Hurtiglenker

Solstice CEO Pushes Back on 'Misread' ESI Deal as Acquirer Drops ~12%

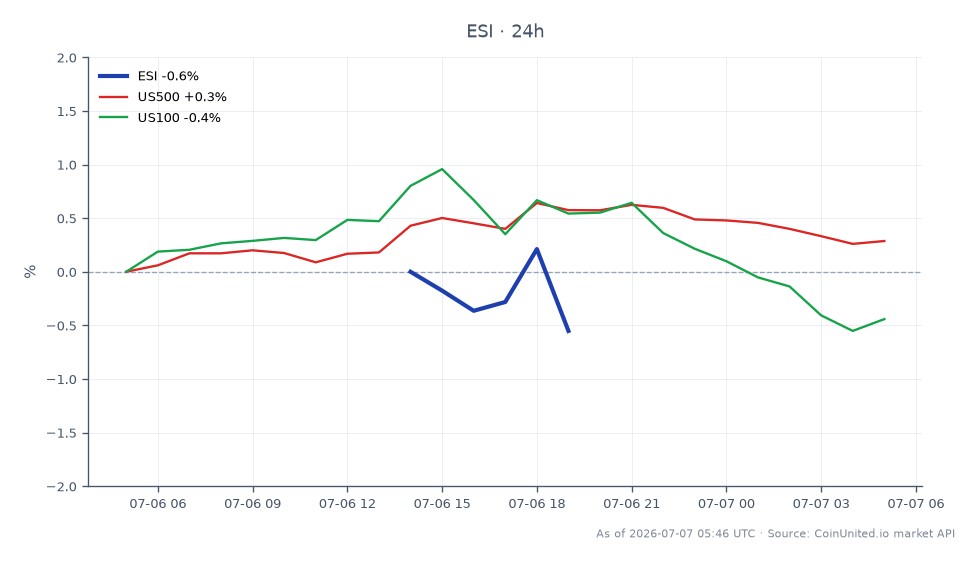

Datasnapshot

Viktige punkter

- •ESI trades below the ~$50.10 implied deal price at $42.34, offering a merger spread trade for risk-arbitrage players willing to hold through the H1 2027 close.

- •SOLS's ~12% drop reflects leverage and dilution concerns on a newly independent company, not necessarily rejection of the strategic rationale.

- •The $4.7B Goldman Sachs bridge commitment must be refinanced — permanent debt terms will be a key re-rating catalyst for SOLS.

- •The combined entity's semiconductor and electronics materials exposure makes this relevant to AI infrastructure supply chain themes.

- •Specialty chemicals peers may face valuation re-rating as the market prices in accelerating consolidation in advanced materials.

As reported by Reuters and confirmed via a company press release, Solstice Advanced Materials (Nasdaq: SOLS) — a recent Honeywell spinoff — agreed to acquire specialty chemicals maker Element Solution

Event Analysis

As reported by Reuters and confirmed via a company press release, Solstice Advanced Materials (Nasdaq: SOLS) — a recent Honeywell spinoff — agreed to acquire specialty chemicals maker Element Solutions (NYSE: ESI) in a definitive cash-and-stock transaction valued at approximately $14.5 billion including net debt. Element shareholders receive $10.00 cash plus 0.500 SOLS shares per ESI share, implying consideration of roughly $50.10 per share — a ~15% premium to ESI's July 2, 2026 closing price of $43.64. The deal was unanimously approved by both boards and is expected to close in H1 2027, with Solstice securing a $4.7 billion bridge commitment from Goldman Sachs.

The strategic logic centers on scale: the combined entity would become an industry-leading advanced materials platform supplying inputs to semiconductor manufacturing, electronics, and industrial end markets. Management cited faster growth, strong margins, and meaningful cash conversion as deal rationale. ESI shareholders will own approximately 44% of the combined company, with David Sewell serving as President and CEO post-close.

What makes this deal notable within the broader M&A acquisition wave is the scale of market skepticism. Solstice fell roughly 11.8–13% on announcement — a reaction the CEO has publicly characterized as a misread. This kind of acquirer punishment is typical when a newly independent company takes on significant leverage early in its public life. The $4.7 billion bridge facility layered onto a relatively young balance sheet raises legitimate questions about near-term earnings accretion timing and integration execution risk, especially given the H1 2027 close horizon.

The deal also connects to the cross-sector acquisition repricing dynamic in specialty materials, where consolidation is accelerating as companies position for AI infrastructure and semiconductor supply chain demand. Peers in advanced materials and specialty chemicals may see valuation re-rating as the market processes what a combined SOLS-ESI platform implies for competitive positioning.

What This Means for Traders

For ESI holders, the deal structure creates a classic acquisition arbitrage setup. At the current ESI price of $42.34 (per live market data), shares trade below the ~$50.10 implied deal consideration, reflecting the standard merger spread that compensates for regulatory, financing, and shareholder vote risk over the ~12-month close window. The key variables to watch: antitrust review given the semiconductor supply chain exposure, and whether Solstice successfully replaces the Goldman bridge with permanent debt on acceptable terms.

For SOLS, the near-term overhang is the leverage profile and dilution from issuing stock as deal currency. The acquirer's ~12% drop is the market pricing in execution risk, not necessarily rejecting the strategic thesis. If the CEO's pushback gains traction — particularly if management provides clearer accretion timelines or synergy specifics — there is a potential re-rating catalyst. Traders should watch for follow-up investor day communications or revised financial guidance as potential short-term inflection points.

