Quick Links

Marvell Targets $16.5B FY2028 Revenue With $1B Capacity Prepayments and Expanded NVIDIA Tie-Up — What Leveraged Traders Must Know

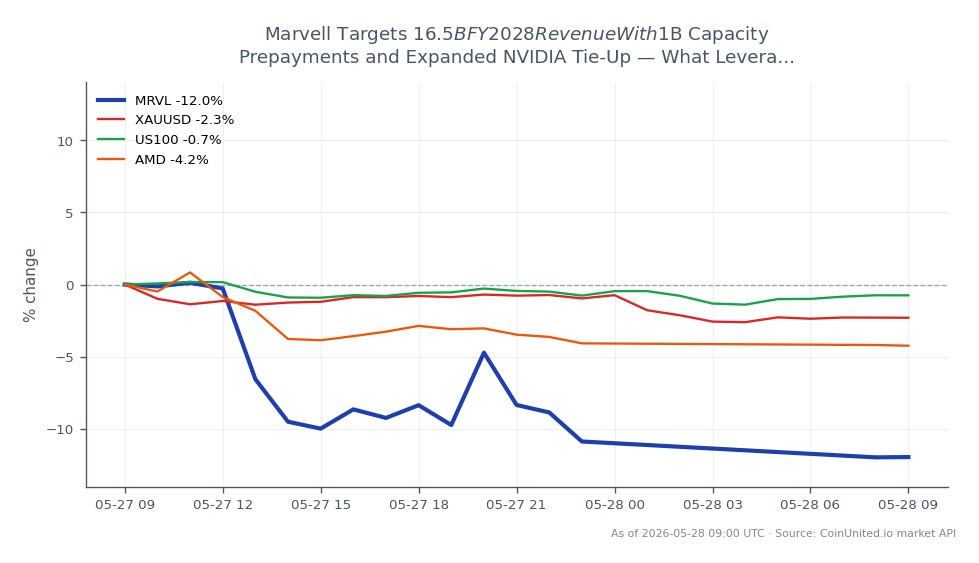

Data Snapshot

Key Takeaways

- •Marvell raised FY2028 revenue guidance to ~$16.5B — a ~10% uplift vs the prior ~$15B target — driven by 40%+ data-center growth, >50% interconnect expansion, and deepened NVIDIA NVLink Fusion integration.

- •Leverage risk is elevated: MRVL's 24h range of $192.83–$197.62 means a 50x long CFD at $193.83 sits less than 0.5% above its intraday low — reduce position size to survive volatility without forced liquidation.

- •TSMC is the strongest cross-market read-through: $1B in capacity prepayments signals high-confidence demand for leading-edge nodes, directly improving foundry utilization visibility.

- •NVIDIA benefits structurally from the partnership expansion — deeper ecosystem integration with custom XPU partners reinforces platform moat and supports NVDA CFD longs.

- •The ~10% guidance raise above prior estimates is the true alpha: markets were modeling ~$15B FY2028; repricing to $16.5B feeds EPS estimate upgrades, but watch for 'confirmation vs. surprise' dynamics if the stock fails to reclaim $197+ on volume.

Marvell Technology has raised its fiscal 2028 revenue target to approximately $16.5B, up from a prior guidance of ~$15B, representing a further ~10% uplift versus earlier long-term estimates, accordin

Event Summary

Marvell Technology has raised its fiscal 2028 revenue target to approximately $16.5B, up from a prior guidance of ~$15B, representing a further ~10% uplift versus earlier long-term estimates, according to Reuters/Refinitiv-confirmed management guidance. The company also disclosed roughly $1B in capacity prepayments to secure foundry and advanced packaging supply, and announced an expansion of its partnership with NVIDIA (NVDA) — building on NVIDIA's prior $2B commitment made March 31 to integrate Marvell's custom XPUs into the NVLink Fusion ecosystem.

