Quick Links

GSK's $11B Nuvalent Acquisition: Leverage Scenarios, Merger-Arb Spreads & Sector Re-Rating

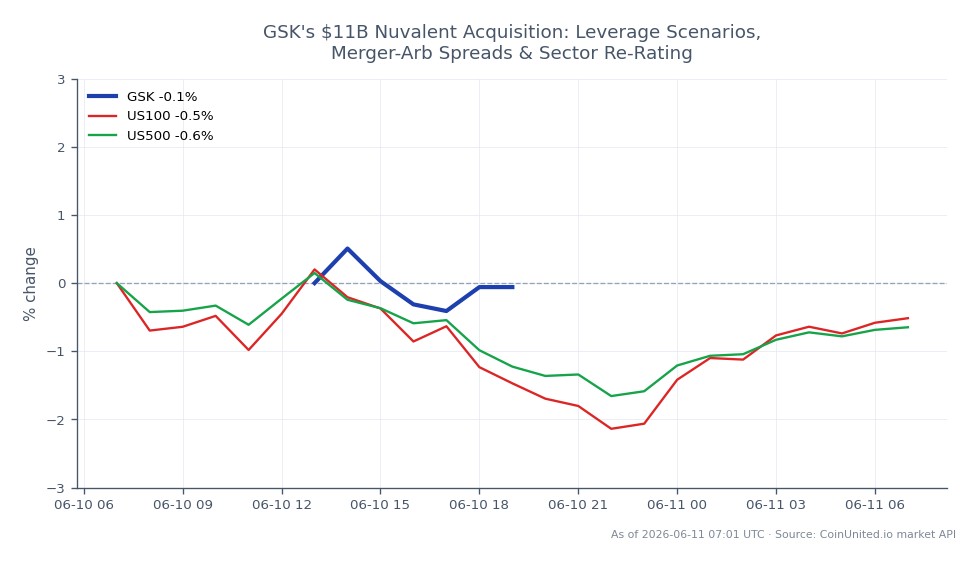

Data Snapshot

Key Takeaways

- •GSK offered $124/share (40% premium) for Nuvalent in an ~$11B all-cash deal expected to close Q3 2026 — confirmed by GSK press release and BioPharma Dive.

- •Leveraged GSK CFD traders face asymmetric risk: tight $50.98–$51.62 range today, but binary FDA read-outs (Sep & Nov 2026) could trigger 5–10% moves in either direction.

- •Nuvalent (NVAL) is now a merger-arb instrument capped near $124 — high-leverage longs above 10x face outsized downside if deal conditions deteriorate.

- •The deal reinforces the pharma M&A re-rating theme, lifting oncology biotech peer valuations and supporting a broader bid floor for late-stage targeted therapy developers.

- •S&P 500 and NASDAQ 100 impact is modest and sector-contained; no material forex or commodities spillover expected.

As reported by Reuters and BioPharma Dive, GSK plc has formally agreed to acquire Nuvalent, Inc. in an all-cash deal valued at approximately $11 billion, codenamed "Project Nashville" and announced on

Event Summary

As reported by Reuters and BioPharma Dive, GSK plc has formally agreed to acquire Nuvalent, Inc. in an all-cash deal valued at approximately $11 billion, codenamed "Project Nashville" and announced on 9 June 2026. The offer price of $124 per share represents a ~40% premium to Nuvalent's prior close and a ~26% premium to its 30-day VWAP. This is GSK's largest acquisition to date and its third M&A deal of 2026, bringing total announced 2026 deal value to ~$14 billion.

Nuvalent's pipeline centers on two late-stage FDA-reviewed lung cancer therapies: zidesamtinib (ROS1 inhibitor, PDUFA date 18 September 2026) and neladalkib (ALK inhibitor, PDUFA date 27 November 2026). GSK will fund the acquisition via new and existing debt while maintaining its credit rating, financial guidance, and dividend policy. Deal close is expected in Q3 2026.

Leverage Impact Analysis

GSK stock (current price: $51.22) reflects a modest acquirer discount — typical for large all-cash deals financed with debt. For leveraged CFD traders on CoinUnited.io, two dynamics dominate:

GSK long scenario: A trader opening a 50x long GSK CFD at $51.22 controls $2,561 in notional exposure per $51.22 margin. A 2% adverse move to ~$50.20 erases ~$102 — roughly the full margin unit. With GSK trading in a tight $50.98–$51.62 24h range, high-leverage entries face whipsaw risk ahead of deal-close confirmation and the September FDA catalyst. Position sizing below 20x is more sustainable for a multi-week hold targeting the oncology re-rating thesis.

Nuvalent merger-arb: With NVAL trading toward the $124 cash offer, the upside is capped. This is now a spread instrument — the arb trades the gap between current price and $124 against closing risk. Leveraged long positions in NVAL above 10x face asymmetric risk: limited upside to $124, but a deal break could reprice shares 30–40% lower instantly.

Monitor open interest and funding rates on CoinUnited.io for confirmation of directional conviction in GSK CFDs.

Cross-Market Impact

This deal is part of the broader pharma & fintech acquisition repricing theme and the wider M&A acquisition wave accelerating through 2026. The sector read-through is constructive for oncology-focused mid/small-cap biotechs, which may see valuation floors lift as cross-sector acquisition repricing benchmarks rise.

For the S&P 500 Index and NASDAQ 100 Index, the impact is modest and sector-specific — healthcare's weighting limits broad index spillover. However, sustained pharma M&A at ~3x peak sales multiples supports healthcare sector earnings expectations, which is a marginal positive for index sentiment. Forex and commodities are largely unaffected; any GBP/USD flow from GSK deploying USD into a US asset is immaterial relative to daily FX volumes.

Trading Considerations

GSK's key catalysts over the next six months are binary FDA decisions: zidesamtinib (18 Sep 2026) and neladalkib (27 Nov 2026). Approval of both would validate the ~3x peak sales multiple GSK paid; a rejection or delay makes the deal look expensive and could pressure shares toward the $49–$50 support zone. The 24h range of $50.98–$51.62 shows limited immediate volatility, suggesting the market has partially priced in the deal. Watch for rating-agency commentary on GSK's post-deal leverage as a secondary catalyst. Traders using the acquisition arbitrage framework should model NVAL spread against a Q3 2026 close timeline.

Trade GSK plc on CoinUnited.io

Frequently Asked Questions

GSK at $51.22 is trading in a narrow range post-announcement, so very high leverage (50x+) is exposed to whipsaw risk. The real leverage catalyst is the pair of FDA decisions in September and November 2026, which could move GSK 5–10% in either direction.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.