Snabblänkar

ABB Q2 Earnings Beat + $5.5bn Rotork Deal: Leverage Scenarios for European Industrials CFDs

Datasnapshot

Viktiga punkter

- •ABB Q2 EBITA of ~$1.708bn beat consensus ~$1.65bn by ~4%, with U.S. orders surging 37% on AI/data-center demand — a fundamental positive for the stock.

- •The $5.5bn all-cash Rotork acquisition at a ~60% premium introduces integration risk and cash reduction; leveraged long ABB CFD positions face near-term volatility from the market's acquisition-premium debate.

- •Rotork equity transitions to an M&A arbitrage trade anchored near 503p — high-leverage positions carry binary deal-break risk over the ~12-month closing timeline.

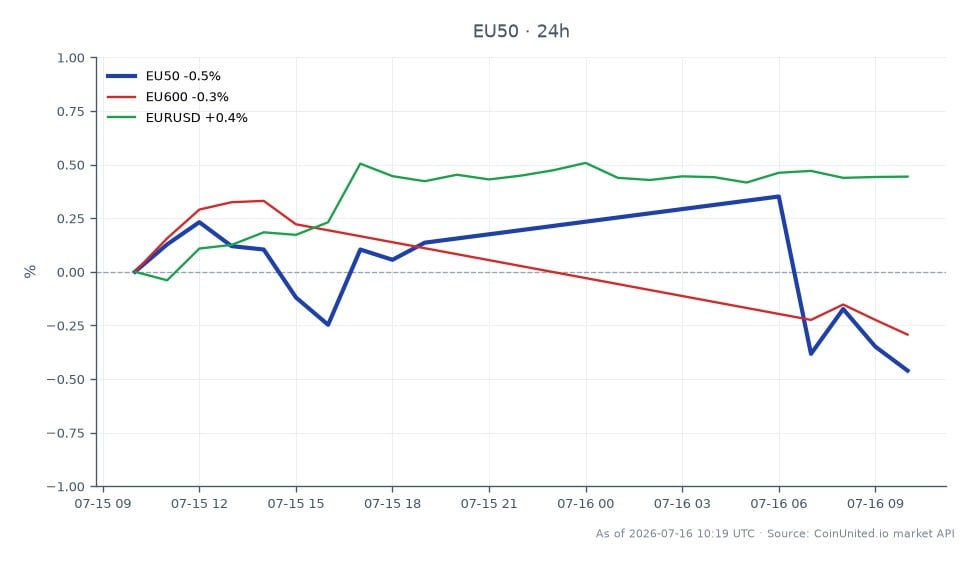

- •ABB's index weight means this event directly impacts EURO STOXX 50 and STOXX Europe 600 CFD traders, acting as a live European industrials sector-rotation signal.

- •No direct crypto or major FX impact; EURUSD effect is marginal and secondary to the equity-specific dynamics.

According to Investing.com and Reuters, ABB Ltd reported Q2 operational EBITA of ~$1.708bn (+9% YoY, margin 19.2%), beating consensus of ~$1.65bn. Simultaneously, ABB announced an all-cash agreement t

Event Summary

According to Investing.com and Reuters, ABB Ltd reported Q2 operational EBITA of ~$1.708bn (+9% YoY, margin 19.2%), beating consensus of ~$1.65bn. Simultaneously, ABB announced an all-cash agreement to acquire Rotork plc, a British flow-control manufacturer, for $5.5 billion — offering Rotork shareholders 503 pence per share, a ~60% premium to its three-month average price. ABB will fund the deal from ~$5.8bn in cash/marketable securities plus committed bank facilities. The transaction, structured as a UK court-sanctioned scheme of arrangement, is expected to close in H1 2027, pending Rotork shareholder and regulatory approval.

ABB's Q2 also showed revenue of $8.90bn (+8% YoY) and record orders, with U.S. orders surging 37%, driven by data-center and AI infrastructure demand. This positions ABB firmly within the AI infrastructure capital reallocation theme playing out across global industrials.

Leverage Impact Analysis

This is a dual-catalyst event — an earnings beat combined with a major acquisition — creating divergent leverage dynamics depending on your ABB position direction.

Bull scenario (long ABB CFD): The Q2 beat and record orders provide fundamental support. A trader holding a 50x long ABB CFD entering at pre-announcement levels would need to manage the acquisition-overhang risk: markets often penalize the acquirer short-term due to cash depletion and integration uncertainty. A 3–5% gap against the position at 50x leverage translates to a 150–250% drawdown on margin — requiring careful stop placement.

Bear scenario (short ABB CFD): If investors perceive the 60% Rotork premium as overpaying, a repricing lower is possible. However, ABB's $5.8bn cash buffer roughly covers the deal, limiting balance-sheet stress. A 20x short facing a relief rally on strong orders could see rapid liquidation.

Rotork arb play: With Rotork anchoring near 503p, this becomes a pure acquisition arbitrage trade. The spread between current market price and 503p reflects deal-completion risk over an ~12-month timeline to H1 2027. High-leverage positions on Rotork carry binary risk — deal breaks compress the spread violently.

Monitor open interest on ABB CFDs and check funding rates on CoinUnited.io for positioning signals as the market digests the dual catalyst.

