Quick Links

Alibaba's $1.5B Bid for Grocer Pupu Signals Renewed China Tech M&A Aggression

Data Snapshot

Key Takeaways

- •Alibaba has offered ~$1.5B for Chinese grocery platform Pupu, per Bloomberg — more than 2x a rival bid from Sun Art, signaling high strategic conviction.

- •The deal targets the high-frequency instant grocery vertical, strengthening Alibaba's position against Meituan and JD.com in local on-demand commerce.

- •Management's willingness to pursue large-scale M&A is a meaningful regulatory signal — China's antitrust climate appears more accommodating for platform deals.

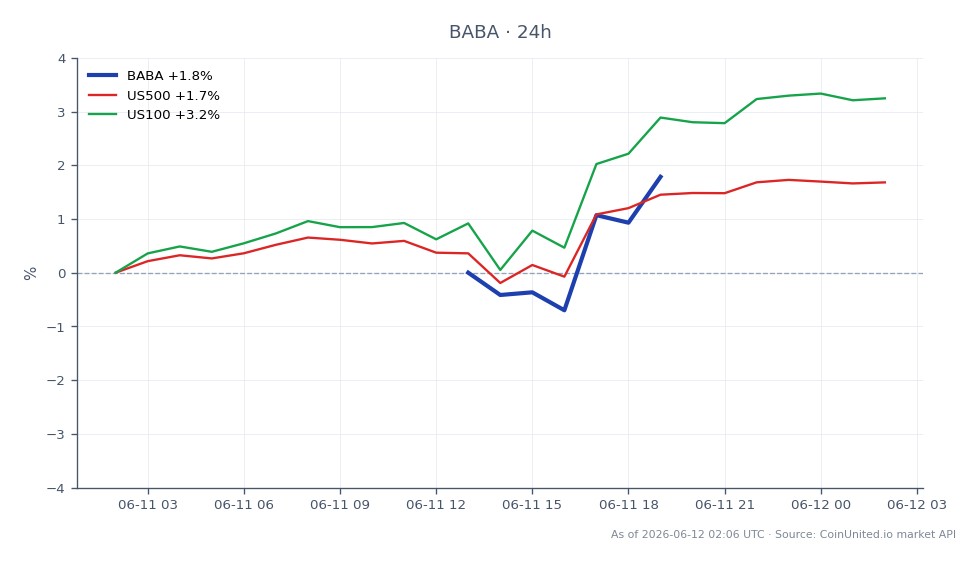

- •BABA is trading at $112.68 (down 2.57%), with the market weighing growth upside against margin dilution risk from subsidy-heavy grocery operations.

- •Peer read-through is negative for Meituan and potentially JD.com; China tech indices may reprice as the M&A wave broadens.

As reported by Bloomberg, Alibaba Group has offered approximately $1.5 billion to acquire Pupu, a Chinese grocery delivery platform. According to reporting via Investing.com summarizing Bloomberg, Ali

Event Analysis

As reported by Bloomberg, Alibaba Group has offered approximately $1.5 billion to acquire Pupu, a Chinese grocery delivery platform. According to reporting via Investing.com summarizing Bloomberg, Alibaba's bid is more than double a rival offer from Sun Art — a notable detail given Sun Art's own close ties to Alibaba's extended retail ecosystem. The deal remains a proposal rather than a closed transaction, meaning regulatory and structural deal risk still applies.

The strategic logic is clear: Pupu operates in the online grocery and instant delivery space, a high-frequency battleground where Alibaba competes directly against Meituan and JD.com. Integrating Pupu would deepen Alibaba's local on-demand commerce capability and bolster its "New Retail" vision — the long-running push to blend digital and physical retail experiences under one ecosystem. The $1.5B price tag is material at the business-unit level but manageable given Alibaba's balance sheet.

Perhaps more significant than the deal itself is what it signals about China's regulatory climate. Large platform M&A in community group buying and online grocery was previously a flashpoint for antitrust scrutiny. Alibaba's willingness to table a sizable acquisition — outbidding a rival by more than 2x — suggests management reads the current regulatory environment as meaningfully more accommodating. This read-through matters for China tech M&A broadly, not just Alibaba. As part of the broader cross-sector acquisition repricing wave, this deal may encourage peers to pursue deals they previously shelved.

What This Means for Traders

For BABA equity and CFD traders, this is a two-sided event. The bullish case: Pupu integration accelerates GMV growth in local services and increases user transaction frequency, supporting the growth re-acceleration narrative that drove BABA's strong Q4 earnings (AI cloud +38%). The bearish friction: grocery delivery is structurally margin-dilutive, requiring ongoing subsidy spend and heavy logistics investment — a concern for investors already watching Alibaba's capital allocation closely. According to live market data, BABA is trading at $112.68, down 2.57% on the day, with a 24-hour range of $109.66–$112.82, suggesting the market's initial reaction leans cautious.

Peer implications are worth watching. A stronger Alibaba in instant grocery delivery is incrementally negative for Meituan's market share narrative, and may pressure JD.com to accelerate its own fresh food investments. For traders using the mergers and acquisitions trading framework, a long BABA / short Meituan relative value trade is one way to express conviction on competitive share shifts without taking a pure directional bet. China internet ETFs and Hang Seng Index products with large Alibaba weightings may also see beta-amplified moves if regulatory approval headlines emerge.

Trade Alibaba Group Holdings Ltd. on CoinUnited.io

Trade BABA with up to 500xx leverage → | Create Free Account

Frequently Asked Questions

No. As of current reporting, this is a Bloomberg-reported proposal. Treat it as high-credibility but unconfirmed — deal terms could change or face regulatory review before closing.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.