Quick Links

Parker-Hannifin's $2.5B Circor Aerospace Deal: Leverage Scenarios & Defense Sector Ripple Effects

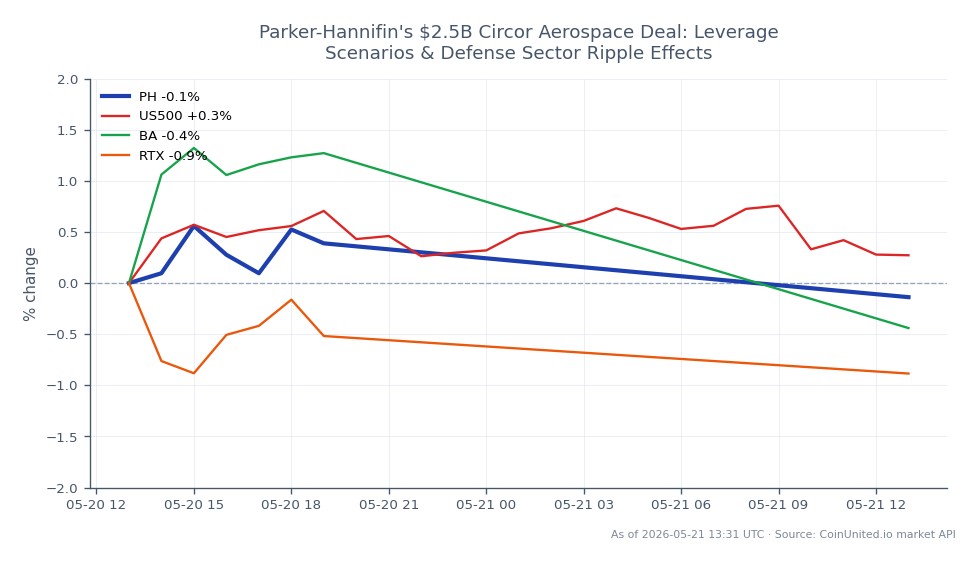

Data Snapshot

Key Takeaways

- •Parker-Hannifin (PH) is acquiring Circor's aerospace/defense unit for $2.5B — a strategic bolt-on that signals confidence in defense sector demand.

- •PH trades at $858.29 (+0.73%); leveraged long CFD positions above 100x face liquidation risk on any pullback below the $847.71 intraday low.

- •RTX Corporation and GE Aerospace are the most direct peer re-rating plays — aerospace/defense M&A typically lifts sector-wide multiples.

- •The deal reinforces the ongoing multi-sector M&A wave; S&P 500 industrials sector receives a mild positive sentiment boost.

- •Gold and forex markets are largely unaffected — this is a single-sector industrial deal with limited macro spillover.

As reported by The Wall Street Journal, Parker-Hannifin Corporation (PH) has agreed to acquire the aerospace and defense unit of Circor International for approximately $2.5 billion. The deal targets C

Event Summary

As reported by The Wall Street Journal, Parker-Hannifin Corporation (PH) has agreed to acquire the aerospace and defense unit of Circor International for approximately $2.5 billion. The deal targets Circor's high-margin aerospace/defense segment — which produces flow and motion control components for commercial and military aircraft — and represents a strategic bolt-on to Parker-Hannifin's existing Aerospace Systems segment. Parker-Hannifin trades at $858.29, up 0.73% on the day, with an intraday range of $847.71–$862.41.

This acquisition fits squarely within the ongoing M&A acquisition wave sweeping industrial and defense sectors, as large-cap industrials deploy balance sheet capacity to capture niche precision-engineering businesses at scale.

Leverage Impact Analysis

With PH at $858.29 and up 0.73% on the day, the initial market reaction is modestly bullish — typical for an acquirer on a bolt-on deal at a defined price. The key leverage risk is a post-announcement drift rather than a sharp gap.

Worked example — long CFD: A trader opening a 50x long PH CFD at $858.29 controls $42,914.50 notional per unit with ~$1,716.58 margin. A 2% move higher to ~$875.46 generates a ~$342 gain per unit — roughly a 20% return on margin. Conversely, a 2% pullback to ~$840.92 would erode the same margin by ~20%, and positions above 100x leverage face liquidation risk on any intraday retest of the $847.71 low.

Downside scenario: Acquirers historically underperform in the 5–10 sessions post-announcement as integration risk is priced. Traders holding leveraged longs should note that a break below $847.71 (today's low) would signal short-term rejection of the deal premium. The broader cross-sector acquisition repricing dynamic suggests peer stocks (RTX, GE Aerospace) may reprice faster than PH itself.

Monitor open interest and funding rates on CoinUnited.io for confirmation of directional conviction before adding leverage.

Cross-Market Impact

This deal amplifies the multi-sector M&A deal surge already visible across industrials. Key cross-market reads:

- -RTX Corporation and GE Aerospace: Both are direct aerospace/defense peers. RTX and GE Aerospace CFD traders should watch for sympathy repricing — consolidation deals signal pricing power and sector confidence, often lifting peer valuations.

- -The Boeing Company: As a major end-customer for flow-control components, Boeing's supply chain visibility improves marginally — mild positive read-through.

- -S&P 500 Index: Large industrial M&A is a risk-on signal for the broader index. Industrials carry ~8.5% weight in the S&P 500, and deal activity supports sector multiples.

- -Gold: Defense spending-linked M&A is not a direct gold catalyst. Gold remains driven by macro/rate factors — this deal has negligible commodity impact.

- -Howmet Aerospace Inc.: As a precision aerospace components peer, Howmet is the most direct read-through target for acquisition premium repricing.

Trading Considerations

Key levels for PH CFD traders: immediate support at $847.71 (today's low); resistance at $862.41 (today's high). A confirmed hold above $858 on volume would suggest the market is pricing deal accretion positively. Watch for any analyst price-target revisions in the next 24–48 hours as the street models the $2.5B purchase price against Parker-Hannifin's balance sheet capacity.

For traders interested in acquisition arbitrage strategies, the Circor aerospace unit is private — the direct arbitrage play sits in PH CFDs and aerospace peers, not a listed Circor spread.

Trade Parker-Hannifin Corporation on CoinUnited.io

Frequently Asked Questions

At $858.29 entry with 50x leverage, a 2% upside move to ~$875 returns ~20% on margin, while a 2% pullback to ~$841 wipes the same amount — positions above 100x are vulnerable to liquidation on a retest of today's $847.71 low.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.