Cross-Market Impact

ABB is a major constituent of European indices. An ABB re-rating — positive or negative — feeds directly into the EURO STOXX 50 and STOXX Europe 600, where industrials carry meaningful index weight. Traders in European index CFDs should treat this as a live sector-rotation signal: a sustained ABB rally could lift the European industrials sub-basket and support broader index momentum.

On EURUSD, the macro read is secondary but relevant — ABB's 37% U.S. order surge signals robust dollar-zone capex, which is marginally USD-supportive. This is too small to move the pair independently but adds to the constructive U.S. growth narrative. The M&A acquisition wave theme signals continued European industrial consolidation, which can attract capital inflows into EUR-denominated equities. The deal fits squarely within the broader cross-sector acquisition repricing dynamic active across global markets.

Trading Considerations

For ABB CFDs, the key tension is earnings strength vs. acquisition execution risk. Watch for analyst price-target revisions in the 24–48 hours post-announcement — upgrades citing synergy potential are the bull trigger; downgrades citing integration complexity or leverage metrics are the bear catalyst. The H1 2027 close timeline means Rotork arb spreads will widen or compress based on regulatory headline risk from EU and UK competition authorities.

For European index traders, monitor whether ABB's move is accompanied by broad industrials sector rotation — confirmation would require peer names (Siemens, Schneider Electric) moving in sympathy, signaling genuine sector earnings beat re-rating rather than single-stock noise.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Vanliga Frågor

Large all-cash acquisitions at a 60% premium often cause short-term volatility in the acquirer's stock as markets debate synergy vs. overpayment — at 50x leverage, even a 2% adverse move erodes 100% of margin, so tight stops are essential. The Q2 earnings beat provides a fundamental buffer, but position sizing should reflect the dual-catalyst uncertainty.

Fortsätt Utforska

Ansvarsfriskrivning: Denna sammanfattning är endast för utbildningsändamål och utgör inte investeringsrådgivning.

