Snabblänkar

Citizens Raises Enova Price Target to $180 on Grasshopper Bank Charter Synergies

Datasnapshot

Viktiga punkter

- •Citizens raised ENVA's price target to $180 from $149 (Market Outperform), citing bank charter benefits from the $369M Grasshopper Bancorp acquisition.

- •The Grasshopper deal gives Enova access to lower-cost deposit funding — a structural upgrade that reduces its historical non-bank lending disadvantage.

- •Deal close is expected in H2 2026, creating a multi-month window for positioning with regulatory approval as the key binary risk.

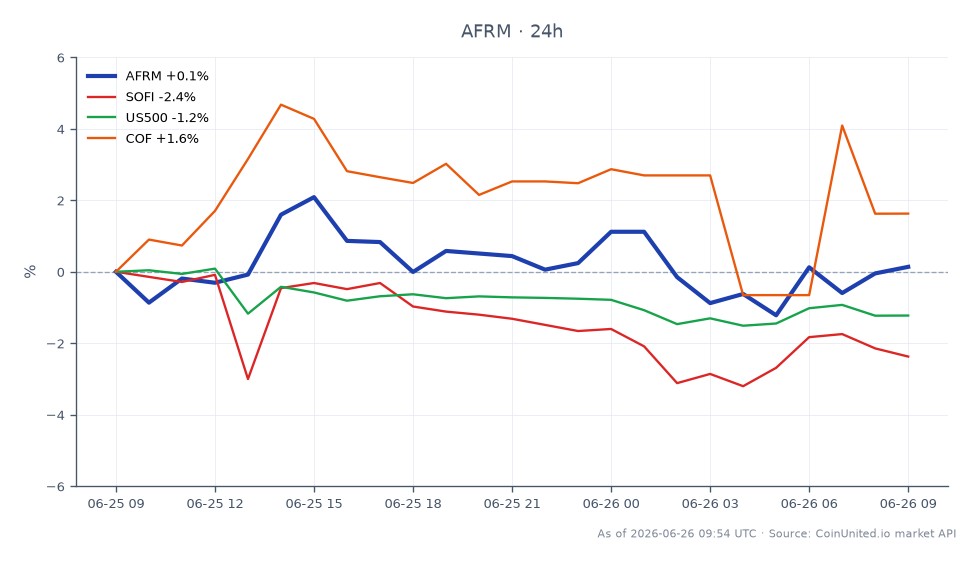

- •Sector read-through is moderate: specialty lenders like Affirm and SoFi could see sympathetic sentiment lift if investors broaden the bank-charter re-rating thesis.

- •This deal exemplifies the cross-sector acquisition repricing wave in fintech, where charter access is becoming a core valuation driver.

According to Investing.com and Yahoo Finance, Citizens raised its price target on Enova International, Inc. (NYSE: ENVA) to $180 from $149, maintaining a Market Outperform rating. The catalyst is Enov

Event Analysis

According to Investing.com and Yahoo Finance, Citizens raised its price target on Enova International, Inc. (NYSE: ENVA) to $180 from $149, maintaining a Market Outperform rating. The catalyst is Enova's pending acquisition of Grasshopper Bancorp, Inc. — a cash-and-stock deal valued at approximately $369 million, according to SEC filings. The deal is expected to close in the second half of 2026.

The strategic logic here is more significant than a typical analyst upgrade. Enova operates in non-prime consumer and small business lending — a segment that has historically faced higher cost-of-capital headwinds compared to bank-chartered lenders. By acquiring Grasshopper, Enova gains a bank charter, unlocking access to lower-cost deposit funding and potentially improving net interest margins meaningfully. This is a structural upgrade to the business model, not just a bolt-on deal — and analysts are repricing accordingly.

What distinguishes this from prior fintech M&A is the charter angle. Non-bank lenders like Enova have long competed at a structural funding disadvantage against chartered institutions. Grasshopper provides a path to close that gap, mirroring a broader trend in the M&A acquisition wave where specialty finance players pursue bank charters as a competitive moat. This deal fits squarely within the cross-sector acquisition repricing theme reshaping financial services valuations in 2026.

What This Means for Traders

The sentiment shift here is risk-on for ENVA specifically, with a 21% target price increase signaling that institutional analysts believe the market has not yet fully priced in the funding-cost improvements the Grasshopper deal enables. With deal close expected in H2 2026, there is a multi-month runway for positioning — but the stock remains sensitive to regulatory approval risk and broader credit-cycle conditions. Traders should watch for any updates on deal approval timelines as binary catalysts.

The read-through to sector peers is moderate but real. Online lenders with similar non-prime or SMB exposure — including Affirm Holdings, Inc. and SoFi Technologies, Inc. — may see marginal sentiment lift if investors extrapolate the thesis that bank charter access rerate specialty lenders broadly. Capital One Financial Corporation and the broader S&P 500 Index financials sector are less directly affected, but any re-rating in fintech credit multiples feeds into sector rotation flows. For a deeper framework on how buyout-driven repricing works across comparable names, see our guide on acquisition repricing.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Vanliga Frågor

Bank charters allow access to federally insured deposit funding, which is structurally cheaper than the wholesale and securitization funding non-bank lenders rely on — improving margins and reducing earnings volatility across credit cycles.

Fortsätt Utforska

Ansvarsfriskrivning: Denna sammanfattning är endast för utbildningsändamål och utgör inte investeringsrådgivning.