Broader read-through exists for specialty chemicals and advanced materials peers, particularly those with semiconductor supply chain geopolitics exposure. The deal signals that scale consolidation in this niche is accelerating, which could trigger takeout speculation across comparable names.

Trade Element Solutions Inc. on CoinUnited.io

Trade ESI with up to 1000xx leverage → | Create Free Account

Ofte stilte spørsmål

The gap — known as the merger spread — reflects market-priced risk of deal failure due to regulatory review, shareholder votes, or financing complications before the expected H1 2027 close. A wider spread means the market assigns higher probability to the deal not completing at stated terms.

Fortsett Utforskningen

Ansvarsfraskrivelse: Denne briefen er kun for utdanningsformål og er ikke investeringsråd.

">%0D%0A <path d="m65.883 9.018.032 5.181h-1.223c-.773-3.733-2.671-5.73-5.797-5.73-4.441 0-6.5 4.442-6.5 9.913 0 5.985 2.38 10.588 6.79 10.588 3.024 0 5.084-1.898 6.211-6.597h1.287l-.482 6.05a13.606 13.606 0 0 1-7.434 1.93c-7.016 0-11.36-4.409-11.36-11.071 0-7.467 4.989-12.166 11.36-12.166a12.961 12.961 0 0 1 7.112 1.899M68.714 21.89c0-5.47 3.572-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.573 9.205-8.367 9.205a7.908 7.908 0 0 1-8.271-8.464zm11.876.354c0-4.762-1.095-8.406-3.669-8.406-2.38 0-3.478 2.703-3.478 6.92 0 4.762 1.126 8.431 3.701 8.431 2.382 0 3.444-2.735 3.444-6.956M93.236 27.555c0 1.126.515 1.318 2.03 1.416v1.062h-8.497V28.97c1.514-.097 2.03-.29 2.03-1.415V16.16l-1.93-1.126v-.611l5.663-1.77h.709l-.005 14.9zM88.345 8.18a2.625 2.625 0 0 1 5.246 0 2.625 2.625 0 0 1-5.246 0zM109.007 18.157c0-1.867-.709-2.8-2.479-2.8a6.474 6.474 0 0 0-3.604 1.319v10.877c0 1.126.482 1.319 1.962 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.93-1.126v-.612l5.76-1.77h.741l-.129 3.154a7.735 7.735 0 0 1 5.954-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.995 1.416v1.062h-8.432V28.97c1.48-.097 1.963-.29 1.963-1.416v-9.396zM123.52 21.851c0 3.927 1.706 6.308 5.247 6.308 3.54 0 5.985-1.867 5.985-6.5V10.82c0-1.74-.419-2.03-3.058-2.253V7.442h7.37v1.126c-2.252.258-2.574.515-2.574 2.253v11.425c0 5.535-3.797 8.116-8.561 8.116-5.697 0-9.108-2.64-9.108-8.174v-11.4c0-1.77-.321-1.965-2.574-2.221V7.44h9.849v1.126c-2.253.258-2.574.45-2.574 2.22l-.002 11.064zM152.26 18.157c0-1.867-.707-2.8-2.478-2.8a6.484 6.484 0 0 0-3.605 1.319v10.877c0 1.126.483 1.319 1.964 1.416v1.062h-8.432V28.97c1.513-.097 2.029-.29 2.029-1.416V16.16l-1.931-1.126v-.612l5.761-1.77h.74l-.129 3.154a7.731 7.731 0 0 1 5.953-3.153c3.025 0 4.602 1.739 4.602 5.245v9.655c0 1.126.514 1.319 1.996 1.416v1.062h-8.432V28.97c1.479-.097 1.962-.29 