快速連結

QXO-TopBuild Merger Clears Final Hurdle: Stockholder Approval Unlocks $17B Building Products Mega-Deal

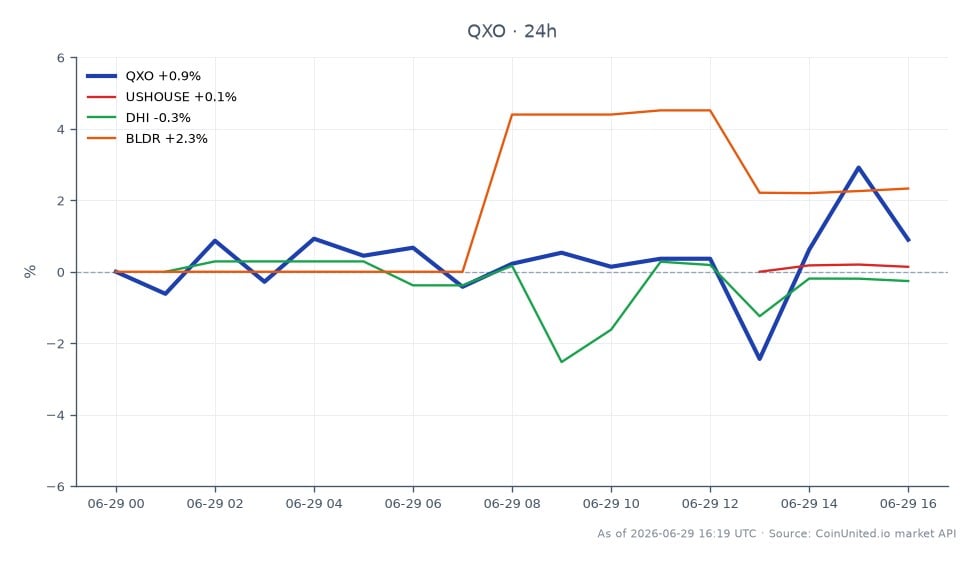

數據快照

重點摘要

- •Stockholder approvals obtained on both sides, with U.S. and Canadian antitrust clearances already in hand — deal closure in Q3 2026 is now the base case.

- •TopBuild's $505 per-share offer price acts as a hard near-term ceiling; spread compression benefits existing merger-arb longs in BLD.

- •QXO absorbs $6B in new debt and issues ~$7.9B in new equity — leverage and dilution dynamics will drive QXO's post-close re-rating.

- •The combined $50B enterprise entity becomes the second-largest North American building products distributor, with pricing power implications for insulation and roofing peers.

- •Residual policy risk remains: the American Economic Liberties Project has called for FTC and state AG scrutiny, adding headline volatility potential ahead of close.

With stockholder approvals now secured from both sides, the QXO Inc. and TopBuild Corp. merger is firmly on track to close in Q3 2026. As documented in SEC filings and a joint press release dated Apri

Event Analysis

With stockholder approvals now secured from both sides, the QXO Inc. and TopBuild Corp. merger is firmly on track to close in Q3 2026. As documented in SEC filings and a joint press release dated April 19, 2026, QXO will acquire TopBuild for approximately $17 billion, valuing each TopBuild share at $505 in a cash-and-stock transaction. TopBuild shareholders had until June 29, 2026 at 5:00 p.m. ET to elect their preferred consideration — cash at $505 per share or 20.200 QXO shares per TopBuild share — with the cash portion capped at 45% of total consideration.

The regulatory path is equally clear. According to SEC filings, the U.S. HSR antitrust waiting period expired in late May 2026, and the Canadian Competition Bureau issued a no-action letter on May 28, 2026 — meaning both major jurisdictions have stepped aside. The one residual risk flagged by the American Economic Liberties Project is an FTC or state AG investigation into potential anticompetitive concentration in insulation and roofing distribution, but this has not halted proceedings. A $600 million termination fee on each side meaningfully anchors both parties to completion.

This deal is part of the broader M&A acquisition wave reshaping industrial distribution, and it reflects a pattern of cross-sector acquisition repricing now rippling through building materials. Post-merger, QXO becomes the second-largest publicly traded building products distributor in North America, with a combined enterprise value of approximately $50 billion. The financing stack — roughly $7.9 billion in new QXO equity, $6 billion in new debt, $1 billion from a committed facility, and ~$2 billion cash on hand — is substantial, and leverage implications for QXO's credit profile deserve close monitoring. Traders who want deeper context on how large acquisition financing reshapes balance sheets can reference our acquisition arbitrage guide.

What This Means for Traders

For TopBuild (BLD), the $505 per-share offer functions as a hard valuation ceiling in the near term. With stockholder approval obtained and antitrust cleared, the deal-completion probability has risen sharply, which should compress any remaining spread between BLD's trading price and the implied deal value. Classic merger-arb positioning — long BLD, short QXO — becomes less attractive as the spread narrows, but residual spread still captures the time value and tail risk to closing. For QXO (QXO), which was trading at $18.05 (+1.95% on the session, with a 24h high of $18.48 and low of $17.23 per live market data), the stock is absorbing dilution from $7.9 billion in new share issuance alongside a dramatically expanded asset base. The re-rating thesis depends on whether QXO can realize scale advantages in purchasing power and pricing.

The sector read-through is meaningful for building products peers. A more consolidated QXO-TopBuild entity may pressure margins for competitors in insulation and roofing distribution and installation, while also shifting channel dynamics for manufacturers selling through these networks. Assets like Builders FirstSource, Inc. and D.R. Horton, Inc. carry indirect exposure — the former as a distribution peer, the latter as a major homebuilder reliant on insulation and building envelope supply chains. The US PHLX Housing Sector Index provides a broader read on whether housing-linked equities are pricing any cost-structure shift from consolidation in their supply base.

Trade QXO, Inc. on CoinUnited.io

Trade QXO with up to 1000xx leverage → | Create Free Account

常見問題

The primary risks are now limited to any unexpected FTC or state AG intervention and remaining customary closing conditions. The $600 million termination fee on each side strongly incentivizes completion.

繼續探索

免責聲明: 本快訊僅供教育目的,不構成投資建議。