Quick Links

BP's Failed £2B North Sea Asset Sale to Ithaca Energy: What the Collapsed Talks Mean for Energy Traders

Data Snapshot

Key Takeaways

- •BP held advanced but now-collapsed talks to sell ~£2B ($2.69B) of UK North Sea assets to Ithaca Energy, per the Financial Times — no deal confirmed by either company.

- •BP is still pursuing alternative buyers, keeping its divestment program on track; this is a delay, not a strategic reversal.

- •Ithaca Energy carried the highest event risk — a deal this size would have been transformational for the mid-cap operator.

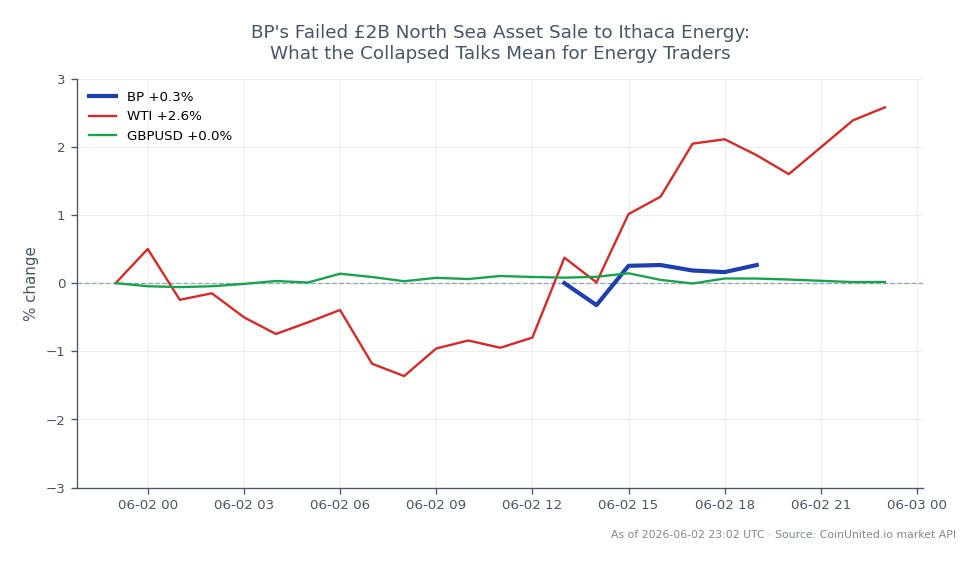

- •BP stock trades at $43.44 (+1.16%) per live data; the collapsed talks are a neutral-to-modest-negative near-term signal, pending new buyer confirmation.

- •North Sea sector peers and service companies may see sentiment spillover as BP's motivated-seller status becomes clearer to the market.

According to the Financial Times, BP held advanced talks to sell approximately £2 billion (~$2.69 billion) worth of UK North Sea upstream oil and gas assets to Ithaca Energy — a mid-cap North Sea prod

Event Analysis

According to the Financial Times, BP held advanced talks to sell approximately £2 billion (~$2.69 billion) worth of UK North Sea upstream oil and gas assets to Ithaca Energy — a mid-cap North Sea producer. As reported by Reuters, which could not independently verify the FT's account, negotiations collapsed in recent weeks, though BP is reportedly still exploring alternative buyers. No binding agreement has been announced by either company, making this a partially verified, market-moving media report rather than a confirmed transaction.

The strategic context matters here. BP has been executing a broader divestment program aimed at reshaping its portfolio, and North Sea assets have been a natural candidate given the UK's evolving energy tax environment and BP's push to rebalance upstream exposure. A £2 billion disposal is not routine — it represents a material portfolio shift that would free up capital for deleveraging, shareholder returns, or lower-carbon investments. The fact that talks reached an advanced stage before collapsing signals genuine intent on BP's part to exit these assets, even if this particular counterparty didn't work out.

For Ithaca Energy, a deal of this scale would have been transformational. As a mid-cap North Sea operator, absorbing £2 billion in assets would significantly alter its reserve base, production profile, and leverage metrics. The breakdown likely reflects disagreements over valuation, financing structure, or due diligence findings — all common friction points in upstream M&A. The energy, pharma & tech acquisition wave context is relevant: North Sea consolidation has been accelerating, and BP's willingness to engage signals that further asset sales to other bidders remain on the table as part of the broader global acquisition & consolidation wave.

For the wider UK Continental Shelf sector, the report acts as a price discovery signal. Other North Sea operators and private equity buyers now know BP is a motivated seller, which could catalyze competitive bidding and reprice comparable assets across the basin.

What This Means for Traders

BP stock (currently trading at $43.44, up +1.16% on the day according to live market data) faces a neutral-to-modest-negative read from this specific headline — collapsed talks remove a near-term catalyst that could have accelerated the divestment program and boosted cash returns. However, BP's continued pursuit of alternative buyers means the strategic narrative remains intact; this is a delay, not an abandonment. Traders should watch for any formal BP announcement or updated divestment guidance as the more actionable catalyst. The 2026 Stocks Market Outlook remains the broader frame for positioning in major energy equities.

Ithaca Energy is the higher-beta play here. If the deal is revived or a rival bid emerges, Ithaca shares could move sharply given the transformational scale of the potential acquisition relative to its market cap. Conversely, if BP sells to a third party, Ithaca loses a growth catalyst. Traders interested in UK energy sector M&A dynamics can also monitor WTI Light Crude Oil as a broader sector sentiment indicator — though this deal alone is unlikely to move crude benchmarks materially.

Cross-market spillover to GBP/USD is minimal. This is primarily an equity and sector story. Volatility on BP CFDs may remain elevated near-term as the market awaits confirmation of BP's next divestment move, making it a watch-and-confirm setup rather than an immediate directional trade.

Trade BP p.l.c. on CoinUnited.io

Frequently Asked Questions

Neither company has publicly stated a reason. Common deal-breakers in upstream M&A include valuation gaps, financing structure disagreements, or due diligence concerns over reserve quality or decommissioning liabilities.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.