Quick Links

Snowflake Q1 FY27 Earnings Beat: 34% Revenue Growth Signals AI Data Layer Re-Acceleration — Leverage Scenarios

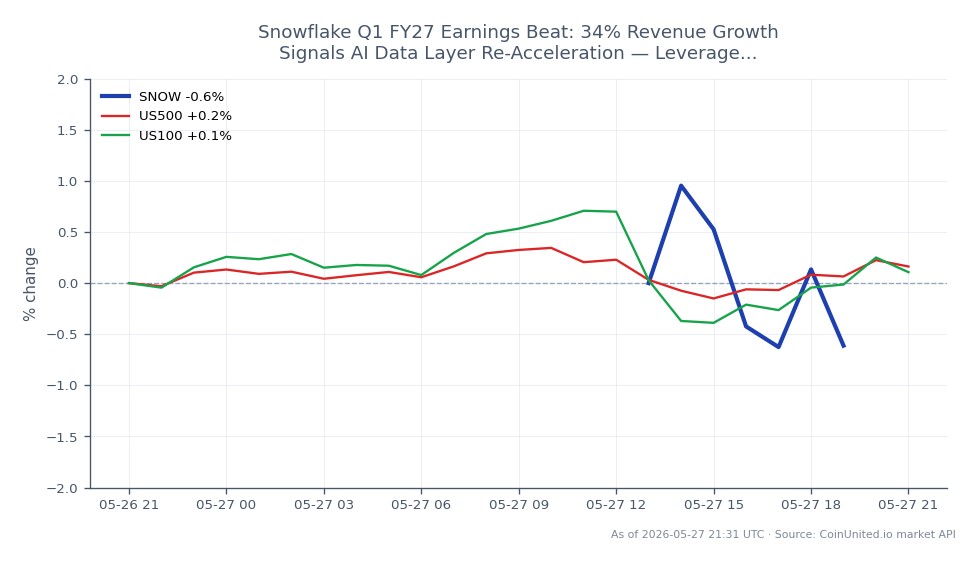

Data Snapshot

Key Takeaways

- •SNOW reported ~34% YoY revenue growth in Q1 FY27, accelerating from +26% in Q1 FY26 — a re-acceleration signal that markets price as a premium multiple expansion catalyst.

- •Leverage risk is asymmetric around earnings: a 50x long SNOW CFD at $174.63 faces liquidation at ~$171.13 — within normal after-hours spread widening — requiring disciplined position sizing.

- •CoinUnited.io's 24/7 SNOW CFD trading allows immediate positioning on the after-hours print, bypassing the NYSE open delay where up to 80% of post-earnings price discovery already occurs.

- •Cross-market read-through is positive for AI-cloud software peers (Microsoft, Alphabet, Oracle) and adds upward pressure on NASDAQ 100 and S&P 500 tech weightings.

- •Guidance is the decisive variable: a beat-and-raise sustains momentum; a beat with a cautious FY27 outlook risks a classic gap-and-fade in high-multiple software.

Snowflake Inc. (SNOW, NYSE) reported Q1 FY2027 results after the U.S. market close on May 27, 2026, with a conference call at 2 p.m. PT / 5 p.m. ET. According to the earnings release, the company post

Event Summary

Snowflake Inc. (SNOW, NYSE) reported Q1 FY2027 results after the U.S. market close on May 27, 2026, with a conference call at 2 p.m. PT / 5 p.m. ET. According to the earnings release, the company posted revenue growth of approximately 34% year-over-year — a meaningful acceleration from the +26% YoY reported in Q1 FY2026 — alongside roughly 616 customer additions and a beat versus analyst consensus on both revenue and EPS. For context, Snowflake's Q4 FY2026 print showed $1.28bn in revenue versus a $1.25bn consensus estimate, with EPS of $0.32 against a $0.27 consensus. The Q1 FY27 results represent a continuation of that beat cadence, with the added signal of re-accelerating top-line growth. As reported by Snowflake's investor relations, the company's prior net revenue retention rate stood at 124%, and markets will closely watch whether this metric held or improved in the new print.

