快速連結

Warsh's Fed Framework Overhaul: Less Guidance, Higher Volatility — Leverage Map Across FX, Rates & Risk Assets

數據快照

重點摘要

- •Leveraged FX and rates positions face higher gap risk without dot-plot guidance — reduce sizing ahead of CPI, PCE, and FOMC dates as the Fed's new reaction function is data-realized, not forecast-driven.

- •QT bias and higher US real yields support USD structurally, putting EURUSD longs and high-beta EM FX at risk; USDJPY upside is the clearest rate-differential trade.

- •Bear-steepening risk in Treasuries (long yields rising faster than short) favors financials CFDs and hurts long-duration tech indices — rotate toward value/quality over high-multiple growth.

- •Gold faces competing forces: higher real yields are bearish, but policy opacity and tail-risk are bullish — expect elevated volatility rather than a clean directional move.

- •Crypto faces a near-term macro headwind from tighter liquidity, but Warsh's stablecoin regulatory clarity push could be a medium-term structural positive for USD-backed token infrastructure.

According to JPMorgan Asset Management and Morningstar, Kevin Warsh has assumed the Federal Reserve Chair role and is signaling a sweeping regime change in Fed operations — without requiring congressi

Event Summary

According to JPMorgan Asset Management and Morningstar, Kevin Warsh has assumed the Federal Reserve Chair role and is signaling a sweeping regime change in Fed operations — without requiring congressional approval. The overhaul spans communication strategy, inflation metrics, balance sheet policy, and regulatory posture. JPMorgan summarizes the agenda via the WARSH acronym: Withdrawal from forward guidance, Anchoring to trimmed-mean inflation, Reduction of the balance sheet, Smaller regulatory footprint, and Honoring Fed independence through inflation discipline.

As reported by Morningstar, Goldman Sachs economists no longer expect rate cuts in 2026, pushing the easing timeline to 2027 at the earliest — contingent on core PCE nearing 2%. Markets have shifted from pricing cuts to factoring in at least one 25 bp hike over the next six months, with the current funds rate target at 3.50–3.75%. The FOMC通膨政策十字路口 is now defined by a monitoring phase, not an active policy pivot.

Leverage Impact Analysis

Warsh's withdrawal from forward guidance is the single most important structural change for leveraged traders: it raises volatility across every asset class around FOMC dates and macro data releases. The Fed macro policy crossroads framework now rewards tactical agility over directional carry.

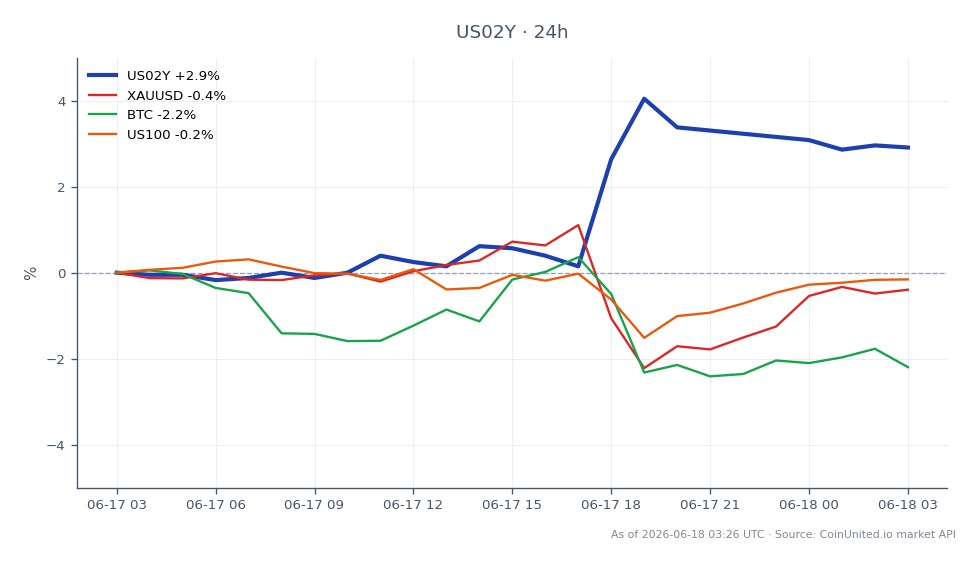

Rates example: The US 2-Year yield (US02Y) is trading at $4.17, down 0.45% on the day but anchored in a tight $4.17–$4.18 range. A 100x long position on US02Y CFDs opened at current levels carries meaningful gap risk around future CPI and trimmed-mean PCE prints — the new reaction function is data-realized, not forecast-driven.

FX example: A 50x long EURUSD position is directly exposed to USD re-pricing. QT bias and higher US real yields structurally support the dollar. With reduced dot-plot guidance, each data surprise now moves FX more sharply — a 1% adverse USD move on a 50x EURUSD position wipes 50% of margin. Per our Fed rate decisions market impact guide, hawkish surprises without the buffer of forward guidance historically generate outsized short-covering rallies in USD.

Key risk: Without the Fed's hand-holding via precise rate-path guidance, implied volatility in SOFR, FX, and equity options carries a structural upward bias. Leverage sizing should be reduced ahead of inflation prints (Dallas Fed trimmed-mean, Cleveland median CPI now market-relevant).

Cross-Market Impact

Treasuries & DXY: QT bias and opacity push long yields higher via term premium expansion — bear-steepening risk is real. USD/JPY dynamics are particularly exposed: higher US real yields widen the rate differential further, sustaining USDJPY upside.

Equities: Financials benefit from a steeper curve and lighter regulation. Long-duration tech (NASDAQ 100) faces headwinds from higher discount rates and elevated macro uncertainty — see S&P 500 FOMC cycle dynamics. VIX carries an upward bias structurally.

Gold: The gold vs. USD inverse relationship is under tension — higher real yields are gold-negative, but policy opacity and tail-risk of error are gold-positive. Expect higher gold volatility, not a clean directional trend.

Crypto: Higher real yields and QT are a macro drag on Bitcoin and Ethereum. Near-term, the liquidity-tightening environment compresses risk-asset multiples. Longer term, Warsh's push for stablecoin regulatory clarity could be a structural tailwind for USD-backed token infrastructure — see institutional stablecoins 2026.

Trading Considerations

US02Y at $4.17 reflects the market's near-term hold consensus, but the range compression (24h spread of just $0.01) signals coiled volatility ahead of the next inflation print. Key levels to watch: a break above $4.18 on US02Y would signal renewed front-end hawkish repricing; DXY strength above recent highs would confirm USD carry trade resumption. Monitor Dallas Fed trimmed-mean and Cleveland median CPI — these now function as Warsh's de facto policy trigger, replacing traditional core PCE thresholds. VIX regime shifts around FOMC dates will determine leverage survivability on equity positions.

Trade United States 2 Year Yield on CoinUnited.io

Trade US02Y with up to 2000xx leverage → | Create Free Account

常見問題

Without dot-plot guidance, each macro data release (CPI, PCE, jobs) now carries outsized FX movement potential — a 50x EURUSD long can lose 50% of margin on a 1% adverse USD move triggered by a single inflation print. Traders should reduce leverage size ahead of key data and treat FOMC weeks as high-volatility, wide-stop environments.

繼續探索

免責聲明: 本快訊僅供教育目的,不構成投資建議。