">%0D%0A <path d="m65.883 9.018.032 5.181h-1.223c-.773-3.733-2.671-5.73-5.797-5.73-4.441 0-6.5 4.442-6.5 9.913 0 5.985 2.38 10.588 6.79 10.588 3.024 0 5.084-1.898 6.211-6.597h1.287l-.482 6.05a13.606 13.606 0 0 1-7.434 1.93c-7.016 0-11.36-4.409-11.36-11.071 0-7.467 4.989-12.166 11.36-12.166a12.961 12.961 0 0 1 7.112 1.899M68.714 21.89c0-5.47 3.572-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.573 9.205-8.367 9.205a7.908 7.908 0 0 1-8.271-8.464zm11.876.354c0-4.762-1.095-8.406-3.669-8.406-2.38 0-3.478 2.703-3.478 6.92 0 4.762 1.126 8.431 3.701 8.431 2.382 0 3.444-2.735 3.444-6.956M93.236 27.555c0 1.126.515 1.318 2.03 1.416v1.062h-8.497V28.97c1.514-.097 2.03-.29 2.03-1.415V16.16l-1.93-1.126v-.611l5.663-1.77h.709l-.005 14.9zM88.345 8.18a2.625 2.625 0 0 1 5.246 0 2.625 2.625 0 0 1-5.246 0zM109.007 18.157c0-1.867-.709-2.8-2.479-2.8a6.474 6.474 0 0 0-3.604 1.319v10.877c0 1.126.482 1.319 1.962 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.93-1.126v-.612l5.76-1.77h.741l-.129 3.154a7.735 7.735 0 0 1 5.954-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.995 1.416v1.062h-8.432V28.97c1.48-.097 1.963-.29 1.963-1.416v-9.396zM123.52 21.851c0 3.927 1.706 6.308 5.247 6.308 3.54 0 5.985-1.867 5.985-6.5V10.82c0-1.74-.419-2.03-3.058-2.253V7.442h7.37v1.126c-2.252.258-2.574.515-2.574 2.253v11.425c0 5.535-3.797 8.116-8.561 8.116-5.697 0-9.108-2.64-9.108-8.174v-11.4c0-1.77-.321-1.965-2.574-2.221V7.44h9.849v1.126c-2.253.258-2.574.45-2.574 2.22l-.002 11.064zM152.26 18.157c0-1.867-.707-2.8-2.478-2.8a6.484 6.484 0 0 0-3.605 1.319v10.877c0 1.126.483 1.319 1.964 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.931-1.126v-.612l5.761-1.77h.74l-.129 3.154a7.731 7.731 0 0 1 5.953-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.996 1.416v1.062h-8.432V28.97c1.479-.097 1.962-.29 1.962-1.416v-9.396zM166.259 27.555c0 1.126.515 1.318 2.029 1.416v1.062h-8.496V28.97c1.512-.097 2.029-.29 2.029-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.709l-.003 14.9zM161.368 8.18a2.62 2.62 0 0 1 2.622-2.518 2.625 2.625 0 0 1 2.623 2.518 2.626 2.626 0 0 1-4.441 1.786 2.62 2.62 0 0 1-.804-1.786zM175.33 12.976h4.183v1.48h-4.183v10.652c0 1.964.741 2.8 2.253 2.8a3.755 3.755 0 0 0 2.414-.901l.387.58a5.65 5.65 0 0 1-4.956 2.768c-2.64 0-4.57-1.384-4.57-4.989v-10.91h-1.996v-.741a13.265 13.265 0 0 0 5.508-4.928h.965l-.005 4.189zM195.514 19.38v.741h-10.492c-.129 4.506 2.189 7.177 5.342 7.177a5.427 5.427 0 0 0 4.796-2.609l.515.29a6.75 6.75 0 0 1-6.888 5.374c-4.665 0-7.787-3.443-7.787-8.406 0-5.507 3.539-9.3 7.948-9.3 4.313 0 6.566 2.864 6.566 6.726m-10.427-.45h6.437c0-3.025-.805-5.085-2.899-5.085-2.125 0-3.283 2.125-3.541 5.084M207.001 7.054v-.676l5.696-1.545h.707v21.788c0 1.094.064 1.45 1.287 1.545l.805.064v.965l-5.857 1.16h-.838l.129-2.993a6.145 6.145 0 0 1-5.181 2.993c-3.895 0-6.5-3.154-6.5-8.046 0-6.087 3.604-9.59 8.206-9.59a5.117 5.117 0 0 1 3.478 1.126V8.048l-1.932-.994zm-5.342 13.709c0 3.926 1.609 6.855 4.538 6.855a3.901 3.901 0 0 0 2.736-1.03v-8.496c0-2.51-1.062-3.99-2.993-3.99-2.703 0-4.28 2.64-4.28 6.667M219.683 24.754a2.796 2.796 0 0 1 2.587 1.729 2.8 2.8 0 1 1-5.387 1.072 2.75 2.75 0 0 1 1.721-2.6 2.753 2.753 0 0 1 1.079-.2zM230.592 27.555c0 1.126.516 1.318 2.029 1.416v1.062h-8.501V28.97c1.512-.097 2.03-.29 2.03-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.708l.002 14.9zM225.7 8.18a2.626 2.626 0 0 1 4.441-1.787c.488.47.777 1.11.804 1.787a2.625 2.625 0 0 1-5.245 0zM233.842 21.89c0-5.47 3.573-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.572 9.205-8.366 9.205a7.904 7.904 0 0 1-7.809-5.179 7.904 7.904 0 0 1-.463-3.285zm11.876.354c0-4.762-1.094-8.406-3.669-8.406-2.382 0-3.479 2.703-3.479 6.92 0 4.762 1.126 8.431 3.7 8.431 2.382 0 3.444-2.735 3.444-6.956M18.386.684a17.469 17.469 0 1 0 0 34.937 17.469 17.469 0 0 0 0-34.937zm0 31.74a14.277 14.277 0 1 1 0-28.554 14.277 14.277 0 0 1 0 28.554z" fill="%23fff"/>%0D%0A <path d="M18.393 36.019a17.868 17.868 0 1 1 17.86-17.868 17.887 17.887 0 0 1-17.86 17.868zm0-34.938a17.07 17.07 0 1 0 17.063 17.07 17.089 17.089 0 0 0-17.063-17.07zm0 31.74a14.675 14.675 0 1 1 10.366-4.297 14.691 14.691 0 0 1-10.373 4.303m0-28.552a13.877 13.877 0 1 0 13.879 13.878A13.893 13.893 0 0 0 18.386 4.275z" fill="%23fff"/>%0D%0A <path d="M17.42 8.46a8.46 8.46 0 1 1-16.923 0 8.46 8.46 0 0 1 16.924 0" fill="%23E48A22"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="sy6kzo59ya">%0D%0A <path fill="%23fff" transform="translate(.5)" d="M0 0h250v36.019H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

