Hızlı Bağlantılar

Kosmos Energy Sells Equatorial Guinea Assets to Panoro for Up to $219.5M — What It Means for KOS and the African Offshore E&P Sector

Veri Anlık Görüntüsü

Ana Çıkarımlar

- •Deal value is up to $219.5m ($180m upfront + $39.5m contingent), not $127m — the lower figure likely reflects a net/adjusted amount.

- •Kosmos directs proceeds to RBL debt reduction plus ~$100m in projected capex/G&A savings, improving balance sheet quality.

- •Panoro becomes the largest shareholder in Block G but faces near-term equity dilution from a ~$48.6m private placement.

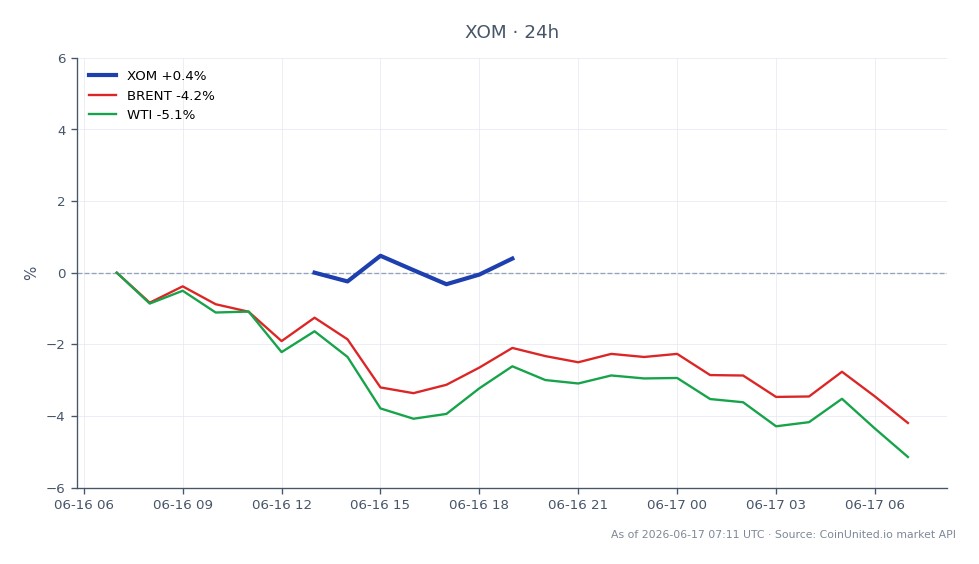

- •Zero impact on global oil supply — Ceiba/Okume continues under operator Trident Energy; Brent and WTI are unaffected.

- •This deal reinforces the broader trend of U.S.-listed E&Ps divesting non-core African assets to smaller, specialist independents.

Kosmos Energy (NYSE/LSE: KOS) has agreed to sell its 40.375% non-operating working interest in the Ceiba Field and Okume Complex (Block G, offshore Equatorial Guinea) to Panoro Energy ASA for $180m up

Event Analysis

Kosmos Energy (NYSE/LSE: KOS) has agreed to sell its 40.375% non-operating working interest in the Ceiba Field and Okume Complex (Block G, offshore Equatorial Guinea) to Panoro Energy ASA for $180m upfront plus up to $39.5m in contingent payments, totaling a maximum $219.5m, according to a Form 8-K filed with the U.S. SEC. The $127m figure cited in some headlines likely reflects a net or post-adjustment amount. The economic effective date is 1 January 2025, with closing expected mid-2026 pending final CEMAC (Central African Economic and Monetary Community) approval — host-country government sign-off from Equatorial Guinea is already secured.

For Kosmos, this is a classic portfolio high-grading play. The company explicitly frames it as balance sheet de-leveraging, with upfront proceeds directed at reducing its reserves-based lending (RBL) facility. Beyond the cash, Kosmos projects roughly $100m in combined capex and G&A savings over two years post-completion — a meaningful relief valve for an independent E&P carrying meaningful debt. Exiting a non-operated, non-core African asset to shore up finances is consistent with the broader energy sector acquisition and divestiture cycle playing out across mid-cap E&Ps.

For Panoro Energy (Oslo: PANORO), the deal transforms its position in Block G, making it the largest shareholder in the block, according to Baird Maritime. The acquisition was partly financed via a NOK 467m (~$48.6m) private placement of approximately 20 million new shares — meaningful dilution in the near term. This deal fits squarely within the global acquisition and consolidation wave where smaller, Africa-focused independents absorb assets divested by larger U.S.-listed players seeking capital discipline.

Critically, this is a change in ownership, not production capacity. Ceiba/Okume continues operating under Trident Energy, so there is no read-through to Brent crude or WTI supply fundamentals. The macro impact is essentially zero; the story is entirely stock-specific.

What This Means for Traders

For KOS holders, the near-term read is cautiously positive on a credit and equity basis. Debt reduction improves leverage metrics and interest coverage, which should support Kosmos's bond spreads and provide a modest re-rating catalyst for equity — particularly if the market had been discounting balance sheet risk. The risk is that selling Equatorial Guinea assets at an implied valuation that investors deem too cheap could weigh on sentiment. This is a stock-specific, relative-value setup rather than a sector catalyst, consistent with the energy, pharma & tech acquisition wave of asset-level deal-making.

For PANORO, short-term pressure is likely given the equity placement overhang and integration risk. However, medium-term upside exists if production thresholds are met and oil prices remain supportive — the contingent payments tied to 2027–2029 oil price and production benchmarks add meaningful optionality. Traders should monitor open interest and funding rates on any KOS CFD position for confirmation signals rather than assuming immediate directional momentum. Broader energy majors like Exxon Mobil and Chevron are unaffected directly, but the deal reinforces the theme of disciplined portfolio management rewarding balance sheet strength over production growth.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Sıkça Sorulan Sorular

The $127m figure likely reflects a net or cash-adjusted amount after accounting for working capital adjustments or interim cash flows since the 1 January 2025 effective date. The SEC-filed terms confirm $180m upfront plus up to $39.5m contingent.

Keşfetmeye Devam Et

Feragatname: Bu özet yalnızca eğitim amaçlıdır ve yatırım tavsiyesi değildir.