Quick Links

KKR & Energy Capital Partners Eye Sweetened Bid for DCC After £58/Share Rejection

Data Snapshot

Key Takeaways

- •DCC's board unanimously rejected a £58.00/share (£4.95–5.0bn) cash bid from KKR and ECP on 29 April 2026, calling it a fundamental undervaluation.

- •Bloomberg reports KKR/ECP are weighing a higher offer — the Irish Takeover Panel's 'put up or shut up' deadline is 10 June 2026.

- •DCC spiked to ~6,235–6,245p on confirmation, well above the 5,800p offer, with 5,800p now acting as a hard valuation floor.

- •Cantor Fitzgerald Ireland's 7,070p price target provides a ceiling reference if a deal is struck at a material premium.

- •Even without a deal, the public PE endorsement of DCC's value may catalyze management action such as buybacks or portfolio restructuring.

As reported by Bloomberg and confirmed across multiple outlets including The Irish Times and MarketScreener, DCC plc — the London-listed, Dublin-based energy distribution and marketing group — unanimo

Event Analysis

As reported by Bloomberg and confirmed across multiple outlets including The Irish Times and MarketScreener, DCC plc — the London-listed, Dublin-based energy distribution and marketing group — unanimously rejected a £58.00 per share (5,800 pence) all-cash takeover proposal from a consortium of KKR & Co and Energy Capital Partners (ECP) on 29 April 2026. The bid valued DCC at approximately £4.95–£5.0 billion, yet the board stated the offer "fundamentally undervalues the company and its future prospects." Bloomberg subsequently reported that KKR and ECP are weighing a higher counter-proposal — making this a live, event-driven situation with a clearly defined regulatory deadline.

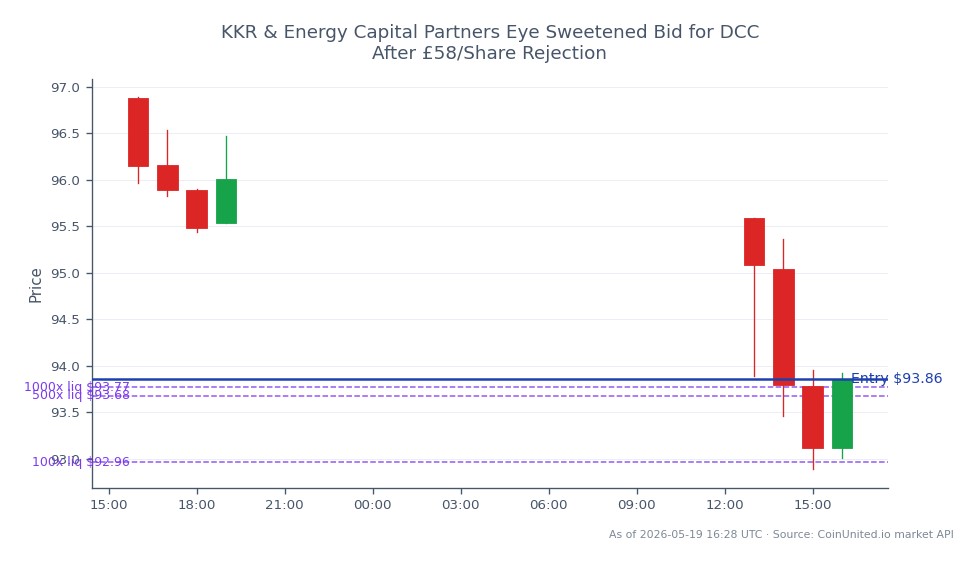

What makes this event significant is the hard deadline now in play. Under Irish Takeover Panel rules, the consortium must either announce a firm intention to bid or walk away by 10 June 2026 — a classic "put up or shut up" clock. This compresses the timeline for any price discovery and creates a binary event window for traders. The rejected offer itself now serves as a public valuation floor, and the market's immediate spike to ~6,235–6,245 pence signals that investors are pricing in a higher bid well above 5,800p.

This deal fits squarely within the broader M&A acquisition wave theme of global private equity targeting listed European corporates perceived as undervalued relative to their cash-generative assets. DCC's energy distribution and logistics model — steady volumes, durable margins — is precisely the type of infrastructure-adjacent business attracting USD-funded PE capital. Even if this specific bid fails, the public endorsement of DCC's value at these levels could catalyze a strategic rethink from management, including buybacks or a portfolio restructuring. The cross-sector acquisition repricing theme is clearly active here.

For context, Cantor Fitzgerald Ireland maintains an Overweight rating with a 7,070p price target on DCC — meaningfully above both the rejected offer and the current trading range. This analyst conviction, combined with the board's confident rejection language, suggests there is a credible gap between the bid price and what management believes the business is worth on a standalone basis.

What This Means for Traders

DCC is now a textbook acquisition arbitrage setup with three distinct scenarios before June 10: (1) KKR/ECP returns with a higher offer, pushing DCC toward or above the 6,235p reaction high; (2) a competing strategic or PE bidder emerges, potentially triggering a bidding war; or (3) no firm offer materializes and the M&A premium deflates toward fundamental-only value. Traders should treat 5,800p as a hard floor reference and the ~6,235p level as near-term resistance reflecting peak bid speculation. The Cantor Fitzgerald 7,070p target provides a ceiling scenario if a deal is struck at a significant premium.

Volatility in DCC will remain elevated through the June 10 deadline and should be treated as binary-event risk. Any RNS filing or Bloomberg/FT leak of a revised price level is a potential catalyst for sharp moves in either direction. For those following the broader M&A wave trading cycle, DCC is a high-conviction event-driven name with unusually clear milestones. KKR's own equity (NYSE: KKR) is unlikely to move materially on this deal given its scale relative to KKR's overall AUM, but confirmed deal completion could provide marginal sentiment support.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

Under Irish Takeover Panel rules, KKR/ECP must announce a firm intention to bid or walk away by 10 June 2026. If they walk away, they are typically barred from re-bidding for 12 months — making this deadline a hard catalyst for price action.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.