian bank peers for sympathy pressure; EUR/USD is not materially impacted at this scale.

- •Ongoing Bank of Italy inspection and open-ended NPL sale timeline sustain elevated volatility — position sizing and stop placement are critical for any re-entry.

Banca Ifis (BIT:IF) collapsed approximately 24% after the bank's Board approved a dramatic profit guidance cut for 2026. According to a company press release, net profit guidance was slashed to €100–1

Event Summary

Banca Ifis (BIT:IF) collapsed approximately 24% after the bank's Board approved a dramatic profit guidance cut for 2026. According to a company press release, net profit guidance was slashed to €100–110 million from a prior estimate of €170–190 million — an implied downgrade of roughly 40–45%. As reported by Finimize, the bank simultaneously booked approximately €70 million in fresh provisions and launched a competitive sale process for its non-performing loan (NPL) unit, which manages roughly €1.5 billion of primarily small, unsecured loans. The guidance revision excludes the financial effects of the NPL deconsolidation and any further impact from an ongoing Bank of Italy regulatory inspection, leaving significant unquantified downside risk on the table.

The strategic rationale, per the company's own communication, is an accelerated pivot toward a specialty finance model focused on corporate clients, distancing the bank from NPL-centric earnings. Fitch Ratings currently affirms Banca Ifis at 'BB+' with Stable Outlook, though its cost-of-risk assumption of 5–6% over the next three years now looks prescient. The bank reported a pro-forma CET1 of 13.7% and Total Capital Ratio of 16.0%, providing capital buffer — but the earnings story has fundamentally changed overnight.

Leverage Impact Analysis

This is a textbook earnings miss and guidance shock event, and the leverage math is punishing. A trader holding a 50x long CFD on Banca Ifis opened before the announcement would face a notional loss of approximately 1,200% of margin on a 24% price drop — instant liquidation territory at any leverage above ~4x long. Even a 10x long position would be wiped out with roughly 240% of margin lost, triggering forced closure well before the session low.

For short-side traders, the calculus inverts: a 20x short CFD on BIT:IF opened at prior levels would have generated roughly 480% return on margin in a single session — illustrating the asymmetric payoff when a high-conviction guidance cut materialises. The key risk now is whether the stock has already priced in the worst. With guidance excluding NPL sale proceeds and inspection outcomes, residual uncertainty remains elevated, making short re-entries at bounces the higher-probability setup versus chasing further downside from a 24% gap lower.

Position sizing is critical: given the unresolved Bank of Italy inspection and open-ended NPL sale timeline, volatility is unlikely to compress quickly. Traders using CoinUnited's up to 2000x leverage on stock CFDs should size accordingly — the headline risk premium here remains live.

Cross-Market Impact

This event is primarily idiosyncratic to Banca Ifis, but it carries sector-read-through worth monitoring. The FTSE MIB Index — Italy's benchmark — has material exposure to mid-cap Italian financials; a single-name move of this magnitude can weigh on financial-sector weighting and sentiment within the index. More broadly, the STOXX Europe 600 Index tracks European financials as a sector, and a narrative of pressured profitability in Italian specialty lenders could prompt marginal re-rating of peers with similar NPL exposure.

For the Euro / US Dollar pair, the direct impact is negligible at this scale — a single mid-cap bank's guidance cut does not move sovereign spreads or ECB policy expectations. However, if this event contributes to a broader Italian bank credit concern narrative, EUR sentiment could face mild headwinds from BTP-Bund spread widening. Watch Italian 10-year yields for any contagion signal. There is no meaningful crypto, commodity, or US equity read-through at this stage.

Trading Considerations

The 24% single-session decline creates a classic post-earnings miss structure: an initial flush, a potential technical bounce into the 38–50% retracement zone, and then a secondary leg lower if the NPL sale terms or inspection outcome disappoints. Key levels to watch are the pre-announcement support zones and the stock's 52-week low, which now likely sits close to or at current prices. Volume confirmation of any bounce will be critical — low-volume rallies in this context are typically distribution, not recovery.

The unresolved variables — Bank of Italy inspection outcome, NPL portfolio sale price, and any dividend revision — mean this remains an event-driven trade rather than a value entry. Monitor Italian peer banks (Mediobanca, BPER Banca) for sympathy moves that may offer cleaner leverage setups with lower idiosyncratic risk.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

よくある質問

A 24% price decline means any long CFD position using more than approximately 4x leverage (where 25% adverse move = 100% of margin) would face full liquidation. At 10x leverage, the margin loss would be approximately 240%, triggering forced closure well before the intraday low.

探索を続ける

免責事項: このブリーフは教育目的のみであり、投資アドバイスではありません。