1.962-1.416v-9.396zM166.259 27.555c0 1.126.515 1.318 2.029 1.416v1.062h-8.496V28.97c1.512-.097 2.029-.29 2.029-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.709l-.003 14.9zM161.368 8.18a2.62 2.62 0 0 1 2.622-2.518 2.625 2.625 0 0 1 2.623 2.518 2.626 2.626 0 0 1-4.441 1.786 2.62 2.62 0 0 1-.804-1.786zM175.33 12.976h4.183v1.48h-4.183v10.652c0 1.964.741 2.8 2.253 2.8a3.755 3.755 0 0 0 2.414-.901l.387.58a5.65 5.65 0 0 1-4.956 2.768c-2.64 0-4.57-1.384-4.57-4.989v-10.91h-1.996v-.741a13.265 13.265 0 0 0 5.508-4.928h.965l-.005 4.189zM195.514 19.38v.741h-10.492c-.129 4.506 2.189 7.177 5.342 7.177a5.427 5.427 0 0 0 4.796-2.609l.515.29a6.75 6.75 0 0 1-6.888 5.374c-4.665 0-7.787-3.443-7.787-8.406 0-5.507 3.539-9.3 7.948-9.3 4.313 0 6.566 2.864 6.566 6.726m-10.427-.45h6.437c0-3.025-.805-5.085-2.899-5.085-2.125 0-3.283 2.125-3.541 5.084M207.001 7.054v-.676l5.696-1.545h.707v21.788c0 1.094.064 1.45 1.287 1.545l.805.064v.965l-5.857 1.16h-.838l.129-2.993a6.145 6.145 0 0 1-5.181 2.993c-3.895 0-6.5-3.154-6.5-8.046 0-6.087 3.604-9.59 8.206-9.59a5.117 5.117 0 0 1 3.478 1.126V8.048l-1.932-.994zm-5.342 13.709c0 3.926 1.609 6.855 4.538 6.855a3.901 3.901 0 0 0 2.736-1.03v-8.496c0-2.51-1.062-3.99-2.993-3.99-2.703 0-4.28 2.64-4.28 6.667M219.683 24.754a2.796 2.796 0 0 1 2.587 1.729 2.8 2.8 0 1 1-5.387 1.072 2.75 2.75 0 0 1 1.721-2.6 2.753 2.753 0 0 1 1.079-.2zM230.592 27.555c0 1.126.516 1.318 2.029 1.416v1.062h-8.501V28.97c1.512-.097 2.03-.29 2.03-1.415V16.16l-1.932-1.126v-.611l5.664-1.77h.708l.002 14.9zM225.7 8.18a2.626 2.626 0 0 1 4.441-1.787c.488.47.777 1.11.804 1.787a2.625 2.625 0 0 1-5.245 0zM233.842 21.89c0-5.47 3.573-9.236 8.367-9.236a7.95 7.95 0 0 1 8.271 8.496c0 5.471-3.572 9.205-8.366 9.205a7.904 7.904 0 0 1-7.809-5.179 7.904 7.904 0 0 1-.463-3.285zm11.876.354c0-4.762-1.094-8.406-3.669-8.406-2.382 0-3.479 2.703-3.479 6.92 0 4.762 1.126 8.431 3.7 8.431 2.382 0 3.444-2.735 3.444-6.956M18.386.684a17.469 17.469 0 1 0 0 34.937 17.469 17.469 0 0 0 0-34.937zm0 31.74a14.277 14.277 0 1 1 0-28.554 14.277 14.277 0 0 1 0 28.554z" fill="%23fff"/>%0D%0A <path d="M18.393 36.019a17.868 17.868 0 1 1 17.86-17.868 17.887 17.887 0 0 1-17.86 17.868zm0-34.938a17.07 17.07 0 1 0 17.063 17.07 17.089 17.089 0 0 0-17.063-17.07zm0 31.74a14.675 14.675 0 1 1 10.366-4.297 14.691 14.691 0 0 1-10.373 4.303m0-28.552a13.877 13.877 0 1 0 13.879 13.878A13.893 13.893 0 0 0 18.386 4.275z" fill="%23fff"/>%0D%0A <path d="M17.42 8.46a8.46 8.46 0 1 1-16.923 0 8.46 8.46 0 0 1 16.924 0" fill="%23E48A22"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="sy6kzo59ya">%0D%0A <path fill="%23fff" transform="translate(.5)" d="M0 0h250v36.019H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