The growth roadmap is steep: FY2026 data-center revenue grew ~46% YoY and represented ~74% of Q4 FY26 revenue. Management guides FY2027 total revenue at ~$11B (>30% growth), with data-center up ~40%, interconnect growing >50%, and custom silicon — already at a $1.5B annual run-rate — growing >20%. The FY2028 target of $16.5B implies 50%+ cumulative growth from FY2027 guidance, anchored by multi-year design wins inside NVIDIA's AI stack. This event aligns with the broader AI revenue monetization and chip demand surge wave reshaping semiconductor valuations.

Leverage Impact Analysis

MRVL is trading at $193.83 (24h range: $192.83–$197.62, -1.13%) at time of writing. The guidance raise is a material positive catalyst, but the stock's -1.13% drift suggests some sell-the-news pressure or prior pricing-in of AI optimism.

Worked example — Long CFD at 50x leverage: A trader opening a 50x long MRVL CFD at $193.83 controls $9,691.50 of notional per $193.83 margin. A 5% move to ~$203.52 returns +250% on margin. However, a -2% adverse move to ~$190 triggers a -100% margin loss at 50x — the 24h low of $192.83 is already within ~0.5% of the current price, meaning intraday wicks alone can stress high-leverage longs.

Liquidation risk: At 100x leverage, a move of just -1% (~$1.94) from entry wipes the position. Given MRVL's history of 18%+ intraday swings on earnings catalysts (as seen May 27), traders holding high-leverage positions through guidance events face acute liquidation cascade risk. Post-catalyst consolidation phases often see algorithmic stop-hunting below round numbers — watch $190 and $185 as key structural levels.

For strategic corporate partnerships plays like this, position sizing is critical: consider reducing leverage to 10x–20x to withstand 5–10% volatility without forced liquidation.

Cross-Market Impact

NVIDIA (NVDA): The expanded NVLink Fusion integration with Marvell reinforces NVIDIA's platform moat. Bullish read-through for NVDA CFD longs — deeper ecosystem lock-in supports sustained AI capex. Traders can reference our NVIDIA stock guide for key levels.

AMD: The Marvell-NVIDIA deepening partnership marginally pressures Advanced Micro Devices as a competing custom silicon/accelerator vendor — though AMD's own hyperscaler design wins provide a partial offset. See our AMD AI chip trading guide for context.

TSMC: The $1B capacity prepayment is a direct bullish signal for Taiwan Semiconductor Manufacturing — prepayments of this scale typically target leading-edge nodes and advanced packaging, improving TSMC's utilization visibility.

NASDAQ 100 (US100): MRVL is a constituent; sustained AI semi guidance upgrades contribute to index-level support. The NASDAQ 100 benefits from the narrative that AI capex remains a multi-year structural cycle, as detailed in our 2026 indices outlook.

Gold/Commodities: This is a micro/sector event with minimal direct macro spillover. Risk-on AI momentum modestly reduces safe-haven flows into gold in the near term.

Trading Considerations

Key levels for MRVL: immediate support at $192.83 (24h low) and $190 psychological; resistance at $197.62 (24h high) and the prior post-earnings high. A clean break above $197.62 on volume would confirm the guidance uplift is being repriced rather than absorbed. Monitor whether the stock reclaims $195+ in the next session — failure to do so suggests the ~10% guidance raise above prior $15B estimates is already discounted.

The $1B prepayment introduces execution risk: if AI hyperscaler spending normalizes before FY2028, these committed costs could pressure free cash flow. Watch quarterly data-center revenue growth rates as the leading indicator — deceleration below 35% YoY would be an early warning signal for this thesis. The cross-sector partnership catalyst theme has historically sustained 2–4 week momentum before mean-reversion; position duration matters as much as direction.

Trade Marvell Technology, Inc. on CoinUnited.io

Trade MRVL with up to 600xx leverage → | Create Free Account

Frequently Asked Questions

At $193.83 with a 24h low of $192.83, a 50x long CFD sits just ~0.5% above its intraday floor — a single wick below $192 could trigger liquidations at extreme leverage. Traders should size positions to withstand at least a 5% drawdown, implying maximum practical leverage of 20x for this setup.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.