"><path fill="%23fff" transform="scale(1.9886)" d="M27.72,2.61a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-30.14,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-32.16,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-34.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-40.2,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-58.29,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-62.32,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m30.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m22.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m34.16,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m18.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.27,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-56.29,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-48.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2"/><path d="M123.088,117.106a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M123.088,133.085a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M91.095,145.087a1.987,1.987,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989,2.01,2.01,0,0,1,1.989-1.988zM107.109,145.087a1.988,1.988,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989c-.035-1.081.872-1.988,1.989-1.988zM115.098,145.087a1.987,1.987,0,1,1,0,3.977,1.987,1.987,0,0,1-1.988-1.989c-.035-1.081.872-1.988,1.988-1.988zM123.088,145.087a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M151.069,149.064a1.988,1.988,0,1,1-1.989,1.989c-.035-1.082.872-1.989,1.989-1.989zM25.271,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491c0-1.575,1.277-2.852,2.83-2.852h6.492a2.852,2.852,0,0,1,2.852,2.852v6.49h.021z" fill="%23fff"/><path d="M33.38,30.568a2.852,2.852,0,0,1-2.852,2.851H7.798a2.852,2.852,0,0,1-2.851-2.851V7.817a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.75h-.021zM29.315,11.86a2.852,2.852,0,0,0-2.852-2.852H11.842A2.852,2.852,0,0,0,8.99,11.86v14.642a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852V11.86h-.021zM25.271,142.338a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491a2.852,2.852,0,0,1,2.852-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.491z" fill="%23fff"/><path d="M33.38,150.468a2.852,2.852,0,0,1-2.852,2.852H7.798a2.852,2.852,0,0,1-2.851-2.852v-22.751a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.751h-.021zm-4.065-18.686a2.852,2.852,0,0,0-2.852-2.852H11.842a2.852,2.852,0,0,0-2.852,2.852v14.621a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852v-14.621h-.021zM145.171,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.491a2.851,2.851,0,0,1-2.851-2.852v-6.491a2.851,2.851,0,0,1,2.851-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.49z" fill="%23fff"/><path d="M153.301,30.568a2.852,2.852,0,0,1-2.852,2.851h-22.75a2.852,2.852,0,0,1-2.852-2.851V7.817a2.852,2.852,0,0,1,2.852-2.852h22.75a2.852,2.852,0,0,1,2.852,2.852v22.75zm-4.065-18.707a2.852,2.852,0,0,0-2.852-2.852h-14.621a2.852,2.852,0,0,0-2.851,2.852v14.642a2.852,2.852,0,0,0,2.851,2.852h14.621a2.852,2.852,0,0,0,2.852-2.852V11.86zM78.535,62.051c-9.176,0-16.607,7.431-16.607,16.607,0,9.176,7.431,16.607,16.607,16.607,9.176,0,16.607-7.431,16.607-16.607,0-9.176-7.431-16.607-16.607-16.607zm0,30.214c-7.501,0-13.572-6.07-13.572-13.572,0-7.501,6.07-13.572,13.572-13.572,7.501,0,13.572,6.07,13.572,13.572,0,7.501-6.071,13.572-13.572,13.572z" fill="%23fff"/><path d="M78.535,95.649c-9.385,0-16.991-7.64-16.991-16.99,0-9.386,7.64-16.992,16.99-16.992,9.386,0,16.992,7.64,16.992,16.991,0,9.35-7.64,16.991-16.991,16.991zm0-33.214c-8.966,0-16.258,7.292-16.258,16.258s7.291,16.258,16.258,16.258c8.966,0,16.258-7.291,16.258-16.258-.035-8.966-7.292-16.258-16.258-16.258zm0,30.214c-7.71,0-13.956-6.28-13.956-13.956,0-7.71,6.28-13.956,13.956-13.956,7.71,0,13.956,6.28,13.956,13.956,0,7.676-6.28,13.956-13.956,13.956zm0-27.179c-7.292,0-13.223,5.931-13.223,13.223,0,7.292,5.931,13.223,13.223,13.223,7.292,0,13.223-5.931,13.223-13.223-.035-7.292-5.966-13.223-13.223-13.223z" fill="%23fff"/><path d="M69.569,77.507a8.06,8.06,0,1,0,0-16.119,8.06,8.06,0,0,0,0,16.119z" fill="%23E48A22"/></g><defs><clipPath id="arusb4546a"><path fill="%23fff" transform="translate(0 .019)" d="M0,0h157v157H0z"/></clipPath></defs></svg>)

