빠른 링크

Qifu Technology (QFIN) Posts $1.12 Non-GAAP EPADS, $566.7M Revenue — Q2 Outlook Points to 24–31% Profit Growth

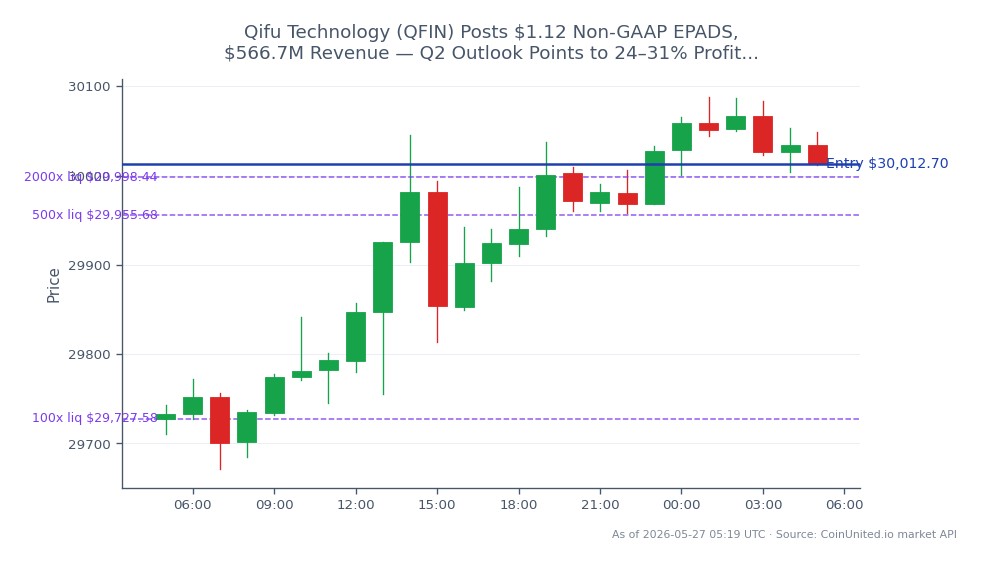

데이터 스냅샷

주요 요점

- •QFIN reported non-GAAP EPADS of $1.12 and revenue of $566.7M, with Q2 2025 net income guidance of RMB 1.75B–1.85B implying 24–31% YoY growth.

- •Take rate expansion to ~5.4% (+~1ppt YoY) and capital-light model shift signal improving earnings quality, not just volume growth.

- •Sustained delivery against guidance challenges the elevated regulatory risk premium historically baked into China fintech ADR valuations.

- •Loan facilitation volumes of ~RMB 84.6B in Q2 2025 (+16% YoY) indicate resilient Chinese consumer credit demand despite macro headwinds.

- •Primary trade is directional on QFIN; secondary read-through supports China ADR sentiment and marginally informs USD/CNY and EM risk narratives.

Qifu Technology Inc. (NASDAQ: QFIN), China's leading credit-tech platform formerly known as Qfin Holdings, reported non-GAAP earnings per ADS of $1.12 alongside revenue of $566.7M, accompanied by forw

Event Analysis

Qifu Technology Inc. (NASDAQ: QFIN), China's leading credit-tech platform formerly known as Qfin Holdings, reported non-GAAP earnings per ADS of $1.12 alongside revenue of $566.7M, accompanied by forward Q2 2025 guidance for non-GAAP net income in the range of RMB 1.75B–1.85B — implying approximately 24–31% year-over-year growth, according to earnings call coverage aggregated by Capyfin and AlphaSpread. These figures are consistent with Qifu's established earnings trajectory, which saw Q1 2025 revenue reach ~$646.4M and Q2 2025 loan facilitation volumes hit ~RMB 84.6B, up 16% YoY.

What distinguishes this print from prior quarters is the combination of margin resilience and volume durability against a backdrop of persistent macro headwinds in China. The company's take rate expanded to approximately 5.4% — nearly 1 percentage point higher YoY — a sign that Qifu is capturing more value per loan facilitated, not just growing volumes. Its ongoing shift toward capital-light loan facilitation further improves earnings quality, reducing balance-sheet risk and supporting higher return-on-equity metrics that institutional investors reward with premium multiples.

Critically, Qifu's outperformance challenges the prevailing bear thesis on China consumer credit. Regulatory overhang has suppressed valuations of Chinese fintech ADRs for years; sustained delivery against guidance — especially in a sector once targeted by Beijing's platform crackdowns — signals that the regulatory risk premium embedded in QFIN's valuation may be excessive. As highlighted in coverage by Insider Monkey and Intellectia AI, this is part of a broader pattern: QFIN has now delivered double-digit YoY profit growth across multiple consecutive quarters, making this less a one-off beat and more a structural re-rating catalyst.

For traders watching the diversified sector earnings beat wave, QFIN joins a cohort of non-US financial names demonstrating that earnings resilience is not purely a US phenomenon. The financials & industrials earnings beat theme is gaining breadth, and QFIN's results add a meaningful China fintech data point to that narrative.

What This Means for Traders

The primary trade is directional on QFIN equity. Whether $1.12 EPADS and $566.7M revenue constitute a true beat depends on where sell-side consensus was set — that comparison is the immediate price driver. If guidance at RMB 1.75B–1.85B tracks toward the upper end and management commentary is constructive on credit quality and regulation, the setup favors a re-rating toward higher forward P/E multiples. Traders should monitor the earnings call tone closely: any caution on non-performing loans or regulatory signals would limit upside even on a headline beat. For context on how to structure around this setup, the earnings beat sector playbooks guide covers entry timing and position sizing in post-earnings environments.

Beyond QFIN itself, the results offer a read-through for other US-listed Chinese consumer finance names and China ADR sentiment broadly. Strong loan volumes in Chinese consumer credit — despite macro uncertainty — marginally supports the China growth resilience narrative, which feeds into USD/CNY dynamics and EM risk appetite. The effect on broad indices like the NASDAQ 100 or S&P 500 is negligible given QFIN's market cap, but sector ETF traders and China ADR basket traders should take note.

Volatility is likely elevated around the earnings release window. Post-earnings implied volatility crush is typical; traders who entered volatility positions pre-announcement should manage IV exposure carefully. For those eyeing directional QFIN trades, CoinUnited's stock CFDs trade 24/7 — meaning you can position on this earnings event immediately, without waiting for the next NASDAQ session to open.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

자주 묻는 질문

The research confirms $1.12 non-GAAP EPADS is consistent with QFIN's recent earnings trajectory, but the precise beat/miss magnitude requires comparison to sell-side consensus estimates not provided in available data. Check real-time consensus on platforms like Bloomberg or FactSet before trading.

계속 탐색하기

면책 조항: 이 브리프는 교육 목적으로만 사용되며 투자 조언이 아닙니다.