"><path fill="%23fff" transform="scale(1.9886)" d="M27.72,2.61a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-30.14,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-32.16,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-36.18,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-34.18,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-40.2,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-58.29,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-62.32,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m30.14,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m22.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-72.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m26.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m34.16,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m24.12,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m18.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-64.32,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.06,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.36,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-70.34,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-68.34,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.27,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-56.29,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m16.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.01a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m14.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m8.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-50.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.1,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-52.25,2.02a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m10.05,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m20.09,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.03,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m-48.25,2a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m6.04,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m4.01,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m12.07,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2.02,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2m2,0a1,1,0,1,1,0,2a1,1,0,1,1,0-2"/><path d="M123.088,117.106a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M123.088,133.085a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M91.095,145.087a1.987,1.987,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989,2.01,2.01,0,0,1,1.989-1.988zM107.109,145.087a1.988,1.988,0,1,1,0,3.977,1.988,1.988,0,0,1-1.989-1.989c-.035-1.081.872-1.988,1.989-1.988zM115.098,145.087a1.987,1.987,0,1,1,0,3.977,1.987,1.987,0,0,1-1.988-1.989c-.035-1.081.872-1.988,1.988-1.988zM123.088,145.087a1.988,1.988,0,1,1,.002,3.976,1.988,1.988,0,0,1-.002-3.976z" fill="%23fff"/><path d="M151.069,149.064a1.988,1.988,0,1,1-1.989,1.989c-.035-1.082.872-1.989,1.989-1.989zM25.271,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491c0-1.575,1.277-2.852,2.83-2.852h6.492a2.852,2.852,0,0,1,2.852,2.852v6.49h.021z" fill="%23fff"/><path d="M33.38,30.568a2.852,2.852,0,0,1-2.852,2.851H7.798a2.852,2.852,0,0,1-2.851-2.851V7.817a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.75h-.021zM29.315,11.86a2.852,2.852,0,0,0-2.852-2.852H11.842A2.852,2.852,0,0,0,8.99,11.86v14.642a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852V11.86h-.021zM25.271,142.338a2.852,2.852,0,0,1-2.852,2.852h-6.49a2.852,2.852,0,0,1-2.853-2.852v-6.491a2.852,2.852,0,0,1,2.852-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.491z" fill="%23fff"/><path d="M33.38,150.468a2.852,2.852,0,0,1-2.852,2.852H7.798a2.852,2.852,0,0,1-2.851-2.852v-22.751a2.852,2.852,0,0,1,2.851-2.852H30.55a2.852,2.852,0,0,1,2.852,2.852v22.751h-.021zm-4.065-18.686a2.852,2.852,0,0,0-2.852-2.852H11.842a2.852,2.852,0,0,0-2.852,2.852v14.621a2.852,2.852,0,0,0,2.852,2.852h14.642a2.852,2.852,0,0,0,2.852-2.852v-14.621h-.021zM145.171,22.438a2.852,2.852,0,0,1-2.852,2.852h-6.491a2.851,2.851,0,0,1-2.851-2.852v-6.491a2.851,2.851,0,0,1,2.851-2.852h6.491a2.852,2.852,0,0,1,2.852,2.852v6.49z" fill="%23fff"/><path d="M153.301,30.568a2.852,2.852,0,0,1-2.852,2.851h-22.75a2.852,2.852,0,0,1-2.852-2.851V7.817a2.852,2.852,0,0,1,2.852-2.852h22.75a2.852,2.852,0,0,1,2.852,2.852v22.75zm-4.065-18.707a2.852,2.852,0,0,0-2.852-2.852h-14.621a2.852,2.852,0,0,0-2.851,2.852v14.642a2.852,2.852,0,0,0,2.851,2.852h14.621a2.852,2.852,0,0,0,2.852-2.852V11.86zM78.535,62.051c-9.176,0-16.607,7.431-16.607,16.607,0,9.176,7.431,16.607,16.607,16.607,9.176,0,16.607-7.431,16.607-16.607,0-9.176-7.431-16.607-16.607-16.607zm0,30.214c-7.501,0-13.572-6.07-13.572-13.572,0-7.501,6.07-13.572,13.572-13.572,7.501,0,13.572,6.07,13.572,13.572,0,7.501-6.071,13.572-13.572,13.572z" fill="%23fff"/><path d="M78.535,95.649c-9.385,0-16.991-7.64-16.991-16.99,0-9.386,7.64-16.992,16.99-16.992,9.386,0,16.992,7.64,16.992,16.991,0,9.35-7.64,16.991-16.991,16.991zm0-33.214c-8.966,0-16.258,7.292-16.258,16.258s7.291,16.258,16.258,16.258c8.966,0,16.258-7.291,16.258-16.258-.035-8.966-7.292-16.258-16.258-16.258zm0,30.214c-7.71,0-13.956-6.28-13.956-13.956,0-7.71,6.28-13.956,13.956-13.956,7.71,0,13.956,6.28,13.956,13.956,0,7.676-6.28,13.956-13.956,13.956zm0-27.179c-7.292,0-13.223,5.931-13.223,13.223,0,7.292,5.931,13.223,13.223,13.223,7.292,0,13.223-5.931,13.223-13.223-.035-7.292-5.966-13.223-13.223-13.223z" fill="%23fff"/><path d="M69.569,77.507a8.06,8.06,0,1,0,0-16.119,8.06,8.06,0,0,0,0,16.119z" fill="%23E48A22"/></g><defs><clipPath id="arusb4546a"><path fill="%23fff" transform="translate(0 .019)" d="M0,0h157v157H0z"/></clipPath></defs></svg>)

