Quick Links

Germany Launches Uniper Sale Process: €18bn Supply Overhang, Equinor M&A Risk & Leverage Scenarios

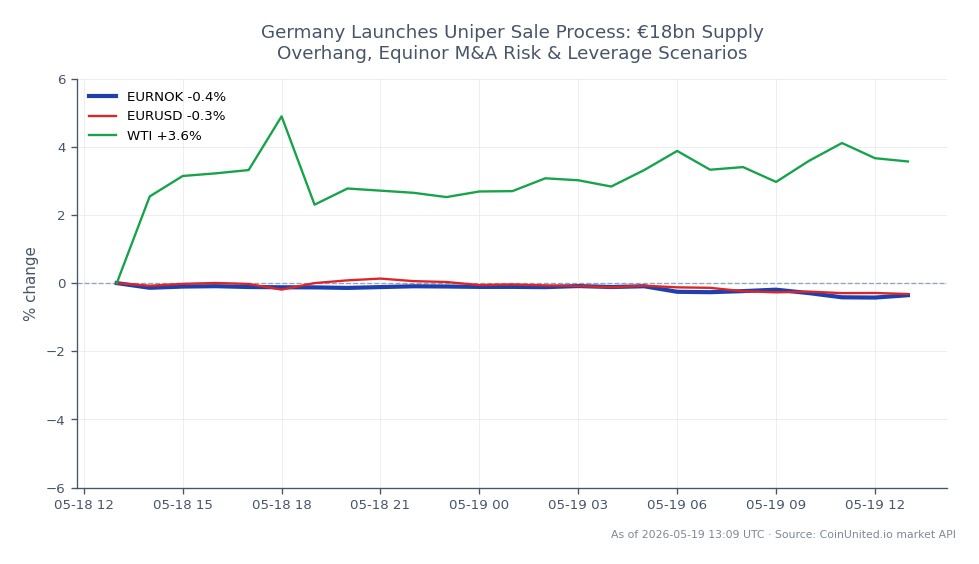

Data Snapshot

Key Takeaways

- •Germany must reduce its ~99% Uniper stake to ≤25%+1 share by end-2028 under EU state-aid rules — a structural, policy-driven sell-down worth €13–14bn+ in equity.

- •Leverage risk is asymmetric: supply overhang creates a near-term bearish bias, but a strategic buyer (Equinor or TAQA) moving to binding talks could trigger a rapid control premium — highly dangerous for high-leverage short positions.

- •Equinor CFDs face event risk if the Norwegian major pursues a deal; M&A announcements historically pressure the acquirer's stock 3–8% on announcement day.

- •EUR/USD and EUR/NOK carry indirect sensitivity — a successful large European privatisation supports post-crisis EU fiscal normalisation narratives.

- •This event reinforces the IPO Wave & Capital Markets Revival theme; successful execution could unlock appetite for other European state-asset sales.

As reported by Reuters and confirmed by the Bundesregierung, the German Federal Government — which owns approximately 99% of Uniper following a 2022 emergency nationalisation — has initiated a formal

Event Summary

As reported by Reuters and confirmed by the Bundesregierung, the German Federal Government — which owns approximately 99% of Uniper following a 2022 emergency nationalisation — has initiated a formal reprivatisation process. Under EU state-aid conditions, Germany must reduce its stake to no more than 25% + 1 share by end-2028. According to Reuters-based sources, Berlin could launch an official tender notice before summer, with options including a direct strategic sale, block trade, or IPO. A previously explored merger with SEFE has been set aside as too complex.

Uniper carries a Frankfurt market valuation of approximately €18bn, meaning Germany could place €13–14bn+ in equity over multiple tranches. Advisors confirmed include UBS and Roland Berger for Germany, Goldman Sachs for Uniper's board, and Citigroup and Deutsche Bank as potential arrangers. Strategic buyer interest has been reported from Abu Dhabi's TAQA and Norway's Equinor, per Bloomberg via source [4]. Transaction structure, pricing, and final timing remain unconfirmed.

Leverage Impact Analysis

For traders using CoinUnited.io's stock CFDs with up to 2000x leverage, Uniper's reprivatisation process creates a classic supply-overhang setup — typically bearish near-term, with event-driven volatility spikes around formal announcements.

Worked example — short-side overhang play: A 50x short Uniper CFD opened at the current market price faces elevated risk around any formal tender notice or book-building announcement. Equity offerings in government sell-downs historically price at a 3–7% discount to the prevailing market price. At 50x leverage, a 5% adverse move (e.g., a surprise strategic buyer emerges and triggers a control premium) would generate a 250% loss on margin — a full liquidation event. Position sizing must account for binary headline risk.

Long-side re-rating play: If a strategic buyer such as Equinor or TAQA moves to binding negotiations, a control premium could materialise rapidly. A 20x long Uniper CFD position could see a 10–15% premium translate to a 200–300% margin return — but this remains conditional on deal confirmation. Monitor for MoU announcements or exclusive negotiation reports as triggers.

Funding rate and open interest data are not yet available for this event stage — check live positioning on CoinUnited.io for real-time confirmation signals.

Cross-Market Impact

Equinor (EQNR): If Equinor pursues a binding offer for a large Uniper stake, expect scrutiny of its return-on-capital and leverage metrics. M&A deals seen as dilutive historically pressure the acquirer's stock 3–8% on announcement. Traders can access Equinor CFDs to position around deal confirmation risk.

EUR/USD & EUR/NOK: The sale is not a macro shock, but a successful large-scale European privatisation supports the narrative of post-crisis EU fiscal normalisation, marginally positive for EUR sentiment. EUR/USD and EUR/NOK both carry indirect sensitivity — EUR/NOK specifically if Equinor's strategic direction shifts materially toward European regulated assets.

WTI Crude / European Energy: Uniper's transition from distressed state entity to market-traded utility signals reduced systemic energy-security tail risk in Germany. This is marginally negative for crisis-risk premiums in WTI Light Crude Oil and European gas contracts, though fundamental supply/demand factors dominate.

This event fits within the broader IPO Wave & Capital Markets Revival theme — a successful Uniper placement would reinforce European ECM momentum and appetite for large state-asset deals.

Trading Considerations

Key levels to watch: Uniper's €18bn market cap implies a per-share reference; any discount guidance in the 3–7% range on deal tranches sets near-term technical support. The primary risk event is the formal tender notice, expected before summer per Reuters sources — this is the first binary catalyst. German snap elections introduce political timing uncertainty: a change in coalition could accelerate or delay the pace of the stake reduction.

Watch for: binding offer announcements from TAQA or Equinor (control premium trigger), official offer size/pricing guidance (overhang confirmation), and Uniper earnings updates that could shift the re-rating narrative.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

Large government sell-downs typically price tranches at a 3–7% discount to market, creating downward pressure on the stock near announcement dates. At 50x leverage, a 5% adverse move equals 250% margin loss — position sizing must reflect this binary headline risk.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.