">%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23fff"/>%0D%0A <path d="M106.646 32.584H4.356A3.857 3.857 0 0 1 .5 28.741V3.867A3.853 3.853 0 0 1 4.355.02h102.29a3.86 3.86 0 0 1 3.855 3.848V28.74a3.853 3.853 0 0 1-3.854 3.845z" fill="%23A6A6A6"/>%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23000"/>%0D%0A <path d="M25.063 16.13a4.717 4.717 0 0 1 2.25-3.961 4.84 4.84 0 0 0-3.812-2.059c-1.603-.168-3.159.959-3.976.959-.833 0-2.09-.942-3.447-.915a5.079 5.079 0 0 0-4.271 2.603c-1.848 3.195-.47 7.89 1.3 10.472.886 1.265 1.92 2.679 3.274 2.626 1.325-.052 1.82-.84 3.417-.84 1.584 0 2.05.84 3.43.81 1.42-.021 2.317-1.27 3.171-2.546a10.434 10.434 0 0 0 1.452-2.952 4.572 4.572 0 0 1-2.786-4.197h-.003zm-2.61-7.718a4.643 4.643 0 0 0 1.065-3.33 4.74 4.74 0 0 0-3.064 1.583 4.42 4.42 0 0 0-1.092 3.207 3.917 3.917 0 0 0 3.091-1.46zM44.25 25.674H42.4l-1.015-3.183H37.86l-.966 3.183H35.09l3.493-10.838h2.156l3.509 10.838h.002zm-3.17-4.517-.918-2.83c-.097-.29-.28-.97-.547-2.042h-.033c-.108.461-.28 1.142-.515 2.042l-.902 2.83h2.914zm12.137.515a4.422 4.422 0 0 1-1.085 3.152 3.178 3.178 0 0 1-2.41 1.03 2.415 2.415 0 0 1-2.235-1.109v4.1H45.75v-8.417c0-.835-.021-1.691-.064-2.569h1.529l.097 1.239h.032a3.09 3.09 0 0 1 2.398-1.395 3.095 3.095 0 0 1 2.552 1.088c.645.817.973 1.84.925 2.88l-.001.001zm-1.77.064a3.22 3.22 0 0 0-.516-1.882 1.781 1.781 0 0 0-1.513-.771c-.427 0-.84.15-1.166.426-.349.284-.59.678-.684 1.118a2.26 2.26 0 0 0-.08.528v1.302a2.09 2.09 0 0 0 .525 1.44 1.737 1.737 0 0 0 1.36.587 1.783 1.783 0 0 0 1.529-.755c.389-.59.58-1.29.544-1.995v.002zm10.768-.064a4.422 4.422 0 0 1-1.084 3.152 3.182 3.182 0 0 1-2.413 1.03 2.415 2.415 0 0 1-2.233-1.109v4.1h-1.739v-8.417c0-.835-.021-1.691-.065-2.569h1.53l.096 1.239h.033a3.092 3.092 0 0 1 3.803-1.153c.443.189.836.478 1.148.846.645.817.973 1.84.924 2.88v.001zm-1.771.064a3.22 3.22 0 0 0-.517-1.882 1.778 1.778 0 0 0-1.511-.771c-.427 0-.841.15-1.168.426-.349.284-.59.678-.683 1.118-.048.172-.075.35-.082.528v1.302a2.097 2.097 0 0 0 .523 1.44 1.74 1.74 0 0 0 1.361.587 1.781 1.781 0 0 0 1.53-.755c.39-.59.581-1.289.547-1.995v.002zm11.831.9a2.893 2.893 0 0 1-.964 2.251 4.278 4.278 0 0 1-2.956.949 5.163 5.163 0 0 1-2.809-.675l.402-1.447a4.84 4.84 0 0 0 2.511.676 2.371 2.371 0 0 0 1.53-.442 1.444 1.444 0 0 0 .548-1.181 1.511 1.511 0 0 0-.452-1.11 4.188 4.188 0 0 0-1.496-.836c-1.9-.707-2.85-1.742-2.85-3.104a2.737 2.737 0 0 1 1.006-2.187 3.981 3.981 0 0 1 2.664-.852 5.27 5.27 0 0 1 2.463.515l-.437 1.415a4.31 4.31 0 0 0-2.084-.498 2.121 2.121 0 0 0-1.438.45 1.289 1.289 0 0 0-.437.982 1.327 1.327 0 0 0 .5 1.061 5.63 5.63 0 0 0 1.577.836c.78.274 1.485.725 2.06 1.318.45.521.686 1.192.663 1.88v-.002zm5.762-3.472H76.12v3.794c0 .965.338 1.447 1.014 1.447.26.006.52-.021.773-.08l.048 1.318a3.942 3.942 0 0 1-1.352.192 2.085 2.085 0 0 1-1.61-.63 3.077 3.077 0 0 1-.578-2.107v-3.94h-1.141v-1.302h1.141v-1.43l1.707-.515v1.943h1.915l-.001 1.31zm8.627 2.54a4.284 4.284 0 0 1-1.03 2.959 3.674 3.674 0 0 1-2.865 1.19 3.504 3.504 0 0 1-2.746-1.14 4.154 4.154 0 0 1-1.022-2.879 4.249 4.249 0 0 1 1.054-2.974 3.655 3.655 0 0 1 2.842-1.155 3.577 3.577 0 0 1 2.768 1.142 4.1 4.1 0 0 1 1 2.856v.001zm-1.802.04a3.496 3.496 0 0 0-.465-1.843 1.72 1.72 0 0 0-1.562-.931 1.746 1.746 0 0 0-1.594.93 3.554 3.554 0 0 0-.466 1.877 3.485 3.485 0 0 0 .466 1.844 1.782 1.782 0 0 0 3.141-.015 3.51 3.51 0 0 0 .48-1.863v.001zm7.454-2.356a3.03 3.03 0 0 0-.547-.047 1.641 1.641 0 0 0-1.42.692 2.605 2.605 0 0 0-.434 1.543v4.1H88.18v-5.355c0-.82-.017-1.64-.052-2.46h1.514l.063 1.495h.049c.164-.488.466-.918.868-1.239.363-.271.804-.419 1.257-.42.145 0 .29.01.435.032v1.656l.002.003zm7.774 2.011c.004.264-.017.528-.064.788h-5.214a2.262 2.262 0 0 0 .756 1.77 2.59 2.59 0 0 0 