Быстрые ссылки

Renault Takes Full Control of Flexis: What the Electric Van Power Grab Means for European Auto Stocks

Основные выводы

- •Renault becomes 100% owner of Flexis SAS, acquiring Volvo's 45% and CMA CGM's 10% stakes pending regulatory approval expected by H1 2026.

- •The Renault Trafic Van E-Tech electric production timeline at Sandouville, France remains on track for end-2026 — operational continuity is confirmed.

- •Full ownership concentrates both upside and execution risk on Renault's balance sheet; sell-side capex and EV margin models will likely be revised.

- •Volvo's exit frees capital for its core heavy-truck electrification priorities; CMA CGM refocuses on shipping and logistics operations.

- •Competitive pressure intensifies on European electric LCV rivals including Stellantis as Renault gains full strategic control over a purpose-built EV van platform.

As reported by Renault Group and corroborated by Automotive Logistics, Renault signed a binding agreement on 23 February 2026 to acquire Volvo Group's 45% stake and CMA CGM's 10% stake in Flexis SAS,

Event Analysis

As reported by Renault Group and corroborated by Automotive Logistics, Renault signed a binding agreement on 23 February 2026 to acquire Volvo Group's 45% stake and CMA CGM's 10% stake in Flexis SAS, giving Renault 100% ownership of the electric van joint venture originally formed in 2024. The transaction is subject to regulatory and antitrust approvals, with an expected closing by end of H1 2026. Simultaneously, Krishnan Sundararajan replaced outgoing CEO Philippe Divry, signalling an operational reset under full Renault command.

Flexis was conceived as a purpose-built electric light commercial vehicle (LCV) platform — a dedicated EV skateboard architecture designed for modular van configurations. The first production model, the Renault Trafic Van E-Tech electric, is set to roll off the Sandouville, France production line by end of 2026, a timeline that remains unchanged despite the ownership restructuring. Prior disclosures suggested Renault and Volvo each committed approximately EUR 300 million to the venture, underscoring the strategic scale involved.

What distinguishes this deal from a routine JV dissolution is the *asymmetry of intent*. Volvo exits to sharpen focus on heavy trucks and construction equipment electrification — both capital-hungry priorities. CMA CGM retreats from manufacturing equity back to its core shipping and logistics operations. Renault, by contrast, is doubling down: absorbing 100% of capex risk to secure full commercial and technological control over a platform it sees as central to European fleet electrification. This fits squarely within the broader global acquisition and consolidation wave reshaping European industrials.

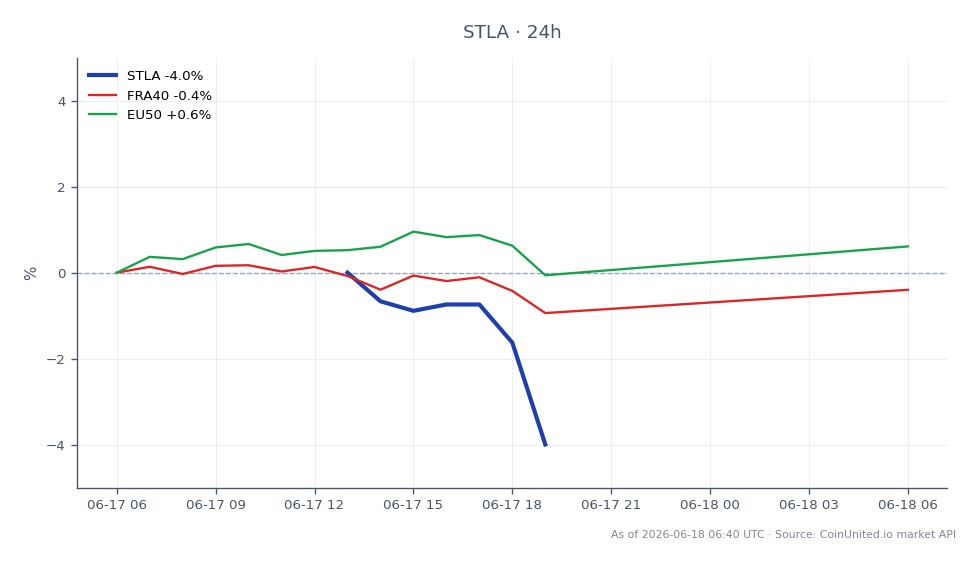

The strategic implication is significant for the European EV commercial segment. Full OEM ownership of a dedicated electric van platform accelerates decision-making and potentially expands licensing or platform-sharing optionality — putting competitive pressure on rivals including Stellantis N.V., Ford, and Mercedes-Benz Vans in the growing zero-emission LCV space. This is the kind of cross-sector acquisition repricing event that gradually reshapes sector valuations.

What This Means for Traders

For Renault equity (Euronext Paris), this is a medium-term structural catalyst rather than an immediate price shock. The bullish read is straightforward: full control means Renault can accelerate EV product strategy, unlock platform economics, and capture 100% of upside if electric LCVs outperform. The bearish counterweight is equally clear — Renault now absorbs 100% of execution, capex, and demand risk previously shared with two well-capitalised partners. Sell-side models will likely adjust medium-term capex assumptions and EV mix projections, which could create volatility around analyst note updates.

For index traders, Renault's weighting in the CAC 40 Index and the EURO STOXX 50 Index means any sentiment shift in French or European autos feeds through to broader index exposure. The event reinforces the European green-industrial investment narrative, which is incrementally supportive for Eurozone industrial and ESG-tilted index positioning. This deal is part of the wider M&A acquisition wave that has been repricing European industrial equities throughout 2025–2026.

Volvo Group's exit is likely neutral to mildly positive on capital discipline grounds — freeing resources for core truck platform electrification. Traders positioned in Volvo should monitor whether proceeds are disclosed and how management frames capital redeployment on the next earnings call.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Часто задаваемые вопросы

No explicit transaction value has been disclosed. Prior JV commitments suggested Renault and Volvo each planned to invest approximately EUR 300 million in Flexis, giving a rough order of magnitude for the platform's strategic value.

Продолжить исследование

Отказ от ответственности: Этот бриф предназначен только для образовательных целей и не является инвестиционной рекомендацией.