Быстрые ссылки

Japan June PPI Surges to +7.1% y/y: BoJ Tightening Risk Spikes, JPY Crosses and JGBs Face Volatility

Снимок данных

Основные выводы

- •Japan June PPI beat at +7.1% y/y (vs. 6.8% expected, 6.3% prior) is the strongest producer inflation print since March 2023, driven by yen weakness, energy costs, and Middle East supply disruptions.

- •Leveraged JPY cross positions (USD/JPY, EUR/JPY, AUD/JPY, GBP/JPY) face two-way liquidation risk: BoJ hawkish repricing strengthens JPY; continued yen weakness extends the carry trade but deepens inflation.

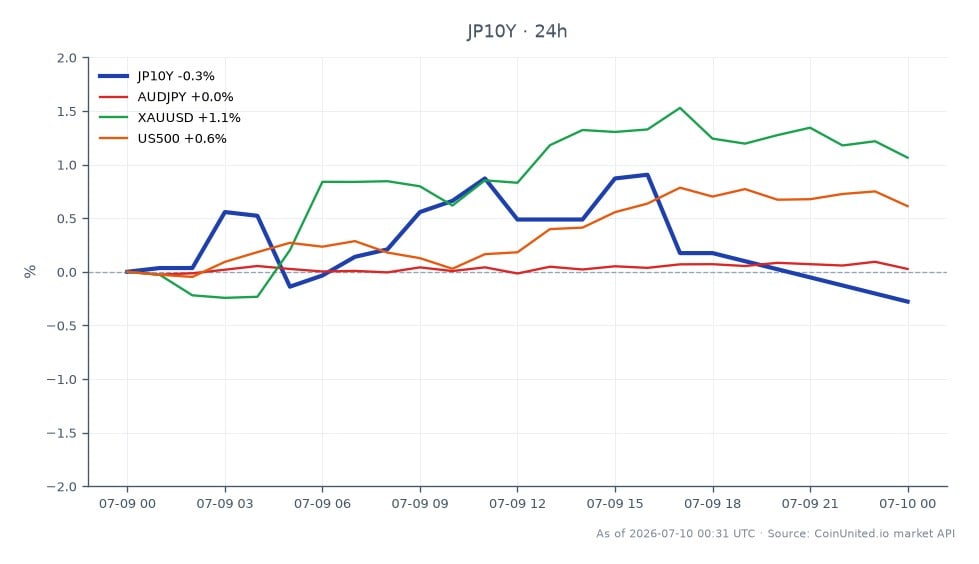

- •Japan 10Y yield (JP10Y) holds at 2.88% — a sustained break higher signals bond market capitulation to BoJ tightening expectations and weighs on global duration assets including Nikkei and US growth equities.

- •Cross-market spillover: higher global yields and potential carry unwinds can reduce risk appetite for Bitcoin and other high-beta assets; gold benefits from the inflation-hedge narrative.

- •This is a structurally-driven shock (weak yen + energy costs + freight), not transitory — CPI pass-through and wage dynamics are the next catalysts to watch for sustained BoJ policy repricing.

Japan's June 2026 Corporate Goods Price Index (PPI) printed at +7.1% y/y, beating the consensus forecast of +6.8% and accelerating sharply from May's +6.3%. According to MaceNews preview data and Trad

Event Summary

Japan's June 2026 Corporate Goods Price Index (PPI) printed at +7.1% y/y, beating the consensus forecast of +6.8% and accelerating sharply from May's +6.3%. According to MaceNews preview data and Trading Economics, this marks the fastest producer inflation in Japan since March 2023, completing a dramatic surge from near-2% readings seen through mid-2025. As reported by Reuters, Japan's services PPI for May had already flagged structural pressure — a 61.8% surge in ocean freight and a 17.3% rise in international air transport costs tied to elevated fuel prices.