1.707.544c.72.01 1.435-.115 2.11-.368l.272 1.204a6.527 6.527 0 0 1-2.623.483 3.805 3.805 0 0 1-2.86-1.067 3.95 3.95 0 0 1-1.039-2.87 4.473 4.473 0 0 1 .967-2.942 3.331 3.331 0 0 1 2.734-1.253 2.916 2.916 0 0 1 2.56 1.253c.48.728.722 1.586.694 2.456v.002zm-1.658-.45a2.348 2.348 0 0 0-.337-1.335 1.518 1.518 0 0 0-1.384-.725 1.648 1.648 0 0 0-1.381.706c-.297.392-.475.86-.515 1.35h3.62l-.003.004zM37.359 11.005a11.12 11.12 0 0 1-1.25-.063v-5.24c.487-.075.98-.112 1.472-.11 1.994 0 2.912.98 2.912 2.576 0 1.842-1.085 2.837-3.134 2.837zm.292-4.742a3.49 3.49 0 0 0-.688.055v3.984c.192.02.385.028.578.023 1.306 0 2.05-.743 2.05-2.133-.002-1.24-.674-1.929-1.94-1.929zm5.702 4.78a1.832 1.832 0 0 1-1.755-1.225 1.826 1.826 0 0 1-.097-.75 1.87 1.87 0 0 1 1.916-2.031 1.817 1.817 0 0 1 1.851 1.968 1.881 1.881 0 0 1-1.915 2.04v-.002zm.032-3.382c-.617 0-1.012.577-1.012 1.383 0 .79.404 1.365 1.005 1.365.6 0 1.004-.616 1.004-1.383 0-.779-.396-1.363-.996-1.363V7.66zm8.29-.545-1.203 3.84h-.784L49.19 9.29a12.619 12.619 0 0 1-.309-1.24h-.016c-.07.42-.174.835-.308 1.24l-.53 1.668h-.792l-1.132-3.841h.878l.435 1.826c.103.435.19.845.263 1.232h.017c.062-.323.165-.727.315-1.225l.546-1.833h.696l.523 1.795c.126.435.229.861.309 1.264h.023c.062-.426.15-.848.262-1.264l.468-1.795h.84-.004zm4.426 3.84h-.854V8.75c0-.679-.263-1.02-.776-1.02a.888.888 0 0 0-.854.942v2.284h-.854v-2.74c0-.34-.009-.705-.032-1.1h.751l.04.593h.024a1.38 1.38 0 0 1 1.219-.67c.806 0 1.336.616 1.336 1.619v2.3-.002zm2.356 0h-.855v-5.6h.855v5.6zm3.115.088a1.832 1.832 0 0 1-1.851-1.976 1.87 1.87 0 0 1 1.914-2.031 1.816 1.816 0 0 1 1.851 1.968 1.88 1.88 0 0 1-1.914 2.04v-.001zm.032-3.383c-.617 0-1.012.578-1.012 1.383 0 .79.404 1.366 1.003 1.366.6 0 1.005-.617 1.005-1.384 0-.779-.394-1.363-.998-1.363l.002-.002zm5.252 3.296-.063-.442h-.022a1.314 1.314 0 0 1-1.125.53 1.118 1.118 0 0 1-1.178-1.131c0-.946.823-1.438 2.247-1.438v-.071c0-.506-.268-.76-.798-.76a1.8 1.8 0 0 0-1.004.286l-.174-.561a2.46 2.46 0 0 1 1.32-.332c1.005 0 1.511.529 1.511 1.588v1.415a5.79 5.79 0 0 0 .056.917l-.77-.001zm-.118-1.913c-.949 0-1.425.23-1.425.774a.543.543 0 0 0 .586.6.818.818 0 0 0 .841-.78l-.002-.594zm4.982 1.913-.04-.617h-.024a1.288 1.288 0 0 1-1.234.704c-.927 0-1.614-.814-1.614-1.96 0-1.201.712-2.049 1.683-2.049a1.157 1.157 0 0 1 1.084.523h.017V5.35h.856v4.57c0 .372.009.72.031 1.036h-.76zm-.126-2.259a.93.93 0 0 0-.9-.998c-.631 0-1.021.561-1.021 1.351 0 .775.402 1.305 1.003 1.305a.96.96 0 0 0 .914-1.019v-.639h.004zm6.277 2.347a1.831 1.831 0 0 1-1.85-1.975 1.87 1.87 0 0 1 1.913-2.031 1.816 1.816 0 0 1 1.852 1.968 1.88 1.88 0 0 1-1.916 2.038zm.031-3.382c-.616 0-1.011.577-1.011 1.383 0 .79.403 1.365 1.003 1.365.6 0 1.005-.616 1.005-1.383 0-.782-.394-1.366-1-1.366h.003zm6.478 3.296h-.857V8.753c0-.68-.263-1.02-.775-1.02a.888.888 0 0 0-.854.94v2.285h-.855V8.215c0-.34-.009-.704-.032-1.099h.752l.04.593h.023a1.38 1.38 0 0 1 1.218-.671c.807 0 1.338.616 1.338 1.62l.002 2.3zm5.749-3.2h-.94v1.864c0 .473.165.712.497.712.128 0 .255-.013.38-.04l.023.648c-.213.07-.438.103-.663.095-.673 0-1.076-.372-1.076-1.344V7.758h-.56v-.64h.56v-.704l.841-.254v.956h.94v.641l-.002.001zm4.52 3.2h-.853v-2.19c0-.687-.26-1.035-.775-1.035a.838.838 0 0 0-.856.909v2.315h-.851V5.355h.854v2.307h.017a1.296 1.296 0 0 1 1.156-.624c.814 0 1.312.63 1.312 1.636l-.003 2.285zm4.635-1.715H96.72a1.102 1.102 0 0 0 1.21 1.137c.353.004.704-.058 1.035-.181l.133.593a3.212 3.212 0 0 1-1.29.237 1.789 1.789 0 0 1-1.913-1.936c0-1.178.728-2.063 1.818-2.063.982 0 1.598.728 1.598 1.826.006.13-.004.26-.03.387h.003zm-.783-.609c0-.593-.3-1.011-.846-1.011a1.014 1.014 0 0 0-.934 1.011h1.78z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="uavr3vx5ga">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