">%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23fff"/>%0D%0A <path d="M106.646 32.584H4.356A3.857 3.857 0 0 1 .5 28.741V3.867A3.853 3.853 0 0 1 4.355.02h102.29a3.86 3.86 0 0 1 3.855 3.848V28.74a3.853 3.853 0 0 1-3.854 3.845z" fill="%23A6A6A6"/>%0D%0A <path d="M109.771 28.74a3.117 3.117 0 0 1-1.929 2.882 3.123 3.123 0 0 1-1.195.237H4.355a3.127 3.127 0 0 1-3.13-3.119V3.867A3.126 3.126 0 0 1 4.355.743h102.292a3.127 3.127 0 0 1 3.125 3.124V28.74h-.001z" fill="%23000"/>%0D%0A <path d="M25.063 16.13a4.717 4.717 0 0 1 2.25-3.961 4.84 4.84 0 0 0-3.812-2.059c-1.603-.168-3.159.959-3.976.959-.833 0-2.09-.942-3.447-.915a5.079 5.079 0 0 0-4.271 2.603c-1.848 3.195-.47 7.89 1.3 10.472.886 1.265 1.92 2.679 3.274 2.626 1.325-.052 1.82-.84 3.417-.84 1.584 0 2.05.84 3.43.81 1.42-.021 2.317-1.27 3.171-2.546a10.434 10.434 0 0 0 1.452-2.952 4.572 4.572 0 0 1-2.786-4.197h-.003zm-2.61-7.718a4.643 4.643 0 0 0 1.065-3.33 4.74 4.74 0 0 0-3.064 1.583 4.42 4.42 0 0 0-1.092 3.207 3.917 3.917 0 0 0 3.091-1.46zM44.25 25.674H42.4l-1.015-3.183H37.86l-.966 3.183H35.09l3.493-10.838h2.156l3.509 10.838h.002zm-3.17-4.517-.918-2.83c-.097-.29-.28-.97-.547-2.042h-.033c-.108.461-.28 1.142-.515 2.042l-.902 2.83h2.914zm12.137.515a4.422 4.422 0 0 1-1.085 3.152 3.178 3.178 0 0 1-2.41 1.03 2.415 2.415 0 0 1-2.235-1.109v4.1H45.75v-8.417c0-.835-.021-1.691-.064-2.569h1.529l.097 1.239h.032a3.09 3.09 0 0 1 2.398-1.395 3.095 3.095 0 0 1 2.552 1.088c.645.817.973 1.84.925 2.88l-.001.001zm-1.77.064a3.22 3.22 0 0 0-.516-1.882 1.781 1.781 0 0 0-1.513-.771c-.427 0-.84.15-1.166.426-.349.284-.59.678-.684 1.118a2.26 2.26 0 0 0-.08.528v1.302a2.09 2.09 0 0 0 .525 1.44 1.737 1.737 0 0 0 1.36.587 1.783 1.783 0 0 0 1.529-.755c.389-.59.58-1.29.544-1.995v.002zm10.768-.064a4.422 4.422 0 0 1-1.084 3.152 3.182 3.182 0 0 1-2.413 1.03 2.415 2.415 0 0 1-2.233-1.109v4.1h-1.739v-8.417c0-.835-.021-1.691-.065-2.569h1.53l.096 1.239h.033a3.092 3.092 0 0 1 3.803-1.153c.443.189.836.478 1.148.846.645.817.973 1.84.924 2.88v.001zm-1.771.064a3.22 3.22 0 0 0-.517-1.882 1.778 1.778 0 0 0-1.511-.771c-.427 0-.841.15-1.168.426-.349.284-.59.678-.683 1.118-.048.172-.075.35-.082.528v1.302a2.097 2.097 0 0 0 .523 1.44 1.74 1.74 0 0 0 1.361.587 1.781 1.781 0 0 0 1.53-.755c.39-.59.581-1.289.547-1.995v.002zm11.831.9a2.893 2.893 0 0 1-.964 2.251 4.278 4.278 0 0 1-2.956.949 5.163 5.163 0 0 1-2.809-.675l.402-1.447a4.84 4.84 0 0 0 2.511.676 2.371 2.371 0 0 0 1.53-.442 1.444 1.444 0 0 0 .548-1.181 1.511 1.511 0 0 0-.452-1.11 4.188 4.188 0 0 0-1.496-.836c-1.9-.707-2.85-1.742-2.85-3.104a2.737 2.737 0 0 1 1.006-2.187 3.981 3.981 0 0 1 2.664-.852 5.27 5.27 0 0 1 2.463.515l-.437 1.415a4.31 4.31 0 0 0-2.084-.498 2.121 2.121 0 0 0-1.438.45 1.289 1.289 0 0 0-.437.982 1.327 1.327 0 0 0 .5 1.061 5.63 5.63 0 0 0 1.577.836c.78.274 1.485.725 2.06 1.318.45.521.686 1.192.663 1.88v-.002zm5.762-3.472H76.12v3.794c0 .965.338 1.447 1.014 1.447.26.006.52-.021.773-.08l.048 1.318a3.942 3.942 0 0 1-1.352.192 2.085 2.085 0 0 1-1.61-.63 3.077 3.077 0 0 1-.578-2.107v-3.94h-1.141v-1.302h1.141v-1.43l1.707-.515v1.943h1.915l-.001 1.31zm8.627 2.54a4.284 4.284 0 0 1-1.03 2.959 3.674 3.674 0 0 1-2.865 1.19 3.504 3.504 0 0 1-2.746-1.14 4.154 4.154 0 0 1-1.022-2.879 4.249 4.249 0 0 1 1.054-2.974 3.655 3.655 0 0 1 2.842-1.155 3.577 3.577 0 0 1 2.768 1.142 4.1 4.1 0 0 1 1 2.856v.001zm-1.802.04a3.496 3.496 0 0 0-.465-1.843 1.72 1.72 0 0 0-1.562-.931 1.746 1.746 0 0 0-1.594.93 3.554 3.554 0 0 0-.466 1.877 3.485 3.485 0 0 0 .466 1.844 1.782 1.782 0 0 0 3.141-.015 3.51 3.51 0 0 0 .48-1.863v.001zm7.454-2.356a3.03 3.03 0 0 0-.547-.047 1.641 1.641 0 0 0-1.42.692 2.605 2.605 0 0 0-.434 1.543v4.1H88.18v-5.355c0-.82-.017-1.64-.052-2.46h1.514l.063 1.495h.049c.164-.488.466-.918.868-1.239.363-.271.804-.419 1.257-.42.145 0 .29.01.435.032v1.656l.002.003zm7.774 