Quick Links

Aave Proposes Stricter Asset Listing Framework After KelpDAO rsETH Exploit Creates Up to $230M in Bad Debt

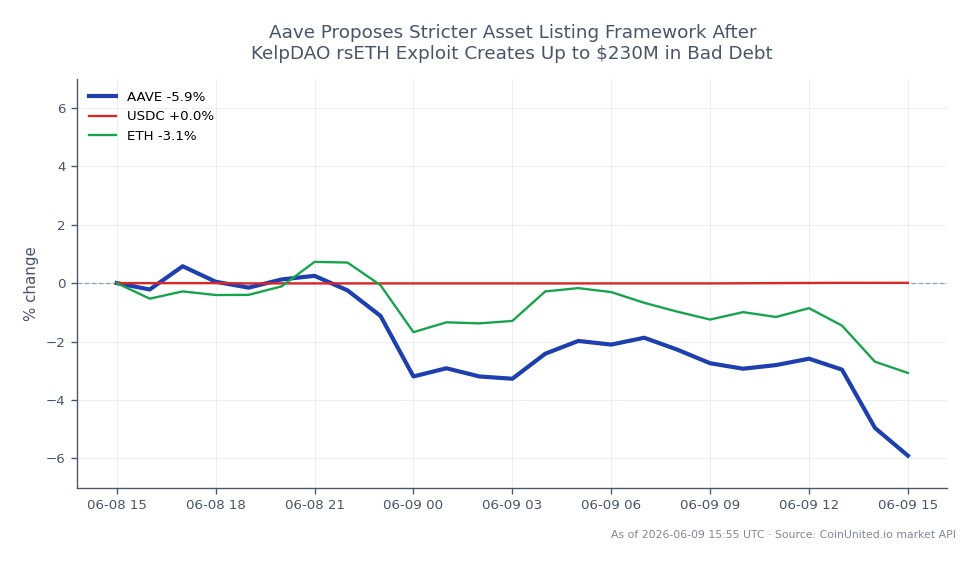

Data Snapshot

Key Takeaways

- •Galaxy Research estimates Aave's bad debt at $123.7M–$230.1M depending on how losses are socialized — final governance decision is the key AAVE price catalyst.

- •The exploit originated from a 1-of-1 DVN misconfiguration on KelpDAO's LayerZero V2 bridge — Aave's own smart contracts were not compromised.

- •Aave's proposed listing framework adds bridge security, oracle design, and interoperability risk checks — tightening collateral standards across the ecosystem.

- •AAVE is trading at $60.37, down 6.49% on the session, with Safety Module activation risk creating persistent near-term selling pressure.

- •The event reinforces the DeFi structural reset thesis: non-protocol infrastructure failures can still generate protocol-level insolvency, making cross-chain risk assessment essential for any leveraged DeFi position.

On April 18, 2026, the KelpDAO rsETH bridge was exploited via a compromised LayerZero V2 Unichain-to-Ethereum route configured as a single-verifier (1-of-1 DVN) — a critical single point of failure in

Event Analysis

On April 18, 2026, the KelpDAO rsETH bridge was exploited via a compromised LayerZero V2 Unichain-to-Ethereum route configured as a single-verifier (1-of-1 DVN) — a critical single point of failure in cross-chain message verification. According to the Aave governance forum, the attacker released 116,500 rsETH from the Ethereum-side adapter and dispersed funds across multiple wallets. Aave froze rsETH and wrsETH reserves, setting loan-to-value to zero within hours — a decisive but costly response.

As reported by Galaxy Research, the stolen rsETH was deployed as collateral across Aave, Compound, and Euler, enabling approximately $236 million in WETH and wstETH borrowings. Galaxy estimates Aave's resulting bad debt at $123.7 million under uniform socialization or $230.1 million if losses are isolated to L2 rsETH positions. This is a textbook case of collateral contagion: a bridge failure outside Aave's own smart contracts still created protocol-level insolvency risk — a structural vulnerability the DeFi structural reset theme has been tracking.

Aave's governance response goes beyond damage control. The newly proposed listing framework adds security and infrastructure checks including bridge security, oracle dependencies, validator decentralization, interoperability risk, cross-protocol contagion exposure, and incident-response readiness. For the Aave DeFi lending ecosystem, this represents a meaningful shift from purely financial underwriting to operational risk assessment. It is a direct acknowledgment that DeFi collateral risk cannot be evaluated in isolation from the infrastructure layers beneath it. Understanding how DeFi bad debt is resolved is now essential context for any lending protocol participant.

What makes this event structurally significant — beyond the immediate dollar figures — is that it validates long-standing concerns about cross-chain infrastructure fragility. A single misconfigured DVN parameter was sufficient to generate nine-figure bad debt across multiple leading lending protocols simultaneously.

What This Means for Traders

Aave (AAVE) is trading at $60.37, down 6.49% over 24 hours with a session low of $60.22, reflecting active selling pressure tied to this event. The bad-debt range ($123.7M–$230.1M) remains a live uncertainty — the final socialization method will determine how much of that cost falls on AAVE stakers via the Safety Module. Until governance resolves this, AAVE faces persistent headline risk and suppressed sentiment, consistent with the DeFi reset risks environment of 2026.

For Ethereum and wstETH, the transmission channel is indirect but real: forced liquidations of borrowed WETH/wstETH positions created selling pressure during the unwind phase. The broader DeFi lending sector — including Compound (COMP) and Euler — carries residual contagion risk given their parallel exposure to the same attacker collateral. Restaking and liquid restaking tokens more broadly may face a repricing of collateral quality premiums, as the market reassesses bridge-linked assets.

The proposed framework itself is medium-term constructive for AAVE if adopted: tighter collateral standards reduce future tail risk and could restore institutional confidence. Traders watching for a sentiment reversal should monitor governance votes on the new framework and the final bad-debt socialization decision as the two key catalysts.

FAQ

Q: Will AAVE stakers absorb the bad debt through the Safety Module? A: Potentially. The Safety Module exists precisely for this scenario, but governance must vote on whether to activate it and how losses are distributed — this decision is the key near-term price catalyst for AAVE.

Q: Is Aave's core smart contract compromised? A: No. According to the Aave governance forum, the exploit was an external event originating from KelpDAO's bridge infrastructure, not a failure of Aave's own contracts.

Q: How does the new listing framework change things for future collateral assets? A: Future assets seeking Aave listing will face checks on bridge security, oracle design, and interoperability risk — not just financial metrics. Assets with weak bridge architectures or single-verifier setups may be excluded or face lower LTV caps.

Q: With AAVE down ~6.5%, is this a leverage entry opportunity or a falling knife? A: The bad-debt range ($123.7M–$230.1M) is still unresolved, meaning downside risk persists until governance confirms the socialization method. Confirmation of a bounded loss figure would be the cleaner entry signal.

Q: Does this affect USDC or stablecoin liquidity on Aave? A: The exploit targeted ETH-denominated collateral, not stablecoins directly. However, large-scale bad debt events can reduce depositor confidence across all asset classes on affected protocols — monitor USDC utilization rates on Aave for any anomalies.

Trade Aave on CoinUnited.io

Trade AAVE with up to 2000xx leverage → | Create Free Account

Frequently Asked Questions

Potentially. The Safety Module exists precisely for this scenario, but governance must vote on activation and loss distribution — this is the key near-term price catalyst for AAVE.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.