">%0D%0A <path d="M106.426 32.584H4.574a4.037 4.037 0 0 1-3.775-2.507 4.029 4.029 0 0 1-.3-1.564V4.09A4.028 4.028 0 0 1 3.01.318a4.038 4.038 0 0 1 1.565-.3h101.852a4.039 4.039 0 0 1 3.774 2.507c.203.496.305 1.028.3 1.564v24.424a4.032 4.032 0 0 1-4.074 4.071z" fill="%23000"/>%0D%0A <path d="M106.426.67a3.445 3.445 0 0 1 3.422 3.42v24.424a3.444 3.444 0 0 1-3.422 3.42H4.574a3.444 3.444 0 0 1-3.422-3.42V4.089A3.438 3.438 0 0 1 4.574.67h101.852zm0-.651H4.574A4.088 4.088 0 0 0 .5 4.089v24.425a4.029 4.029 0 0 0 2.508 3.771 4.039 4.039 0 0 0 1.566.3h101.852a4.04 4.04 0 0 0 2.892-1.181 4.023 4.023 0 0 0 1.182-2.89V4.089a4.082 4.082 0 0 0-4.074-4.07z" fill="%23A6A6A6"/>%0D%0A <path d="M39.122 8.323a2.216 2.216 0 0 1-.57 1.628 2.558 2.558 0 0 1-3.585 0 2.393 2.393 0 0 1-.734-1.794 2.394 2.394 0 0 1 .734-1.785 2.395 2.395 0 0 1 1.792-.736c.34.004.676.087.978.244.292.122.546.318.736.57l-.407.407a1.52 1.52 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57 1.677 1.677 0 0 0-.573 1.384 1.675 1.675 0 0 0 .57 1.384c.355.336.817.538 1.304.57a1.789 1.789 0 0 0 1.386-.57 1.347 1.347 0 0 0 .407-.976h-1.793v-.652h2.366v.326h-.003zm3.748-2.036h-2.2v1.547h2.038v.57H40.67v1.547h2.2v.651h-2.854V5.718h2.855v.57zm2.69 4.315h-.653V6.287h-1.385v-.57h3.422v.57H45.56v4.315zm3.747 0V5.718h.652v4.884h-.652zm3.423 0h-.652V6.287h-1.385v-.57h3.34v.57h-1.385v4.315h.082zm7.74-.65a2.559 2.559 0 0 1-3.585 0 2.394 2.394 0 0 1-.736-1.792 2.393 2.393 0 0 1 .736-1.791 2.558 2.558 0 0 1 3.586 0 2.395 2.395 0 0 1 .735 1.791 2.391 2.391 0 0 1-.736 1.791zm-3.096-.408c.346.35.812.554 1.304.57a1.623 1.623 0 0 0 1.304-.57c.366-.369.57-.867.57-1.387a1.675 1.675 0 0 0-.57-1.381 1.924 1.924 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57c-.365.367-.57.864-.57 1.381a1.676 1.676 0 0 0 .57 1.387zm4.726 1.058V5.718h.736l2.366 3.826V5.718h.651v4.884h-.657l-2.523-3.989v3.99H62.1z" fill="%23fff" stroke="%23fff" stroke-width=".2" stroke-miterlimit="10"/>%0D%0A <path d="M55.989 17.767a3.43 3.43 0 0 0-3.258 2.149c-.173.43-.256.89-.246 1.352a3.47 3.47 0 0 0 2.159 3.241c.427.175.884.263 1.345.26a3.432 3.432 0 0 0 3.258-2.15c.172-.429.256-.889.245-1.351a3.376 3.376 0 0 0-3.503-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-7.578-5.536a3.431 3.431 0 0 0-3.258 2.149c-.172.43-.256.89-.246 1.352a3.472 3.472 0 0 0 2.16 3.241c.426.175.883.263 1.344.26a3.432 3.432 0 0 0 3.258-2.15c.173-.429.256-.889.246-1.351a3.376 3.376 0 0 0-3.504-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-9.044-4.478v1.466h3.503a3.077 3.077 0 0 1-.815 1.872 3.607 3.607 0 0 1-2.688 1.059 3.796 3.796 0 0 1-3.83-3.908 3.838 3.838 0 0 1 2.347-3.605c.47-.198.973-.301 1.483-.303a4.041 4.041 0 0 1 2.688 1.056l1.06-1.056a5.223 5.223 0 0 0-3.667-1.466 5.49 5.49 0 0 0-5.46 5.373 5.49 5.49 0 0 0 5.46 5.374 4.693 4.693 0 0 0 3.748-1.547 4.9 4.9 0 0 0 1.304-3.42c.017-.3-.01-.6-.082-.892h-5.051v-.003zm36.992 1.14a3.163 3.163 0 0 0-2.933-2.198c-1.793 0-3.26 1.384-3.26 3.5a3.406 3.406 0 0 0 3.423 3.502 3.345 3.345 0 0 0 2.852-1.547l-1.141-.814a1.986 1.986 0 0 1-1.711.976 1.769 1.769 0 0 1-1.711-1.058l4.644-1.954-.163-.407zm-4.726 1.14a1.977 1.977 0 0 1 1.793-2.035 1.441 1.441 0 0 1 1.303.732l-3.096 1.303zm-3.83 3.34h1.549V14.267h-1.548v10.18zm-2.444-5.943a2.682 2.682 0 0 0-1.874-.814 3.502 3.502 0 0 0-3.34 3.501 3.369 3.369 0 0 0 2.048 3.149c.409.174.848.266 1.292.27a2.34 2.34 0 0 0 1.793-.814h.081v.489c0 1.302-.736 2.035-1.874 2.035a1.81 1.81 0 0 1-1.711-1.221l-1.304.57a3.36 3.36 0 0 0 3.096 2.035c1.793 0 3.26-1.058 3.26-3.582v-6.19h-1.467v.572zm-1.792 