Quick Links

ConvaTec Organic Revenue Miss Sends CTEC Shares Down 7%: What Med-Tech Traders Need to Know

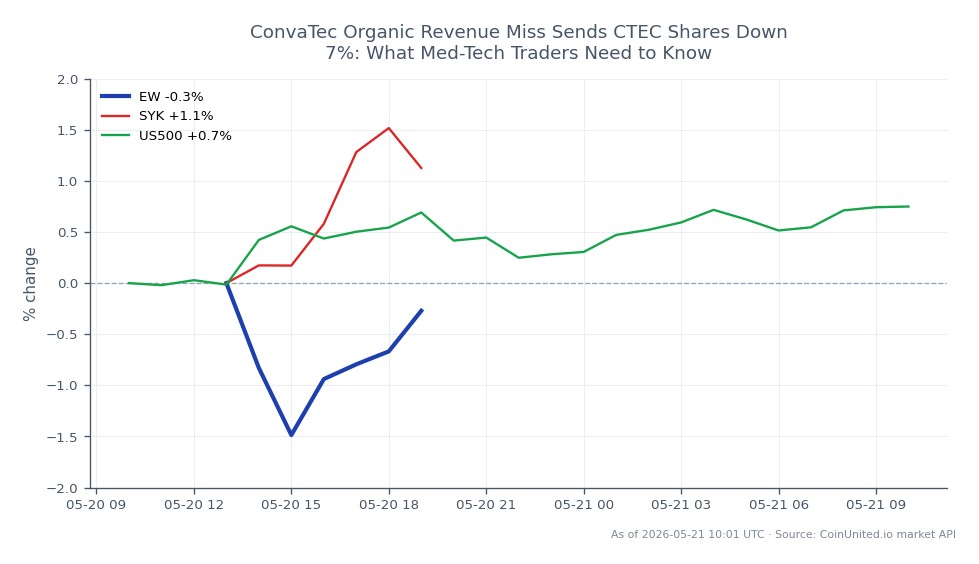

Data Snapshot

Key Takeaways

- •ConvaTec FY2025 revenue of ~$2.44bn grew 6.5% reported, but organic growth lagged consensus expectations, triggering an approximately 7% selloff in CTEC shares.

- •Management raised the medium-term organic growth target to 6–8% from 2027, but near-term execution credibility is now the market's focus.

- •The selloff is primarily idiosyncratic — macro, FX, crypto, and commodity markets are not meaningfully affected.

- •Watch for sympathy moves in adjacent med-tech peers if management cites broad hospital procurement headwinds rather than company-specific issues.

- •A 7% drawdown in a premium-valued compounder can attract long-only buyers if the growth thesis remains intact — monitor volume and support levels for reversal signals.

ConvaTec Group PLC (LSE: CTEC), the FTSE 100 wound care and ostomy specialist, saw its shares tumble approximately 7% after reported organic revenue growth came in below market expectations. According

Event Analysis

ConvaTec Group PLC (LSE: CTEC), the FTSE 100 wound care and ostomy specialist, saw its shares tumble approximately 7% after reported organic revenue growth came in below market expectations. According to data from the London Stock Exchange and AJ Bell, ConvaTec's FY2025 results showed total revenue of approximately $2.44 billion — up 6.5% on a reported basis — with adjusted operating profit of $544 million, up 12.1%. While the headline numbers appear solid, the selloff signals that consensus had been positioned for organic growth toward the upper end of the company's 5–7% guidance range, and the delivered figure disappointed.

The magnitude of the reaction reflects ConvaTec's valuation premium. As noted by Simply Wall St., analyst forecasts had priced in roughly 20% EPS growth per annum and ~6.1% annual revenue growth, implying the market expected consistent delivery at the high end of guidance. Missing that bar — even narrowly — triggers an earnings miss revenue shock de-rating for growth-oriented healthcare names. Management did reiterate 2026 guidance of 5–7% organic growth (ex-InnovaMatrix) and raised the medium-term target from 5–7% to 6–8% from 2027 (per AJ Bell and London Stock Exchange filings), but near-term execution credibility is now under scrutiny.

This event is particularly significant because ConvaTec had recently been repositioned as a defensive compounder — a rare combination of steady healthcare demand and improving margins. Any crack in the growth narrative matters disproportionately. The explicit carve-out of InnovaMatrix from organic growth metrics also raises questions about the underlying quality of the core business trajectory, which analysts will probe heavily on the earnings call.

What This Means for Traders

For single-stock traders, the immediate question is whether this is a one-off execution stumble or the start of a structural deceleration. If management's 6–8% medium-term target remains credible, the 7% drawdown could represent a valuation reset that long-only institutional buyers step into — making CTEC a potential earnings miss recovery play over a 4–8 week horizon. However, if the call reveals demand headwinds in hospital procurement or geographic softness, the de-rating could extend. Traders should watch for volume profile confirmation — whether selling exhausts intraday or continues into the close.

For sector and index traders, the read-through matters selectively. Edwards Lifesciences Corporation and Stryker Corporation operate in adjacent med-tech segments, and any ConvaTec commentary about broader hospital budget constraints would create sympathy pressure on those names. The S&P 500 Index impact is negligible given CTEC's weight, but European healthcare ETFs and FTSE 350 Healthcare sector funds face marginal drag. This event fits the broader pattern outlined in our earnings miss sector strategies guide — idiosyncratic misses in premium-valued defensive growers tend to see sharp initial drops followed by stabilisation once selling exhausts, unless macro headwinds are confirmed.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

It depends on whether the miss is company-specific (execution, timing) or reflects broader demand weakness — listen for management commentary on hospital volumes and pricing dynamics on the earnings call. If the 6–8% medium-term target is reaffirmed credibly, the drop could be a valuation entry point.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.