The critical forward variable is guidance: for high-multiple software names, a beat-and-raise on full-year product revenue and operating margin typically drives sustained post-earnings momentum. Any commentary around AI-native workloads, Snowflake Native Apps, or data marketplace consumption will be scrutinized as evidence that enterprise AI spend is flowing into the data layer — not just semiconductors.

Leverage Impact Analysis

SNOW entered the earnings print at $174.63, with a 24-hour range of $173.18–$179.06 and a modest -1.59% pre-print drift. Post-earnings gap-ups on beat-and-raise prints in high-growth software typically range from 8–15% intraday.

Worked example — Long CFD: A trader opening a 50x long SNOW CFD at $174.63 controls $8,731.50 of notional per contract. A 10% post-earnings gap to ~$192 generates ~$873 profit on a ~$175 margin outlay — a ~499% return on margin. However, a 2% adverse move to ~$171 triggers a ~100% margin loss, underscoring that post-earnings gaps can move against position direction if guidance disappoints.

Liquidation risk: With 50x leverage, the liquidation threshold sits approximately 2% below entry (~$171.13). Traders holding leveraged longs through the print must size accordingly. Using higher leverage (100x+) compresses that buffer to under 1% — well within normal after-hours spread widening on earnings nights.

Since SNOW CFDs on CoinUnited.io trade 24/7, traders can respond to the after-hours earnings release immediately — without waiting for NYSE's 9:30 a.m. ET open. This structural edge matters when the largest price discovery window is the first 30–60 minutes post-release. Monitor open interest for confirmation of directional conviction before sizing up.

Cross-Market Impact

A SNOW growth re-acceleration has clear read-through across the AI-Cloud Enterprise Embedding Wave theme. Peer software names in data analytics and AI infrastructure — including Microsoft Corp., Alphabet Inc (Google), and Oracle Corporation — are likely to see sympathetic bid as the print validates enterprise AI data-layer spending. The broader AI Infrastructure Capital Reallocation narrative is reinforced when consumption-based data platforms show accelerating revenue.

At the index level, SNOW's weighting in the NASDAQ 100 Index and S&P 500 Index means a 10%+ gap-up adds marginal upward pressure on both benchmarks, particularly within the Information Technology sector weighting. Growth-factor ETFs holding SNOW as a constituent will see NAV support.

Cross-asset spillover is limited but non-zero: a strong AI software print reinforces risk-on sentiment, mildly pressuring safe-haven flows (USTs, JPY, CHF) while supporting pro-cyclical positioning. For traders watching earnings beat sector playbooks, software re-acceleration can catalyze rotation into high-growth tech from defensives.

Trading Considerations

Key levels to monitor: immediate support at the 24h low of $173.18 and pre-print resistance at $179.06. A confirmed post-earnings gap above $179 opens the path toward prior highs; failure to hold $173 on any gap-fade scenario would signal sell-the-news dynamics. Volume profile and guidance tone — particularly FY27 full-year product revenue guidance and any revision to operating margin — will determine whether the gap sustains or fades intraday.

The primary risk factor is a beat on the quarter paired with cautious forward guidance, which historically produces gap-and-fade patterns in high-multiple software. Traders should also watch NRR: if net revenue retention slips meaningfully below 120%, the consumption-growth thesis weakens regardless of the headline beat.

Trade Snowflake Inc. on CoinUnited.io

Trade SNOW with up to 800xx leverage → | Create Free Account

Frequently Asked Questions

Post-earnings gap risk on software stocks commonly exceeds 8–12%, so leverage above 10–20x materially compresses the margin buffer against adverse moves. At 50x, the liquidation threshold is approximately 2% below entry ($171.13 on a $174.63 open) — well within realistic gap-fade territory if guidance disappoints.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.