The drivers are structural, not transitory: a weakened yen (at its lowest vs. the dollar since December 1986, per available source commentary), persistently elevated Middle East-linked energy costs, and rising prices for fuels, non-ferrous metals, chemicals, and plastics. As detailed in our BOJ Policy & Japan Inflation trader's guide, the yen weakness–imported inflation–BoJ reaction loop is now tightening at an accelerating pace.

Leverage Impact Analysis

This print is a high-volatility catalyst for JPY crosses. The BoJ inflation overshoot policy risk theme is now squarely in play — and leveraged FX positions face meaningful liquidation risk in both directions.

USD/JPY scenario: If the market reads this as a BoJ hawkish catalyst, JPY strengthens. A trader holding a 100x long USD/JPY perpetual at 157.00 faces a ~157-pip adverse move per 1% JPY appreciation before a 1% margin wipe — approximately a 1.57-pip stop zone. At 200x leverage, that compresses further. Conversely, if markets focus on the ongoing yen weakness driving the inflation rather than the policy response, USD/JPY could extend higher, liquidating short positions.

JGB yields (JP10Y): Live market data shows the Japan 10-Year at 2.88% (24h range flat at 2.88%). A PPI shock of this magnitude historically pressures short-end JGBs higher and steepens the curve. Leveraged long JGB positions face mark-to-market losses if yields reprice upward; monitor for a break above recent highs.

EUR/JPY, AUD/JPY, GBP/JPY: Carry-funded positions are most vulnerable. A sudden JPY spike tied to BoJ repricing could trigger cascade liquidations across the ECB & BOJ macro inflation divergence theme. Reduce leverage or widen stops ahead of any BoJ commentary.

Cross-Market Impact

The macro inflation pressure narrative extends well beyond Japanese assets:

- -Nikkei 225 / TOPIX (JAP225, JAPTOPIX): Cost-sensitive industrials, transportation, and manufacturers face margin compression from higher input costs. Japanese financial stocks may benefit from a steeper yield curve if BoJ tightening expectations firm.

- -Gold (XAUUSD): Persistent global inflation — Japan PPI adds to a pattern seen in US wholesale data — reinforces inflation-hedge asset rotation. Gold's inverse relationship with real yields is directly relevant if JGB yields rise faster than nominal expectations.

- -US 10Y (US10Y): A hawkish BoJ pivot could reduce Japanese institutional demand for US Treasuries (as domestic yields become more attractive), adding upward pressure on US yields and weighing on the S&P 500 via discount rate expansion.

- -Bitcoin (BTC): Indirect but real — tighter global liquidity and higher yields compress risk appetite. Carry unwinds funded in JPY can trim leveraged crypto exposure. Monitor funding rates on CoinUnited.io for positioning shifts.

- -Australian Dollar / Japanese Yen: AUD/JPY is a key carry trade barometer — a BoJ hawkish shift combined with RBA dynamics creates a high-volatility cross worth monitoring closely.

Trading Considerations

Key levels to watch: USD/JPY resistance and the structural yen weakness trend versus policy-driven JPY strength. The JP10Y at 2.88% is a near-term pivot — a sustained move higher confirms bond market repricing. For JPY crosses, the critical question is whether BoJ rhetoric follows the data; watch for any inter-meeting commentary or official statements referencing import-driven inflation as a policy trigger. For the full USD/JPY framework, see our USD/JPY carry trade guide.

Position sizing discipline is essential. With leverage relevance rated 0.82 on this event, this is not a set-and-forget trade. Confirm directional bias with funding rate data and open interest trends before scaling in.

Trade Japan 10 Year Yield on CoinUnited.io

Trade JP10Y with up to 2000xx leverage → | Create Free Account

Часто задаваемые вопросы

At 100x leverage on a USD/JPY long, a 1% JPY appreciation erases roughly the full margin — the ambiguity between a BoJ hawkish read (JPY strength) and a continued weak-yen read creates two-way liquidation risk. Reduce position size or widen stops until BoJ direction is confirmed.

Продолжить исследование

Отказ от ответственности: Этот бриф предназначен только для образовательных целей и не является инвестиционной рекомендацией.