Quick Links

Indonesia Coal Export Crackdown: Leverage Scenarios and Cross-Market Ripple Effects

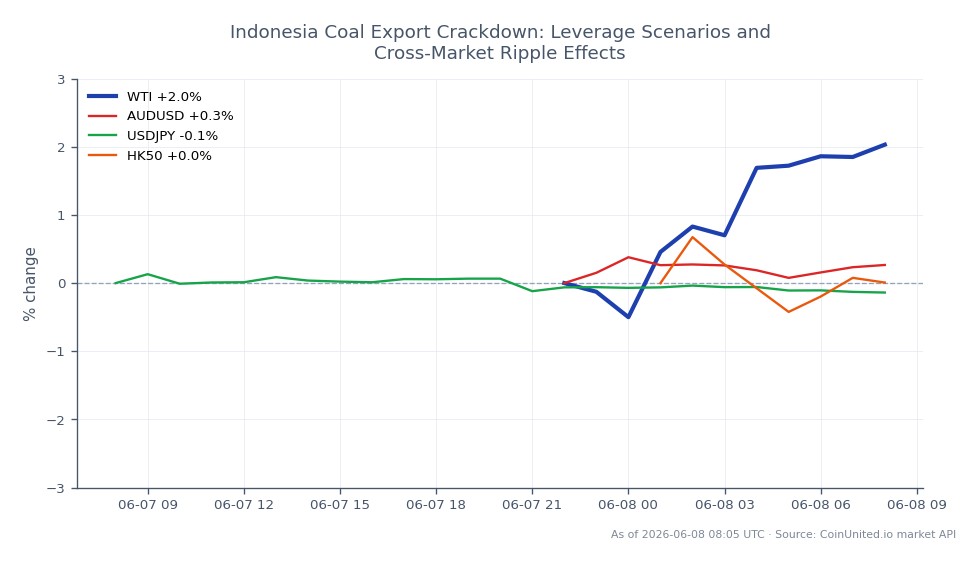

Data Snapshot

Key Takeaways

- •Indonesia controls ~40% of seaborne thermal coal; DMO enforcement and the new Danantara export channel create discrete policy catalysts capable of sharp price spikes — high leverage coal CFD positions should carry wide margin buffers.

- •A 50x long coal CFD amplifies a 5% policy-driven price move to 250% gain/loss on margin — funding rates and open interest should be monitored on CoinUnited.io before sizing positions.

- •AUD/USD is a cross-market beneficiary: Australian coal exporters gain volume and pricing power when Indonesian supply is constrained, making AUD a macro proxy for this trade.

- •JPY faces headwinds as Japan's coal import bill rises, complicating BOJ rate normalization — watch USD/JPY for further yen softness tied to energy cost deterioration.

- •Hang Seng-listed industrials and Chinese utilities face margin pressure from higher seaborne coal costs, adding to APAC stagflation risk.

Indonesia — the world's largest thermal coal exporter, accounting for roughly 40% of seaborne thermal coal trade — is tightening its grip on coal exports through a combination of stricter Domestic Mar

Event Summary

Indonesia — the world's largest thermal coal exporter, accounting for roughly 40% of seaborne thermal coal trade — is tightening its grip on coal exports through a combination of stricter Domestic Market Obligation (DMO) enforcement, export permit linkage, and a new state-agency export channel. According to research sourced from Indonesian regulatory filings and energy market analysis, miners must sell at least 25% of approved production domestically at a regulated cap of US$70/ton, well below international Newcastle benchmarks. The government has announced plans to route all coal exports through a state agency under sovereign wealth fund Danantara, with coal designated in the first wave alongside palm oil and ferroalloys, subject to a three-month transition period.

Historical precedent is clear: past Indonesian export restrictions triggered sharp seaborne coal price spikes. With Indonesia exporting approximately 400 million tons in 2020 — nearly half to China — any supply disruption sends an outsized signal to Asian energy markets and feeds directly into the macro inflation pressure theme already weighing on regional economies.

Leverage Impact Analysis

For leveraged commodity CFD traders on CoinUnited.io, Indonesian coal policy creates a high-volatility, policy-driven environment with asymmetric spike risk — ideal for tactical positions but dangerous for unhedged exposure.

Worked example — Long Coal CFD: A trader entering a 50x long Coal CFD position at a hypothetical entry near current spot levels faces amplified sensitivity to each policy headline. A 5% price move — well within the range seen during past Indonesian export disruptions — translates to a 250% gain or loss on margin. Given that DMO tightening, permit suspensions, or implementation friction in the new Danantara channel can move prices by double digits in short windows, position sizing is critical. Traders should monitor real-time funding rates on CoinUnited.io and keep margin buffers wide.

Short-side liquidation risk: Any trader short coal CFDs with leverage above 20x faces acute liquidation risk if a sudden export-permit suspension or DMO quota increase is announced. The policy-driven nature of this event means gaps can occur with little warning — unlike demand-side moves that build gradually. Check open interest for positioning signals before sizing short exposure.

Funding rate watch: Supply-shock narratives in commodities tend to attract speculative longs, which can push funding rates higher on perpetual-style instruments. Monitor this on CoinUnited.io for cost-of-carry implications on multi-day positions.

Cross-Market Impact

WTI Light Crude Oil: Coal price spikes in Asia create second-order oil demand uplift as utilities and industrials reassess fuel mix economics. This is a secondary effect but relevant for energy basket traders.

Australian Dollar / US Dollar: Australia is a direct beneficiary when Indonesian coal supply tightens — Australian producers gain both volume and pricing power as Asian buyers substitute supply sources. Our AUD/USD Trading Guide outlines how commodity-price dynamics drive this pair; a sustained Indonesian supply squeeze is structurally AUD-positive.

US Dollar / Japanese Yen: Japan is a major coal importer. Rising energy import costs worsen Japan's trade balance, adding yen depreciation pressure and complicating the Bank of Japan's rate normalization path — a dynamic covered in depth in our USD/JPY trading guide.

Hang Seng Index: China absorbs close to half of Indonesian coal exports. Higher seaborne coal costs feed into Chinese power and industrial input prices, pressuring margins for energy-intensive HK-listed industrials. Traders can reference our Hang Seng Index guide for sector-level exposure mapping. This event also amplifies APAC stagflation and currency stress risks across the region.

Trading Considerations

Key triggers to watch: any announced increase to the DMO domestic allocation share (currently 25%), export-permit suspension announcements for non-compliant miners, and operational delays in standing up the Danantara export channel. Each of these can function as a discrete, tradeable catalyst rather than a gradual reprice. The spread between the US$70/ton DMO cap and elevated Newcastle benchmarks is the core tension — the wider that gap, the stronger the regulatory pressure and the more abrupt the potential policy response.

Risk factors include partial implementation (bureaucratic delays reducing actual supply impact), demand softness from a slowing Chinese economy offsetting supply tightness, and LNG price normalization reducing coal substitution demand. Volatility windows around Indonesian policy announcements warrant reduced leverage or tighter stops.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

A sudden permit suspension is a discrete policy shock — prices can gap up sharply before traders can exit. At 50x leverage, even a 3-5% gap move can wipe margin; keep position sizes small and stops active around known policy announcement windows.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.