Quick Links

Five Below Raises FY26 Guidance Above Consensus: $5.4B–$5.48B Revenue, +6–8% Comps, $8.85 EPS Midpoint

Data Snapshot

Key Takeaways

- •Five Below raised FY26 revenue guidance to $5.4B–$5.48B, above Street consensus of ~$5.36B, with comp sales guidance nearly doubling to +6–8%.

- •Adjusted EPS midpoint of ~$8.85 represents a double-digit percentage upgrade vs. prior guidance range of $7.74–$8.25.

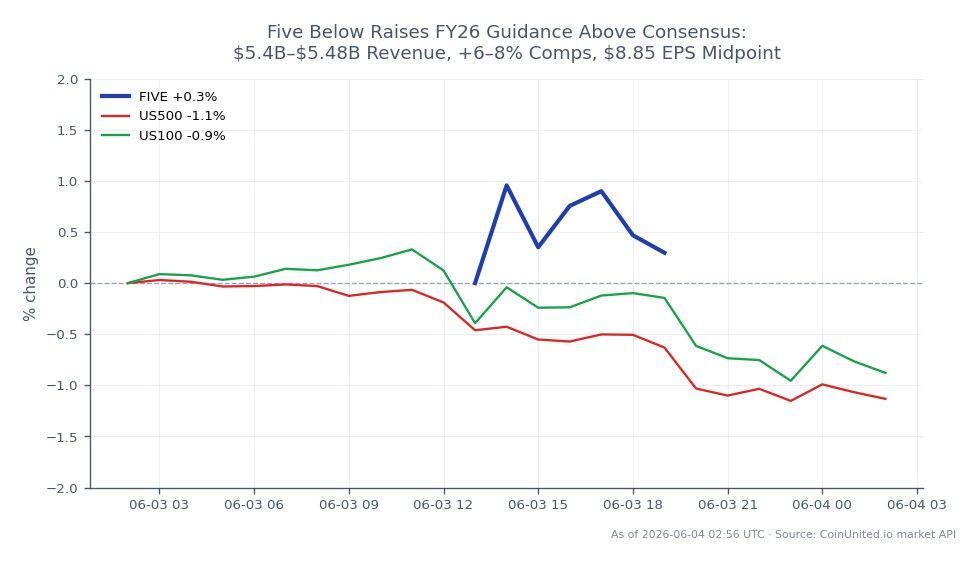

- •FIVE trading at $223.06 (+1.11%) with the stock already above the prior analyst consensus target — near-term upside depends on analyst model revisions.

- •Strong comp sales inflection signals genuine same-store demand strength, not just expansion-driven growth — a higher-quality earnings signal.

- •Positive read-through for US value/discount retail sector; modest supportive signal for consumer discretionary indices exposure.

Five Below, Inc. (FIVE) delivered a significant guidance upgrade following a strong Q1, raising its FY26 revenue outlook to $5.4B–$5.48B (from $5.2B–$5.3B), comparable sales growth guidance to +6–8% (

Event Analysis

Five Below, Inc. (FIVE) delivered a significant guidance upgrade following a strong Q1, raising its FY26 revenue outlook to $5.4B–$5.48B (from $5.2B–$5.3B), comparable sales growth guidance to +6–8% (from +3–5%), and adjusted EPS guidance to $8.65–$9.05 (from $7.74–$8.25), according to reporting via TipRanks and StockAnalysis. The EPS midpoint of approximately $8.85 lands above the prior consensus range and implies a double-digit percentage earnings upgrade — a rare trifecta of revenue, comp, and profit upgrades in a single print.

Critically, the new revenue range sits above Street consensus of ~$5.36B, which means analysts are likely to revise models upward. With 18 analysts currently rating FIVE a Buy, this guidance beat has the characteristics of a catalyst that accelerates re-rating rather than simply confirming existing targets. The comp sales inflection — doubling the growth floor from +3% to +6% — signals genuine demand momentum, not just cost engineering.

This event fits squarely within the broader Q1 Earnings Beat & Outlook Upgrade Wave playing out across sectors in 2026. What makes FIVE's upgrade notable is its read-through value: a discount specialty retailer raising comps this aggressively suggests the US value consumer remains structurally active. This is different from past Five Below beats that were driven by store-count expansion — this cycle points to same-store demand strength, which carries higher-quality earnings multiple implications. For broader context on navigating these setups, see the 2026 Stocks Market Outlook.

What This Means for Traders

FIVE is trading at $223.06 (24h range: $219.23–$225.68), up +1.11% at the time of this report — suggesting the market has begun pricing the news but may not have fully absorbed the magnitude of the guidance revision. The analyst 12-month consensus target of approximately $148.41 implies the stock has already significantly rerated above prior models, meaning near-term price action will depend on how quickly analysts revise targets upward to reflect the new EPS midpoint of $8.85. Traders should watch for a wave of analyst upgrades and price target increases as the primary near-term catalyst.

From a sector read-through perspective, strong comps from a value-format retailer are a positive signal for consumer, industrial & energy earnings beat positioning. Discount retail strength can indicate trade-down behavior benefiting the broader value retail segment — a theme that matters for anyone holding consumer discretionary exposure in the S&P 500 Index or NASDAQ 100 Index. Those interested in the mechanics of trading these events can reference the guide on how to trade earnings beats.

Volatility outlook for FIVE is moderate-to-elevated near-term as analyst revisions land. The core risk to the long thesis: the stock has already moved well above the prior consensus target, so any macro deterioration in consumer spending could reset multiple expansion quickly. Monitor open interest and options flow on FIVE for confirmation of institutional follow-through.

Trade Five Below, Inc. on CoinUnited.io

Trade FIVE with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

The $148.41 figure reflects pre-announcement models that haven't yet absorbed the new EPS and revenue guidance. Expect a wave of analyst target upgrades that will likely close much of that gap — the key question is where revised targets land relative to current price.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.