Быстрые ссылки

Delta Air Lines Beats June Quarter Guidance, Forecasts Strong Q3: Leverage Scenarios & Airline Sector Ripple Effects

Снимок данных

Основные выводы

- •Delta reported Q2 2026 EPS of $1.00, beating its June quarter guidance target of ~$1B pre-tax profit despite absorbing more than $2B in fuel expense increases.

- •Q3 2026 EPS guidance of $2.00–$2.50/share, if above Street consensus, should trigger upward estimate revisions and potential multiple expansion for DAL.

- •Leveraged DAL CFD traders at 50x face liquidation on a ~2% adverse move from $90.85 — position sizing discipline and stop placement at or below the $88.10 session low are critical.

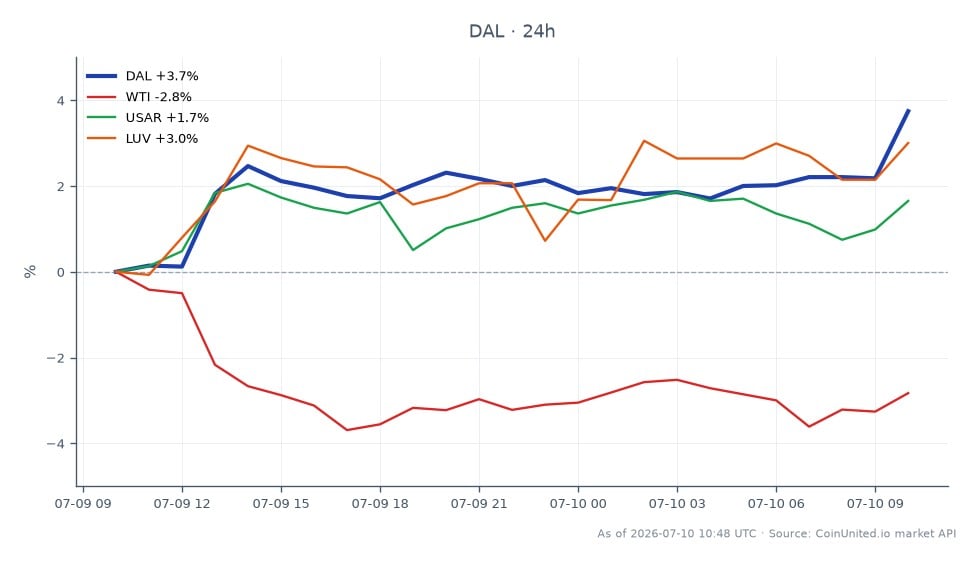

- •Strong Delta results are a positive cross-market read-through for UAL, AAL, and LUV, and serve as demand confirmation for refined products/WTI.

- •Continued net debt reduction ($760M in Q1 2026) improves DAL's credit profile relative to more leveraged airline peers, supporting relative value long positioning.

Delta Air Lines (DAL) delivered a June quarter 2026 earnings beat, reporting Q2 2026 EPS of $1.00 (per MarketBeat aggregation), ahead of company guidance. The result follows a Q1 2026 non-GAAP EPS of

Event Summary

Delta Air Lines (DAL) delivered a June quarter 2026 earnings beat, reporting Q2 2026 EPS of $1.00 (per MarketBeat aggregation), ahead of company guidance. The result follows a Q1 2026 non-GAAP EPS of $0.64 and management's March 2026 guidance for approximately $1 billion in June quarter pre-tax profit — achieved despite absorbing more than a $2 billion increase in fuel expense at the forward curve, according to Delta's investor relations releases. Delta also issued constructive Q3 2026 EPS guidance in the $2.00–$2.50/share range, with the company projecting low-teens revenue growth on flat capacity in the June quarter.

Key operating metrics from the March 2026 release show Q1 operating revenue of $14.2B (+~10% YoY), operating income of $652M (4.6% margin), and adjusted net debt down $760M from end-2025 to $13.5B — signaling continued deleveraging. The beat-and-raise pattern, combined with explicit fuel cost absorption, positions Delta as a sector bellwether ahead of peer reports from United Airlines Holdings and American Airlines.

Leverage Impact Analysis

DAL trades at $90.85 (24h range: $88.10–$92.59, +1.98%) on CoinUnited.io. With up to 2000x leverage available on stock CFDs, position sizing discipline is critical around earnings events.

Worked example — Long DAL CFD:

- -A 50x long DAL CFD opened at $90.85 controls $4,542.50 notional per unit. A 3% post-earnings move to ~$93.57 generates ~$136 gain per unit. However, a 2% reversal to $88.93 approaches the ~$1.82/unit margin buffer at 50x — illustrating how tight stops are essential.

- -At 20x leverage, a trader has a ~5% buffer (~$4.54/unit) before liquidation, providing more room to absorb intraday volatility around the $88.10 session low.

Key risk: Earnings beats often see "sell the news" reversals, particularly when guidance is already priced in. Traders holding >50x long positions through any Q3 guidance disappointment face rapid liquidation. Monitor whether Q3 EPS guidance ($2.00–$2.50) sits above or below Street consensus — the gap determines whether upward estimate revisions force a sustained re-rating or a one-day pop fades. For a broader framework, see how to trade earnings beats.

Cross-Market Impact

Airline peers: A strong DAL print is a direct positive read-through for United Airlines Holdings, Inc. (UAL), American Airlines Group Inc. (AAL), and Southwest Airlines Co. (LUV). If Delta absorbed $2B+ in fuel costs while staying profitable, the market will re-examine peer margin assumptions — particularly for more fuel-exposed carriers like AAL.

WTI Crude / Jet Fuel: Delta's confirmed resilience in absorbing elevated fuel costs is demand-confirmatory for refined products. WTI Light Crude Oil traders can treat this as a signal that air travel demand remains inelastic even at high jet fuel prices — marginally supportive of the energy demand thesis, though insufficient to move oil prices alone.

Macro / Consumer: Low-teens revenue growth on flat capacity implies strong fare pricing power — a data point consistent with resilient U.S. consumer and corporate travel spending. This marginally supports broader consumer discretionary sentiment and indices, though the macro spillover is second-order. For the broader 2026 stocks market outlook, airline strength adds to the consumer-cyclical picture.

Trading Considerations

DAL's key technical levels to watch: the 24h high of $92.59 acts as immediate resistance; a sustained break above opens toward prior swing highs. The $88.10 session low is the near-term support floor — a close below this level on high volume would signal the beat is already priced in. Volume confirmation of any post-earnings breakout is critical; absent that, the move risks fading.

The primary risk factor remains fuel. Delta's explicit reference to a $2B+ fuel expense headwind being absorbed through pricing and capacity discipline means any WTI spike or jet fuel cost acceleration beyond current forward curves could reverse the margin narrative quickly. Watch Q3 guidance vs. sell-side consensus updates in the hours following the release for directional confirmation. Earnings beat sector playbooks provide additional frameworks for positioning around these setups.

Trade Delta Air Lines, Inc. on CoinUnited.io

Trade DAL with up to 1000xx leverage → | Create Free Account

Часто задаваемые вопросы

At 50x leverage with DAL at $90.85, a 2% adverse move to ~$88.93 approaches liquidation — so the $88.10 session low is the key stop reference. A sustained move above $92.59 resistance on volume would validate the long thesis with room to run.

Продолжить исследование

Отказ от ответственности: Этот бриф предназначен только для образовательных целей и не является инвестиционной рекомендацией.