Hurtiglenker

Korea CPI Hits 26-Month High at 3.1%: BOK Rate Hike Risk Pressures KRW, KOSPI, and Global Chip Stocks

Datasnapshot

Viktige punkter

- •South Korea CPI surged to 3.1% YoY in May (highest since March 2024), driven by transport (+11.6% YoY) and fuel prices tied to Middle East tensions — per Reuters.

- •BOK July rate hike is now the base case; this is KRW-supportive medium-term but introduces hard volatility event risk for leveraged KRW and KOSPI CFD positions.

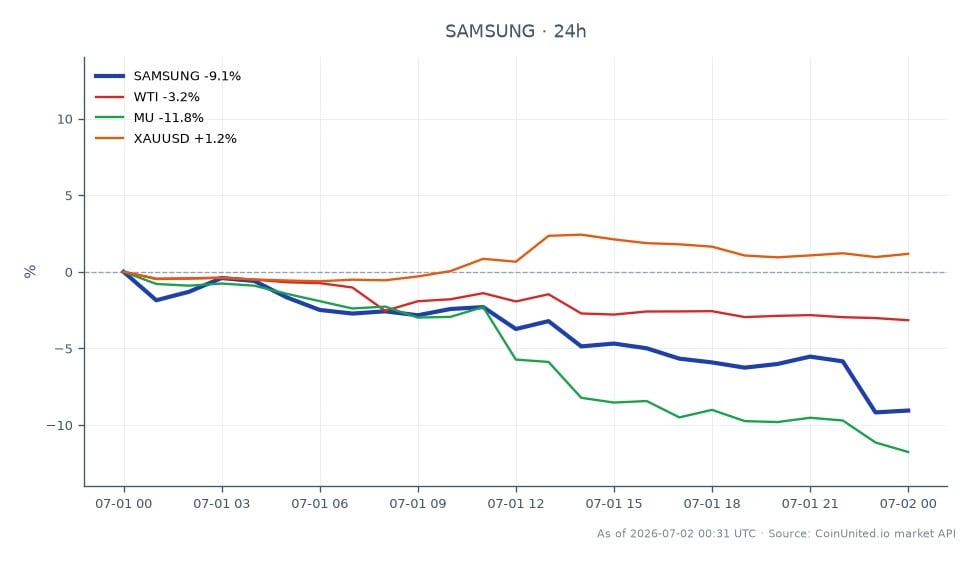

- •Samsung is down 12.67% on the session ($189.38); a 50x long opened at the $197 session high is fully liquidated — high-leverage entries near session lows carry mean-reversion upside but BOK risk remains.

- •Cross-market rotation thesis: Korean semi weakness may drive capital into US-listed peers (MU, NVDA) and the SOX index — monitor relative performance for confirmation.

- •Oil-driven inflation creates a dual exposure: WTI strength sustains BOK hawkishness while also supporting gold as an APAC inflation hedge.

According to Reuters, South Korea's headline CPI accelerated to 3.1% YoY in May 2026, up sharply from 2.6% in April and above the 3.0% consensus — the highest reading since March 2024. Core CPI (ex fo

Event Summary

According to Reuters, South Korea's headline CPI accelerated to 3.1% YoY in May 2026, up sharply from 2.6% in April and above the 3.0% consensus — the highest reading since March 2024. Core CPI (ex food and energy) rose to 2.5% YoY from 2.2%, its fastest pace since February 2024. On a monthly basis, CPI rose 0.5% MoM, double the 0.3% consensus.

As reported by ING and Reuters, the primary drivers were transport inflation surging to 11.6% YoY (fuel prices up 23–33% depending on product), food prices at +1.6% YoY, and housing/utilities at +1.8% YoY — all tied to higher oil prices linked to Middle East tensions and a weaker Korean won. The Bank of Korea (BOK) has revised its annual inflation forecast up from 2.2% to 2.7%, with market participants now pricing a rate hike at the July BOK meeting. This is a core APAC hawkish pivot and inflation surge signal with direct macro inflation pressure implications across multiple asset classes.

Leverage Impact Analysis

USD/KRW (Forex CFD): A hawkish BOK pivot is structurally KRW-supportive via improved carry, but near-term USD/KRW remains volatile. A trader holding a 100x long USD/KRW CFD faces acute liquidation risk if the BOK surprises with an early or outsized hike — even a 0.5% KRW strengthening move could erase a 50x position's margin buffer entirely. Conversely, if oil prices continue rising (the primary inflation driver), import-cost pressure could keep KRW weak and sustain the USD/KRW long.

Samsung Electronics (Stock CFD): Samsung is trading at $189.38, down 12.67% on the session (24h high: $197.01, low: $187.11). A trader with a 50x long Samsung CFD opened at $197.01 (session high) is now sitting on a ~6.4% adverse move — representing ~320% loss relative to their margin at 50x, a full liquidation scenario. High-leverage shorts opened near $197 are significantly in profit but face mean-reversion risk ahead of the July BOK meeting. Monitor the semiconductor supply chain geopolitics theme for further catalysts.

For leveraged KOSPI200 index CFD traders, rate-hike expectations compress domestic-demand multiples. Position sizing must account for BOK meeting date risk (July) as a hard volatility event.

Cross-Market Impact

Semiconductors — Global Spillover: Korea's chip heavyweights (Samsung and SK Hynix) are critical nodes in the global memory supply chain. Sell-side outflow warnings — directionally consistent with macro conditions — could trigger rotation from Korean semis into US peers. Watch the PHLX Semiconductor Index (SOX) for relative strength signals; if Korean semis underperform while SOX holds, it signals capital rotation rather than sector-wide de-risking. Micron Technology (MU) and NVIDIA could see marginal bid as reallocation destinations.

Oil/WTI: The inflation spike is explicitly oil-driven (Middle East tensions). Sustained WTI strength above current levels directly feeds Korean import costs, creating a feedback loop that keeps BOK hawkish longer than the base case. Review the Iran conflict and APAC stagflation framework for persistence risk.

Gold: Inflation-driven risk-off in APAC historically supports gold as a regional safe haven. If BOK tightening compresses Korean growth expectations, inflation-hedge asset rotation into gold CFDs becomes structurally attractive.

USD/JPY: A hawkish BOK adds modest pressure on regional carry trades. With BOJ also navigating inflation, watch USD/JPY for correlated moves — both central banks tightening simultaneously could reinforce yen strength and pressure the broader Asia carry complex.

Trading Considerations

Key levels: Samsung support sits near the $187.11 session low; a break below opens a void toward prior structural support. The July BOK meeting is the next hard catalyst — any forward guidance or intermeeting communication resets KRW and KOSPI positioning entirely. For macro inflation trading strategy context, traders should monitor monthly CPI prints and BOK statements for confirmation that the July hike is fully priced.

Risk factors include oil price trajectory (primary inflation driver), won depreciation pace, and whether foreign institutional outflows from Korean equities accelerate into a self-reinforcing cycle. Check live funding rates and open interest on CoinUnited.io for KRW and Samsung CFD positioning signals before sizing new entries.

Trade Samsung Electronics Co Ltd on CoinUnited.io

Trade SAMSUNG with up to 1000xx leverage → | Create Free Account

Ofte stilte spørsmål

A confirmed July BOK hike would strengthen KRW, meaning USD/KRW shorts become attractive but USD/KRW longs face rapid adverse moves — at 100x leverage, even a 0.5% KRW appreciation can trigger liquidation. Size positions conservatively ahead of the July meeting date.

Fortsett Utforskningen

Ansvarsfraskrivelse: Denne briefen er kun for utdanningsformål og er ikke investeringsråd.