2.011c.004.264-.017.528-.064.788h-5.214a2.262 2.262 0 0 0 .756 1.77 2.59 2.59 0 0 0 1.707.544c.72.01 1.435-.115 2.11-.368l.272 1.204a6.527 6.527 0 0 1-2.623.483 3.805 3.805 0 0 1-2.86-1.067 3.95 3.95 0 0 1-1.039-2.87 4.473 4.473 0 0 1 .967-2.942 3.331 3.331 0 0 1 2.734-1.253 2.916 2.916 0 0 1 2.56 1.253c.48.728.722 1.586.694 2.456v.002zm-1.658-.45a2.348 2.348 0 0 0-.337-1.335 1.518 1.518 0 0 0-1.384-.725 1.648 1.648 0 0 0-1.381.706c-.297.392-.475.86-.515 1.35h3.62l-.003.004zM37.359 11.005a11.12 11.12 0 0 1-1.25-.063v-5.24c.487-.075.98-.112 1.472-.11 1.994 0 2.912.98 2.912 2.576 0 1.842-1.085 2.837-3.134 2.837zm.292-4.742a3.49 3.49 0 0 0-.688.055v3.984c.192.02.385.028.578.023 1.306 0 2.05-.743 2.05-2.133-.002-1.24-.674-1.929-1.94-1.929zm5.702 4.78a1.832 1.832 0 0 1-1.755-1.225 1.826 1.826 0 0 1-.097-.75 1.87 1.87 0 0 1 1.916-2.031 1.817 1.817 0 0 1 1.851 1.968 1.881 1.881 0 0 1-1.915 2.04v-.002zm.032-3.382c-.617 0-1.012.577-1.012 1.383 0 .79.404 1.365 1.005 1.365.6 0 1.004-.616 1.004-1.383 0-.779-.396-1.363-.996-1.363V7.66zm8.29-.545-1.203 3.84h-.784L49.19 9.29a12.619 12.619 0 0 1-.309-1.24h-.016c-.07.42-.174.835-.308 1.24l-.53 1.668h-.792l-1.132-3.841h.878l.435 1.826c.103.435.19.845.263 1.232h.017c.062-.323.165-.727.315-1.225l.546-1.833h.696l.523 1.795c.126.435.229.861.309 1.264h.023c.062-.426.15-.848.262-1.264l.468-1.795h.84-.004zm4.426 3.84h-.854V8.75c0-.679-.263-1.02-.776-1.02a.888.888 0 0 0-.854.942v2.284h-.854v-2.74c0-.34-.009-.705-.032-1.1h.751l.04.593h.024a1.38 1.38 0 0 1 1.219-.67c.806 0 1.336.616 1.336 1.619v2.3-.002zm2.356 0h-.855v-5.6h.855v5.6zm3.115.088a1.832 1.832 0 0 1-1.851-1.976 1.87 1.87 0 0 1 1.914-2.031 1.816 1.816 0 0 1 1.851 1.968 1.88 1.88 0 0 1-1.914 2.04v-.001zm.032-3.383c-.617 0-1.012.578-1.012 1.383 0 .79.404 1.366 1.003 1.366.6 0 1.005-.617 1.005-1.384 0-.779-.394-1.363-.998-1.363l.002-.002zm5.252 3.296-.063-.442h-.022a1.314 1.314 0 0 1-1.125.53 1.118 1.118 0 0 1-1.178-1.131c0-.946.823-1.438 2.247-1.438v-.071c0-.506-.268-.76-.798-.76a1.8 1.8 0 0 0-1.004.286l-.174-.561a2.46 2.46 0 0 1 1.32-.332c1.005 0 1.511.529 1.511 1.588v1.415a5.79 5.79 0 0 0 .056.917l-.77-.001zm-.118-1.913c-.949 0-1.425.23-1.425.774a.543.543 0 0 0 .586.6.818.818 0 0 0 .841-.78l-.002-.594zm4.982 1.913-.04-.617h-.024a1.288 1.288 0 0 1-1.234.704c-.927 0-1.614-.814-1.614-1.96 0-1.201.712-2.049 1.683-2.049a1.157 1.157 0 0 1 1.084.523h.017V5.35h.856v4.57c0 .372.009.72.031 1.036h-.76zm-.126-2.259a.93.93 0 0 0-.9-.998c-.631 0-1.021.561-1.021 1.351 0 .775.402 1.305 1.003 1.305a.96.96 0 0 0 .914-1.019v-.639h.004zm6.277 2.347a1.831 1.831 0 0 1-1.85-1.975 1.87 1.87 0 0 1 1.913-2.031 1.816 1.816 0 0 1 1.852 1.968 1.88 1.88 0 0 1-1.916 2.038zm.031-3.382c-.616 0-1.011.577-1.011 1.383 0 .79.403 1.365 1.003 1.365.6 0 1.005-.616 1.005-1.383 0-.782-.394-1.366-1-1.366h.003zm6.478 3.296h-.857V8.753c0-.68-.263-1.02-.775-1.02a.888.888 0 0 0-.854.94v2.285h-.855V8.215c0-.34-.009-.704-.032-1.099h.752l.04.593h.023a1.38 1.38 0 0 1 1.218-.671c.807 0 1.338.616 1.338 1.62l.002 2.3zm5.749-3.2h-.94v1.864c0 .473.165.712.497.712.128 0 .255-.013.38-.04l.023.648c-.213.07-.438.103-.663.095-.673 0-1.076-.372-1.076-1.344V7.758h-.56v-.64h.56v-.704l.841-.254v.956h.94v.641l-.002.001zm4.52 3.2h-.853v-2.19c0-.687-.26-1.035-.775-1.035a.838.838 0 0 0-.856.909v2.315h-.851V5.355h.854v2.307h.017a1.296 1.296 0 0 1 1.156-.624c.814 0 1.312.63 1.312 1.636l-.003 2.285zm4.635-1.715H96.72a1.102 1.102 0 0 0 1.21 1.137c.353.004.704-.058 1.035-.181l.133.593a3.212 3.212 0 0 1-1.29.237 1.789 1.789 0 0 1-1.913-1.936c0-1.178.728-2.063 1.818-2.063.982 0 1.598.728 1.598 1.826.006.13-.004.26-.03.387h.003zm-.783-.609c0-.593-.3-1.011-.846-1.011a1.014 1.014 0 0 0-.934 1.011h1.78z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <clipPath id="uavr3vx5ga">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)