4.804a2.025 2.025 0 0 1-1.956-2.117 2.02 2.02 0 0 1 1.956-2.117 1.961 1.961 0 0 1 1.874 2.117 1.957 1.957 0 0 1-1.875 2.114v.003zm19.881-9.035h-3.667v10.175h1.548v-3.83h2.119a3.185 3.185 0 0 0 3.087-1.92 3.177 3.177 0 0 0-1.82-4.237 3.185 3.185 0 0 0-1.267-.193v.005zm.082 4.885h-2.2V15.65h2.2a1.788 1.788 0 0 1 1.792 1.71 1.862 1.862 0 0 1-1.793 1.791v.005zm9.37-1.465c-1.14 0-2.282.488-2.689 1.547l1.385.57a1.438 1.438 0 0 1 1.385-.736 1.532 1.532 0 0 1 1.63 1.303v.079a3.236 3.236 0 0 0-1.548-.407c-1.467 0-2.934.814-2.934 2.28a2.386 2.386 0 0 0 2.524 2.279 2.294 2.294 0 0 0 1.955-.977h.082v.817h1.466v-3.908a3.08 3.08 0 0 0-3.259-2.85l.003.003zm-.163 5.617c-.489 0-1.222-.244-1.222-.893 0-.814.896-1.058 1.63-1.058.48.002.954.113 1.385.326a1.895 1.895 0 0 1-1.793 1.62v.005zm8.555-5.373-1.71 4.396H99.5l-1.793-4.396h-1.63l2.69 6.188-1.549 3.419h1.548l4.153-9.607h-1.629.002zm-13.688 6.51h1.548V14.267h-1.548v10.18z" fill="%23fff"/>%0D%0A <path d="M8.974 6.125a1.59 1.59 0 0 0-.326 1.14v17.992a1.61 1.61 0 0 0 .408 1.14l.081.081 10.104-10.095v-.163L8.974 6.125z" fill="url(%23nqixmws78b)"/>%0D%0A <path d="m22.5 19.802-3.34-3.338v-.244l3.34-3.338.081.082 3.99 2.28c1.141.65 1.141 1.709 0 2.36L22.5 19.802z" fill="url(%23euwe5vohvc)"/>%0D%0A <path d="m22.581 19.72-3.422-3.418L8.974 26.477c.408.407.978.407 1.711.082l11.896-6.84z" fill="url(%23wso0uh08dd)"/>%0D%0A <path d="M22.581 12.882 10.685 6.125c-.736-.407-1.303-.326-1.71.081l10.184 10.096 3.422-3.42z" fill="url(%23mrdt54dj1e)"/>%0D%0A <path opacity=".2" d="m22.5 19.64-11.815 6.675a1.334 1.334 0 0 1-1.63 0l-.08.082.08.081a1.333 1.333 0 0 0 1.63 0L22.5 19.64z" fill="%23000"/>%0D%0A <path opacity=".12" d="M8.974 26.316a1.59 1.59 0 0 1-.326-1.14v.081a1.61 1.61 0 0 0 .408 1.14v-.081h-.082zm17.6-8.956L22.5 19.64l.081.08 3.993-2.279a1.355 1.355 0 0 0 .815-1.14c0 .408-.326.733-.815 1.059z" fill="%23000"/>%0D%0A <path opacity=".25" d="m10.685 6.206 15.89 9.037c.488.326.814.651.814 1.059a1.352 1.352 0 0 0-.815-1.14L10.685 6.125c-1.143-.652-2.037-.163-2.037 1.14v.08c0-1.22.894-1.79 2.037-1.139z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <linearGradient id="nqixmws78b" x1="18.265" y1="27.13" x2="2.062" y2="22.737" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2300A0FF"/>%0D%0A <stop offset=".007" stop-color="%2300A1FF"/>%0D%0A <stop offset=".26" stop-color="%2300BEFF"/>%0D%0A <stop offset=".512" stop-color="%2300D2FF"/>%0D%0A <stop offset=".76" stop-color="%2300DFFF"/>%0D%0A <stop offset="1" stop-color="%2300E3FF"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="euwe5vohvc" x1="28.064" y1="17.927" x2="8.353" y2="17.927" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FFE000"/>%0D%0A <stop offset=".409" stop-color="%23FFBD00"/>%0D%0A <stop offset=".775" stop-color="orange"/>%0D%0A <stop offset="1" stop-color="%23FF9C00"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="wso0uh08dd" x1="20.731" y1="16.06" x2="7.736" y2="-5.775" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FF3A44"/>%0D%0A <stop offset="1" stop-color="%23C31162"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="mrdt54dj1e" x1="6.443" y1="34.068" x2="12.205" y2="24.305" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2332A071"/>%0D%0A <stop offset=".069" stop-color="%232DA771"/>%0D%0A <stop offset=".476" stop-color="%2315CF74"/>%0D%0A <stop offset=".801" stop-color="%2306E775"/>%0D%0A <stop offset="1" stop-color="%2300F076"/>%0D%0A </linearGradient>%0D%0A <clipPath id="oefv1zwvza">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)