Quick Links

DRC's Strategic Mineral Designation Raises Royalties on Lithium Miners — What Leveraged Commodity Traders Must Know

Data Snapshot

Key Takeaways

- •DRC's 2018 Mining Code enables royalties up to 10% on strategic minerals, with lithium now firmly in that category — directly compressing IRR for Manono and similar projects.

- •Leveraged long positions in DRC-exposed lithium miner CFDs (ALB) face structural headwinds from the 50% super-profit tax, which caps upside in bull-market scenarios.

- •Non-DRC lithium producers (SQM, Australian peers) gain a relative cost-curve advantage — a potential CFD long divergence trade.

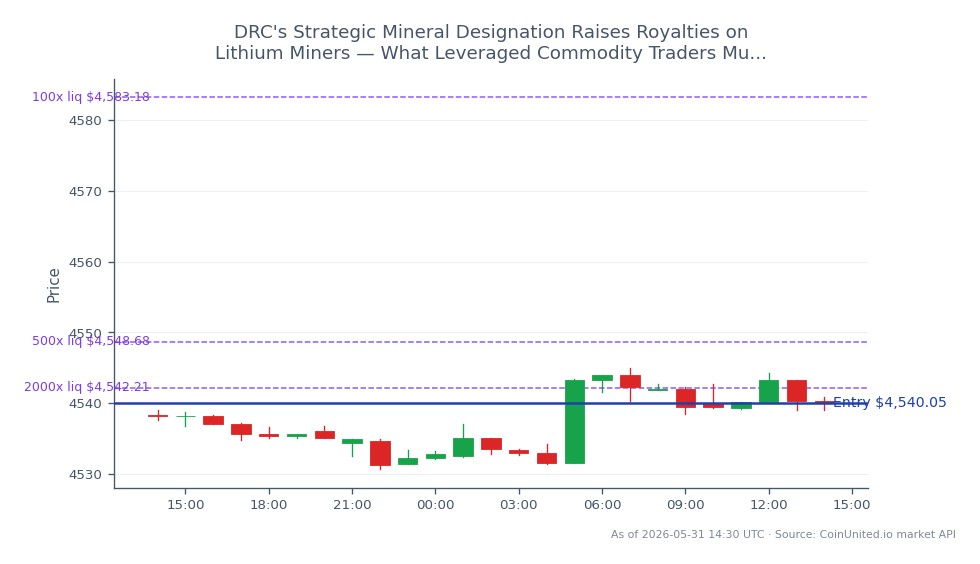

- •Gold (XAUUSD $4,540.05) receives a secondary bullish tailwind as resource-nationalism reinforces the macro inflation pressure and inflation hedge rotation narrative.

- •AUD/USD may see modest medium-term support if DRC supply constraints tighten the global lithium cost curve, benefiting Australian producers.

The Democratic Republic of Congo's 2018 Mining Code, confirmed by UNCTAD and the U.S. Department of Commerce, enables the DRC government to classify minerals as "strategic substances" — triggering roy

Event Summary

The Democratic Republic of Congo's 2018 Mining Code, confirmed by UNCTAD and the U.S. Department of Commerce, enables the DRC government to classify minerals as "strategic substances" — triggering royalty rates that can surge from standard levels to as high as 10% (the cobalt precedent), plus a 50% super-profit tax when market prices exceed feasibility-study prices by 25% or more. According to U.S. commercial guidance, lithium is now explicitly treated within this critical/strategic minerals category, with the Manono lithium project — described externally as one of the richest hard-rock lithium deposits globally — squarely in scope.

In February 2025, the DRC suspended cobalt exports for four months to address oversupply, signaling willingness to deploy both fiscal and trade levers simultaneously. A framework agreement with KoBold Metals (backed by major U.S. tech investors) to explore DRC lithium nationwide underscores the state's intent to capture maximum value from its resource base.

Leverage Impact Analysis

This event carries a medium leverage-relevance score (0.55), primarily because lithium lacks a liquid, standardized futures contract on major exchanges — direct CFD plays on lithium spot are limited. However, the ripple effects on Albemarle Corporation (ALB) and SQM equity CFDs are directly tradeable with up to 2000x leverage on CoinUnited.io.

Worked example — ALB short CFD: If ALB trades at $70 (monitor live pricing on CoinUnited), a trader entering a 50x short CFD controls $3,500 notional per $70 margin. A 5% move lower — consistent with the scale of royalty-driven cost-curve repricing seen when cobalt received strategic designation — generates $175 profit on a $70 position. However, a 2% adverse move triggers a $70 margin erosion of ~$35 (50% margin call threshold), so position sizing must account for event-driven volatility spikes.

Key risk for leveraged longs in DRC-exposed miners: The super-profit tax (50% on profits when prices exceed feasibility benchmarks by >25%) acts as a structural cap on upside leverage for miners in bull markets — precisely when leveraged long equity positions would otherwise compound gains fastest. Shorter stability clauses (5 years vs. the prior 10) increase discount-rate assumptions in DCF models, compressing forward valuations.

For indirect Gold / US Dollar positioning: rising resource-nationalism signals across DRC battery metals can reinforce the inflation hedge asset rotation thesis, providing a modest tailwind for gold CFD longs.

Cross-Market Impact

Lithium miner equities (ALB, SQM, TSLA supply chain): DRC-exposed miners face immediate equity pressure from downward IRR revisions. Non-DRC peers (Australian, Canadian, Chilean producers) gain relative cost advantage — watch SQM as a potential beneficiary CFD long.

Tesla, Inc. and EV OEMs: Higher upstream lithium costs compress battery input margins. Tesla's vertical integration partially insulates it, but sustained DRC fiscal tightening increases procurement cost risk across the sector.

Gold (XAUUSD at $4,540.05, +0.96% on session): Broader resource-nationalism and supply-side inflation from critical minerals feed the macro inflation pressure narrative that has driven gold's recent breakout above $4,500. This event is a secondary supporting factor, not a primary gold catalyst.

AUD/USD: Australia is a major lithium exporter that benefits from DRC supply-cost increases. The AUD/USD trading dynamics could see modest support if DRC supply concerns escalate, though the effect is indirect and slow-moving.

Trading Considerations

The key levels to watch are ALB and SQM equity CFD reaction to any official DRC royalty rate announcement for lithium — the cobalt precedent (2% to 10%) sets the upper bound for analogous repricing. Monitor whether KoBold Metals' Manono project timelines are revised, as delays would signal deeper regulatory risk than markets currently price.

Risk factors include implementation uncertainty (exact royalty percentage unconfirmed), DRC's track record of negotiated outcomes with large investors, and the possibility that higher royalties are partially offset by infrastructure concessions. Given XAUUSD's current level of $4,540.05 near session highs ($4,544.95), watch for any gold pullback to the $4,530 intraday support as a leveraged long re-entry context if DRC news amplifies the inflation/resource-nationalism macro theme.

Trade Gold / US Dollar on CoinUnited.io

Trade XAUUSD with up to 2000xx leverage → | Create Free Account

Frequently Asked Questions

A 50x short ALB CFD benefits if royalty increases trigger a downward IRR revision in DRC-exposed project models — but implementation risk is high since the exact lithium royalty rate is unconfirmed. Size positions to withstand 3-5% adverse swings until a concrete rate announcement is made.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.