Quick Links

GSK in $9–10B Nuvalent Talks: Leverage Scenarios, Merger-Arb Angles & Cross-Market Read

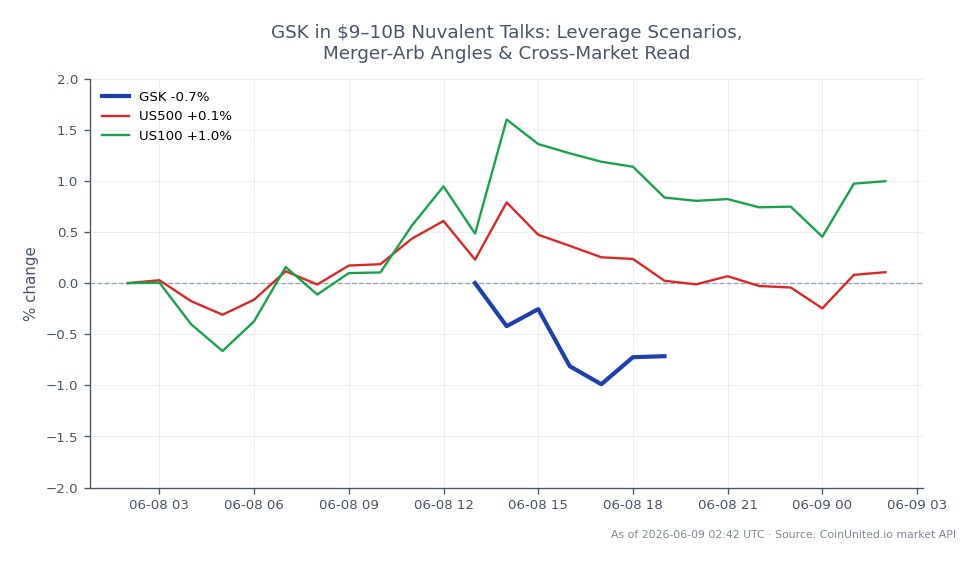

Data Snapshot

Key Takeaways

- •GSK is in unconfirmed talks to acquire Nuvalent for $9–10B (FT report) — no signed deal yet; treat as credible M&A leak with headline risk in both directions.

- •Leverage risk on GSK CFDs is asymmetric: a 50x long at $50.70 faces ~100% margin loss on a ~2% adverse move — size positions to account for acquirer de-rating and deal uncertainty.

- •NUVL is the primary event-driven vehicle; a confirmed cash offer triggers a gap-up toward the implied $9–10B valuation, but deal-break risk remains the key downside scenario.

- •Royalty Pharma (RPRX) holds royalties on Nuvalent's lead assets through 2041–2042 — a strategic buyer is a modest positive read-through for RPRX's royalty cash flows.

- •Broader oncology biotech multiples benefit from a $9–10B clinical-stage deal price — watch for sympathy moves in mid-cap TKI and targeted therapy names as the M&A acquisition wave theme reprices the sector.

According to the Financial Times, GSK plc (NYSE: GSK) is in advanced talks to acquire Nuvalent, Inc., a Massachusetts-based clinical-stage oncology company focused on precision kinase inhibitors (TKIs

Event Summary

According to the Financial Times, GSK plc (NYSE: GSK) is in advanced talks to acquire Nuvalent, Inc., a Massachusetts-based clinical-stage oncology company focused on precision kinase inhibitors (TKIs). As reported by Investing.com relaying the FT, a transaction could value Nuvalent at $9–10 billion, representing a "significant premium" to its pre-rumor market cap. No definitive agreement has been signed, and GSK's own press releases have not confirmed the deal — this remains a credible M&A leak, not a completed transaction.

GSK's strategic rationale centers on deepening its oncology franchise via Nuvalent's lead assets: neladalkib and zidesamtinib — targeted kinase inhibitors with royalty durations projected through 2041–2042 per Royalty Pharma's recent royalty acquisition. This follows GSK's broader M&A activity in 2025, including its $1.15B acquisition of IDRx, and fits the pharma & fintech acquisition repricing theme gaining momentum across global markets.

Leverage Impact Analysis

GSK CFD traders face an asymmetric setup. According to live market data, GSK is currently trading at $50.70 (24h range: $50.45–$51.39, down 1.69%). Large acquirers typically trade flat to slightly lower on premium deal announcements — a pattern consistent with GSK's current softness.

Worked example — short-term acquirer pressure: A trader with a 50x long GSK CFD opened at $50.70 controls $2,535 of notional exposure per lot. A 2% further decline to ~$49.69 (consistent with typical acquirer re-rating on a large development-stage biotech deal) would produce a ~100% loss of margin at that leverage tier. Traders holding leveraged GSK longs should note that deal uncertainty keeps headline risk elevated in both directions — a deal collapse could send GSK back toward its 24h low of $50.45, while formal confirmation with a strategic narrative could spark a recovery toward $51.39 and beyond.

Nuvalent (NUVL) — the merger-arb leg: NUVL is the primary event-driven vehicle here. A confirmed cash offer near $9–10B implies a sharp gap-up toward the implied per-share offer price. High-leverage long NUVL positions would capture the bulk of that move, but traders must size for deal-break risk: if talks collapse, NUVL could retrace substantially. This is a classic M&A acquisition wave setup where position sizing relative to deal-break probability is the core risk management variable.

Monitor open interest and funding rates on CoinUnited.io for real-time positioning signals on both names.

Cross-Market Impact

The $9–10B price tag for a clinical-stage oncology company reinforces high strategic valuations across the global acquisition & consolidation wave. Mid-cap oncology developers with differentiated TKI or targeted therapy pipelines are the clearest beneficiaries — expect sentiment lift and potential multiple expansion across biotech-heavy ETFs.

Royalty Pharma (RPRX): Holds a low-single-digit royalty on neladalkib and zidesamtinib through 2041–2042. A credible strategic buyer accelerating commercialization is a modest positive read-through for RPRX's future royalty cash flows.

Indices: GSK is a constituent of global pharma/healthcare indices. A renewed cross-sector acquisition repricing cycle in oncology supports sector multiples on the S&P 500 Index and NASDAQ 100 Index healthcare weightings, though the macro spillover is second-order.

FX/Commodities: No material GBP or commodity impact is expected — this is company-specific M&A with negligible macro transmission.

Trading Considerations

Key levels for GSK CFD traders: $50.45 (24h low / immediate support), $51.39 (24h high / near-term resistance). A confirmed deal announcement would likely test levels above $51.39; a deal collapse or negative clinical update on Nuvalent's pipeline could breach $50.45 and open a larger re-rating. For broader context on how acquisitions at this scale move markets, CoinUnited's M&A trading guide and acquisition arbitrage guide provide detailed level-setting frameworks.

This event requires immediate market confirmation — watch for any formal GSK press release or regulatory filing as the definitive trigger for directional conviction.

Trade GSK plc on CoinUnited.io

Frequently Asked Questions

GSK is trading at $50.70 and acquirers typically re-rate modestly lower on large premium deals — a 50x long CFD at current levels faces full margin loss on roughly a 2% decline. Until a definitive agreement is confirmed, headline risk cuts both ways: formal deal announcement could push above $51.39, while deal collapse risks a break below $50.45.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.