Quick Links

Howard Hughes Holdings Closes $2.1B Vantage Deal — A Berkshire-Style Pivot That Reprices HHH

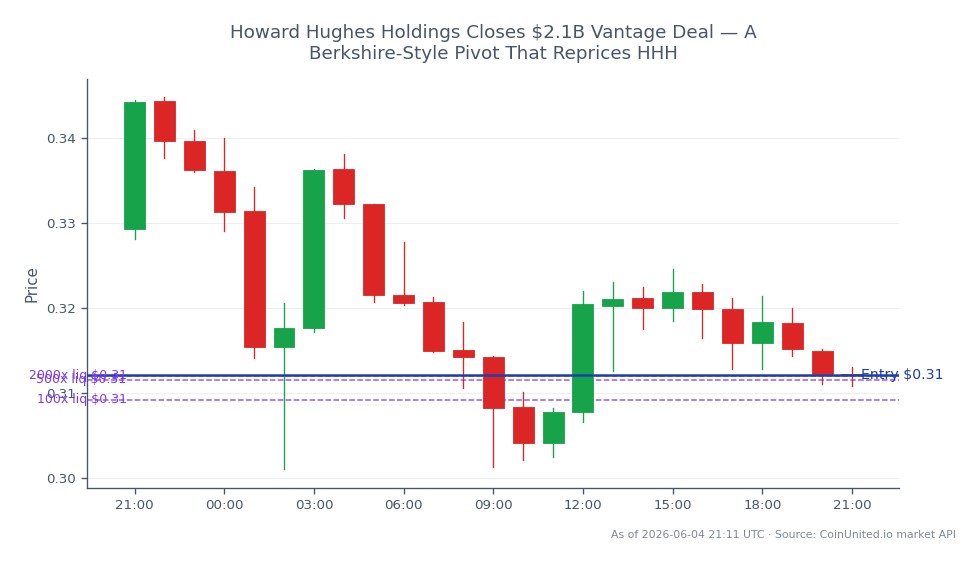

Data Snapshot

Key Takeaways

- •HHH is acquiring Vantage Group Holdings for $2.1B cash, pivoting from real estate development to a diversified holding-company/insurance model.

- •Pershing Square is providing up to $1.0B in preferred stock financing and will manage Vantage's investment portfolio post-close.

- •Deal priced at ~1.5x Vantage's estimated 2025 year-end book value — a premium that sets a sector comparable for specialty reinsurer M&A.

- •AM Best placed Vantage under review with developing implications, introducing credit/rating risk as a key watchpoint.

- •Closing expected Q2 2026 with a December 2026 long-stop — regulatory approval timeline is the primary event-driven catalyst.

Howard Hughes Holdings (NYSE: HHH) has agreed to acquire Vantage Group Holdings, a specialty insurer and reinsurer, for $2.1 billion in cash — a transaction that fundamentally redefines what HHH is. A

Event Analysis

Howard Hughes Holdings (NYSE: HHH) has agreed to acquire Vantage Group Holdings, a specialty insurer and reinsurer, for $2.1 billion in cash — a transaction that fundamentally redefines what HHH is. As reported by *Insurance Journal* and confirmed via SEC filings, the deal is financed in part by up to $1.0 billion of non-voting exchangeable perpetual preferred stock purchased by Pershing Square Holdings, the vehicle controlled by Bill Ackman. The deal is expected to close in Q2 2026, subject to regulatory approvals including Hart-Scott-Rodino clearance and insurance-specific sign-offs, with a long-stop date of December 2026.

The strategic logic mirrors the Berkshire Hathaway model: acquire an insurer to gain access to long-duration float, then deploy that capital into higher-returning investments. Pershing Square affiliates are expected to manage Vantage's investment portfolios post-close, further cementing the parallel. The acquisition price is approximately 1.5x Vantage's estimated year-end 2025 book value, according to Dealroom — a meaningful premium that signals confidence in Vantage's underwriting quality. This is part of the broader cross-sector acquisition wave repricing theme playing out across markets.

What makes this deal structurally different from a typical real estate acquisition is the capital model shift. HHH moves from a capital-intensive, development-driven real estate company to a diversified holding company with recurring insurance float. AM Best has placed Vantage and affiliates under review with developing implications — a signal that rating agencies see the transition as material enough to warrant scrutiny. For traders tracking the M&A acquisition wave, HHH becomes a case study in corporate identity transformation rather than simple bolt-on growth.

What This Means for Traders

The primary trading opportunity sits squarely in HHH stock. The announcement introduces a classic acquisition arbitrage setup: HHH's equity is being repriced around a new business model, while deal-completion risk — regulatory approval, financing execution, and AM Best's rating review — creates uncertainty that typically compresses a stock toward a discount. Traders should monitor whether HHH trades at a premium or discount to its implied post-deal NAV as regulatory milestones approach.

At the sector level, specialty reinsurers and insurance holding companies may see secondary repricing as the market reassesses acquisition multiples in the space. The 1.5x book value entry point for Vantage sets a visible comparable for peers. Separately, the M&A wave trading guide framework applies here: event-driven positioning around regulatory approval timelines (Q2 2026 target) is the key catalyst to track. Volatility in HHH could spike around any AM Best rating action or regulatory filing update. Since this news broke outside a standard session catalyst window, CoinUnited's 24/7 stock CFDs allow traders to position on HHH without waiting for the next NYSE open.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

The deal is pending insurance-specific regulatory approvals and Hart-Scott-Rodino clearance, with a long-stop date of December 2026 — meaning break risk is real. AM Best's review of Vantage's ratings adds a further complication traders should monitor.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.