Hızlı Bağlantılar

Apollo's $7.7B easyJet Counter-Bid: Merger Arb Spreads, Leverage Traps & European Aviation Repricing

Veri Anlık Görüntüsü

Ana Çıkarımlar

- •Castlelake's £6.90/share easyJet bid is confirmed in principle; an Apollo $7.7B topping bid remains unverified — treat as speculative until UK Takeover Code filings appear.

- •easyJet shares trade ~10–11% below the offer price (£6.12–£6.22 vs £6.90), implying significant deal-failure risk that can rapidly liquidate high-leverage long CFD positions on adverse news.

- •A 50x leveraged long easyJet CFD faces liquidation on a ~2% adverse move — deal-break scenarios involving a 30%+ share retracement would be catastrophically destructive to leveraged longs.

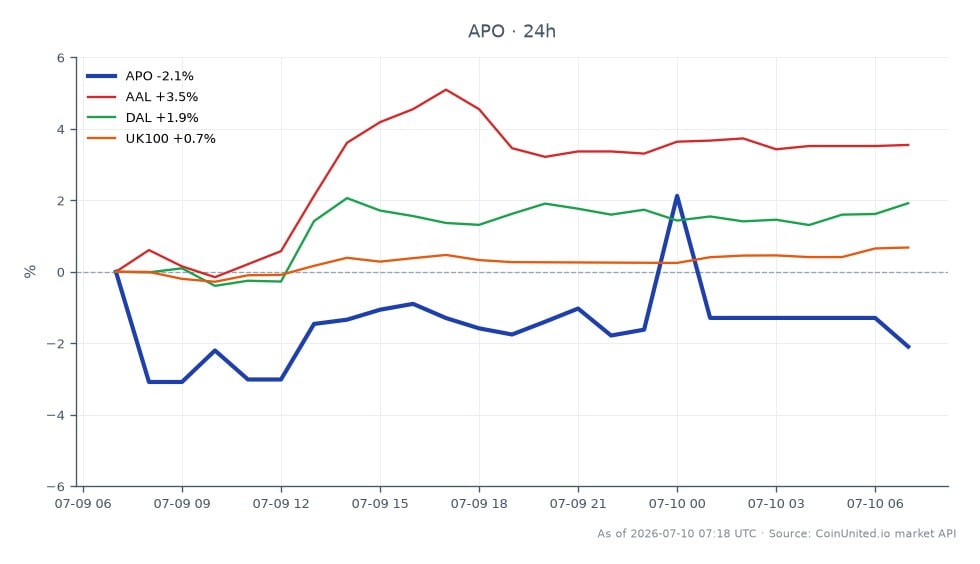

- •U.S. airline CFDs (DAL, UAL, AAL, LUV) may see sympathy bids as PE appetite for aviation assets at premium multiples re-rates sector comps.

- •Apollo (APO) at $119.37 with a 24h low of $118.47 offers minimal buffer for high-leverage APO CFD positions — monitor for official deal announcements as the primary repricing catalyst.

As reported by Reuters and CNBC, U.S. investment firm Castlelake has agreed in principle to acquire easyJet plc at £6.90 per share — valuing the carrier at approximately £5.5 billion (~$7.3 billion) —

Event Summary

As reported by Reuters and CNBC, U.S. investment firm Castlelake has agreed in principle to acquire easyJet plc at £6.90 per share — valuing the carrier at approximately £5.5 billion (~$7.3 billion) — representing a 73% premium to easyJet's May 29 closing price. The easyJet board is "minded to recommend" the offer, but the deal remains conditional, with Castlelake required to file a firm intention to bid by August 3 under UK Takeover Code rules.

A competing Apollo Global Management bid at ~$7.7 billion is currently unverified in public sources and should be treated as speculative. However, easyJet shares have already jumped 9–11% to four-year highs, trading around £6.12–£6.22 — still below the £6.90 Castlelake offer — implying the market prices in a meaningful probability of deal failure or a bidding contest. Apollo Global Management (APO) closed at $119.37, down 0.48% on the day (24h high: $125.98).

Leverage Impact Analysis

This is a live M&A acquisition wave scenario with a meaningful merger-arb spread — a high-voltage environment for leveraged CFD traders.

The arb spread trap: easyJet trades ~10–11% below the £6.90 Castlelake bid. A trader going long easyJet CFDs with 50x leverage to capture the spread faces amplified deal-break risk. If the deal collapses and shares revert to pre-bid levels (near £4.00, implied by the ~73% premium), a 42%+ drawdown in the underlying would wipe a 50x position many times over. Margin calls would trigger well before that — a 2% adverse move eliminates a 50x position entirely.

Apollo topping bid scenario: If a verified $7.7B Apollo counter-bid emerges, the spread compresses rapidly. Traders short easyJet (betting on deal failure) face a violent squeeze. A 5% gap-up on a topping bid announcement would liquidate short CFD positions running >20x leverage opened near current prices.

APO CFD positioning: Apollo stock itself (APO at $119.37) may re-rate on deal confirmation due to capital deployment implications. A 50x long APO CFD opened at $119.37 would see liquidation at approximately $117.19 (a ~1.8% adverse move), given the stock's 24h low of $118.47 — highlighting how thin the margin buffer is at high leverage on a name with active M&A news flow.

Cross-Market Impact

This deal sits within the broader global acquisition & consolidation wave reshaping European listed equities.

UK Indices: The FTSE 100 Index and FTSE 250 (where easyJet has heavier weight) will see passive rebalancing flows at deal completion. Pre-deal, easyJet's double-digit move contributes outsized performance to UK travel & leisure sub-indices.

U.S. Airlines (cross-sector read): A PE-driven take-private in European low-cost aviation signals appetite for airline assets at premium multiples. This is a secondary positive read for Delta Air Lines, United Airlines, American Airlines, and Southwest Airlines — though U.S. carriers face different demand/fuel dynamics. Watch for sympathy moves.

Brent Crude: A PE-owned easyJet may pursue fleet efficiency and route discipline over time, a marginal negative for jet fuel demand growth — but the Brent crude impact is second-order and unlikely to move benchmarks near-term.

GBP/FX: USD-denominated buyers acquiring GBP-priced assets generates marginal GBP demand, but deal size (~$7–8B) is small relative to daily FX turnover — negligible macro FX impact.

Trading Considerations

The key technical level is the £6.90 bid price — the ceiling on easyJet near-term unless a topping bid is confirmed. The floor is harder to define: if either bidder walks away before August 3, shares could retrace sharply toward pre-bid levels. Per the research report, at least one institutional shareholder estimates >30% deal-failure probability, which explains the persistent spread.

For APO CFD traders, the stock's 24h range of $118.47–$125.98 shows significant intraday volatility. The cross-sector acquisition repricing dynamic means APO could see further moves on deal confirmation. Monitor the August 3 Castlelake deadline and any UK Takeover Panel filings as the primary catalysts.

Trade Apollo Global Management, Inc. (New) on CoinUnited.io

Sıkça Sorulan Sorular

The ~10–11% gap between easyJet's market price and the £6.90 bid is the arb spread — but at 50x leverage, even a 2% move against your position triggers liquidation, meaning deal-break risk is existential for high-leverage longs.

Keşfetmeye Devam Et

Feragatname: Bu özet yalnızca eğitim amaçlıdır ve yatırım tavsiyesi değildir.