">%0D%0A <path d="M106.426 32.584H4.574a4.037 4.037 0 0 1-3.775-2.507 4.029 4.029 0 0 1-.3-1.564V4.09A4.028 4.028 0 0 1 3.01.318a4.038 4.038 0 0 1 1.565-.3h101.852a4.039 4.039 0 0 1 3.774 2.507c.203.496.305 1.028.3 1.564v24.424a4.032 4.032 0 0 1-4.074 4.071z" fill="%23000"/>%0D%0A <path d="M106.426.67a3.445 3.445 0 0 1 3.422 3.42v24.424a3.444 3.444 0 0 1-3.422 3.42H4.574a3.444 3.444 0 0 1-3.422-3.42V4.089A3.438 3.438 0 0 1 4.574.67h101.852zm0-.651H4.574A4.088 4.088 0 0 0 .5 4.089v24.425a4.029 4.029 0 0 0 2.508 3.771 4.039 4.039 0 0 0 1.566.3h101.852a4.04 4.04 0 0 0 2.892-1.181 4.023 4.023 0 0 0 1.182-2.89V4.089a4.082 4.082 0 0 0-4.074-4.07z" fill="%23A6A6A6"/>%0D%0A <path d="M39.122 8.323a2.216 2.216 0 0 1-.57 1.628 2.558 2.558 0 0 1-3.585 0 2.393 2.393 0 0 1-.734-1.794 2.394 2.394 0 0 1 .734-1.785 2.395 2.395 0 0 1 1.792-.736c.34.004.676.087.978.244.292.122.546.318.736.57l-.407.407a1.52 1.52 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57 1.677 1.677 0 0 0-.573 1.384 1.675 1.675 0 0 0 .57 1.384c.355.336.817.538 1.304.57a1.789 1.789 0 0 0 1.386-.57 1.347 1.347 0 0 0 .407-.976h-1.793v-.652h2.366v.326h-.003zm3.748-2.036h-2.2v1.547h2.038v.57H40.67v1.547h2.2v.651h-2.854V5.718h2.855v.57zm2.69 4.315h-.653V6.287h-1.385v-.57h3.422v.57H45.56v4.315zm3.747 0V5.718h.652v4.884h-.652zm3.423 0h-.652V6.287h-1.385v-.57h3.34v.57h-1.385v4.315h.082zm7.74-.65a2.559 2.559 0 0 1-3.585 0 2.394 2.394 0 0 1-.736-1.792 2.393 2.393 0 0 1 .736-1.791 2.558 2.558 0 0 1 3.586 0 2.395 2.395 0 0 1 .735 1.791 2.391 2.391 0 0 1-.736 1.791zm-3.096-.408c.346.35.812.554 1.304.57a1.623 1.623 0 0 0 1.304-.57c.366-.369.57-.867.57-1.387a1.675 1.675 0 0 0-.57-1.381 1.924 1.924 0 0 0-1.304-.57 1.622 1.622 0 0 0-1.304.57c-.365.367-.57.864-.57 1.381a1.676 1.676 0 0 0 .57 1.387zm4.726 1.058V5.718h.736l2.366 3.826V5.718h.651v4.884h-.657l-2.523-3.989v3.99H62.1z" fill="%23fff" stroke="%23fff" stroke-width=".2" stroke-miterlimit="10"/>%0D%0A <path d="M55.989 17.767a3.43 3.43 0 0 0-3.258 2.149c-.173.43-.256.89-.246 1.352a3.47 3.47 0 0 0 2.159 3.241c.427.175.884.263 1.345.26a3.432 3.432 0 0 0 3.258-2.15c.172-.429.256-.889.245-1.351a3.376 3.376 0 0 0-3.503-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-7.578-5.536a3.431 3.431 0 0 0-3.258 2.149c-.172.43-.256.89-.246 1.352a3.472 3.472 0 0 0 2.16 3.241c.426.175.883.263 1.344.26a3.432 3.432 0 0 0 3.258-2.15c.173-.429.256-.889.246-1.351a3.376 3.376 0 0 0-3.504-3.501zm0 5.536a2.024 2.024 0 0 1-1.956-2.117 2.018 2.018 0 0 1 1.956-2.116 1.976 1.976 0 0 1 1.85 1.322c.09.254.125.525.105.794a2.019 2.019 0 0 1-1.955 2.117zm-9.044-4.478v1.466h3.503a3.077 3.077 0 0 1-.815 1.872 3.607 3.607 0 0 1-2.688 1.059 3.796 3.796 0 0 1-3.83-3.908 3.838 3.838 0 0 1 2.347-3.605c.47-.198.973-.301 1.483-.303a4.041 4.041 0 0 1 2.688 1.056l1.06-1.056a5.223 5.223 0 0 0-3.667-1.466 5.49 5.49 0 0 0-5.46 5.373 5.49 5.49 0 0 0 5.46 5.374 4.693 4.693 0 0 0 3.748-1.547 4.9 4.9 0 0 0 1.304-3.42c.017-.3-.01-.6-.082-.892h-5.051v-.003zm36.992 1.14a3.163 3.163 0 0 0-2.933-2.198c-1.793 0-3.26 1.384-3.26 3.5a3.406 3.406 0 0 0 3.423 3.502 3.345 3.345 0 0 0 2.852-1.547l-1.141-.814a1.986 1.986 0 0 1-1.711.976 1.769 1.769 0 0 1-1.711-1.058l4.644-1.954-.163-.407zm-4.726 1.14a1.977 1.977 0 0 1 1.793-2.035 1.441 1.441 0 0 1 1.303.732l-3.096 1.303zm-3.83 3.34h1.549V14.267h-1.548v10.18zm-2.444-5.943a2.682 2.682 0 0 0-1.874-.814 3.502 3.502 0 0 0-3.34 3.501 3.369 3.369 0 0 0 2.048 3.149c.409.174.848.266 1.292.27a2.34 2.34 0 0 0 1.793-.814h.081v.489c0 1.302-.736 2.035-1.874 2.035a1.81 1.81 0 0 1-1.711-1.221l-1.304.57a3.36 3.36 0 0 0 3.096 2.035c1.793 0 3.26-1.058 3.26-3.582v-6.19h-1.467v.572zm-1.792 4.804a2.025 2.025 0 0 1-1.956-2.117 2.02 2.02 0 0 1 1.956-2.117 1.961 1.961 0 0 1 1.874 2.117 1.957 1.957 0 0 1-1.875 2.114v.003zm19.881-9.035h-3.667v10.175h1.548v-3.83h2.119a3.185 3.185 0 0 0 3.087-1.92 3.177 3.177 0 0 0-1.82-4.237 3.185 3.185 0 0 0-1.267-.193v.005zm.082 4.885h-2.2V15.65h2.2a1.788 1.788 0 0 1 1.792 1.71 1.862 1.862 0 0 1-1.793 1.791v.005zm9.37-1.465c-1.14 0-2.282.488-2.689 1.547l1.385.57a1.438 1.438 0 0 1 1.385-.736 1.532 1.532 0 0 1 1.63 1.303v.079a3.236 3.236 0 0 0-1.548-.407c-1.467 0-2.934.814-2.934 2.28a2.386 2.386 0 0 0 2.524 2.279 2.294 2.294 0 0 0 1.955-.977h.082v.817h1.466v-3.908a3.08 3.08 0 0 0-3.259-2.85l.003.003zm-.163 5.617c-.489 0-1.222-.244-1.222-.893 0-.814.896-1.058 1.63-1.058.48.002.954.113 1.385.326a1.895 1.895 0 0 1-1.793 1.62v.005zm8.555-5.373-1.71 4.396H99.5l-1.793-4.396h-1.63l2.69 6.188-1.549 3.419h1.548l4.153-9.607h-1.629.002zm-13.688 6.51h1.548V14.267h-1.548v10.18z" fill="%23fff"/>%0D%0A <path d="M8.974 6.125a1.59 1.59 0 0 0-.326 1.14v17.992a1.61 1.61 0 0 0 .408 1.14l.081.081 10.104-10.095v-.163L8.974 6.125z" fill="url(%23nqixmws78b)"/>%0D%0A <path d="m22.5 19.802-3.34-3.338v-.244l3.34-3.338.081.082 3.99 2.28c1.141.65 1.141 1.709 0 2.36L22.5 19.802z" fill="url(%23euwe5vohvc)"/>%0D%0A <path d="m22.581 19.72-3.422-3.418L8.974 26.477c.408.407.978.407 1.711.082l11.896-6.84z" fill="url(%23wso0uh08dd)"/>%0D%0A <path d="M22.581 12.882 10.685 6.125c-.736-.407-1.303-.326-1.71.081l10.184 10.096 3.422-3.42z" fill="url(%23mrdt54dj1e)"/>%0D%0A <path opacity=".2" d="m22.5 19.64-11.815 6.675a1.334 1.334 0 0 1-1.63 0l-.08.082.08.081a1.333 1.333 0 0 0 1.63 0L22.5 19.64z" fill="%23000"/>%0D%0A <path opacity=".12" d="M8.974 26.316a1.59 1.59 0 0 1-.326-1.14v.081a1.61 1.61 0 0 0 .408 1.14v-.081h-.082zm17.6-8.956L22.5 19.64l.081.08 3.993-2.279a1.355 1.355 0 0 0 .815-1.14c0 .408-.326.733-.815 1.059z" fill="%23000"/>%0D%0A <path opacity=".25" d="m10.685 6.206 15.89 9.037c.488.326.814.651.814 1.059a1.352 1.352 0 0 0-.815-1.14L10.685 6.125c-1.143-.652-2.037-.163-2.037 1.14v.08c0-1.22.894-1.79 2.037-1.139z" fill="%23fff"/>%0D%0A </g>%0D%0A <defs>%0D%0A <linearGradient id="nqixmws78b" x1="18.265" y1="27.13" x2="2.062" y2="22.737" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2300A0FF"/>%0D%0A <stop offset=".007" stop-color="%2300A1FF"/>%0D%0A <stop offset=".26" stop-color="%2300BEFF"/>%0D%0A <stop offset=".512" stop-color="%2300D2FF"/>%0D%0A <stop offset=".76" stop-color="%2300DFFF"/>%0D%0A <stop offset="1" stop-color="%2300E3FF"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="euwe5vohvc" x1="28.064" y1="17.927" x2="8.353" y2="17.927" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FFE000"/>%0D%0A <stop offset=".409" stop-color="%23FFBD00"/>%0D%0A <stop offset=".775" stop-color="orange"/>%0D%0A <stop offset="1" stop-color="%23FF9C00"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="wso0uh08dd" x1="20.731" y1="16.06" x2="7.736" y2="-5.775" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%23FF3A44"/>%0D%0A <stop offset="1" stop-color="%23C31162"/>%0D%0A </linearGradient>%0D%0A <linearGradient id="mrdt54dj1e" x1="6.443" y1="34.068" x2="12.205" y2="24.305" gradientUnits="userSpaceOnUse">%0D%0A <stop stop-color="%2332A071"/>%0D%0A <stop offset=".069" stop-color="%232DA771"/>%0D%0A <stop offset=".476" stop-color="%2315CF74"/>%0D%0A <stop offset=".801" stop-color="%2306E775"/>%0D%0A <stop offset="1" stop-color="%2300F076"/>%0D%0A </linearGradient>%0D%0A <clipPath id="oefv1zwvza">%0D%0A <path fill="%23fff" transform="translate(.5 .019)" d="M0 0h110v32.566H0z"/>%0D%0A </clipPath>%0D%0A </defs>%0D%0A</svg>%0D%0A)