Quick Links

Snowflake +35% on AI Earnings Beat: Leverage Scenarios & Sector Read-Through for SNOW CFD Traders

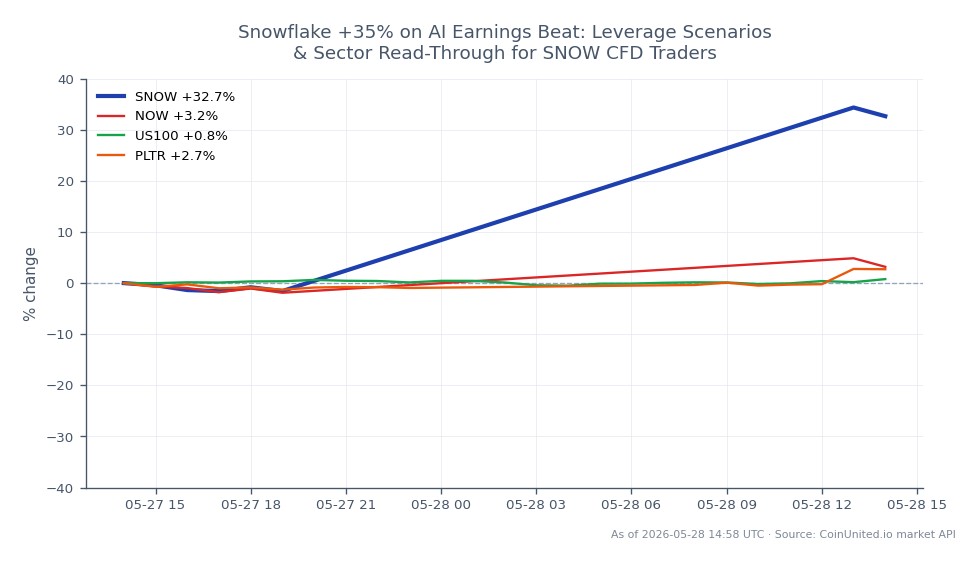

Data Snapshot

Key Takeaways

- •SNOW surged 34.58% to $235.01, reporting ~$1.28B Q4 FY2026 revenue (~30% YoY growth, ~230bps beat) — a violent short-squeeze driven by AI data-layer re-rating.

- •Leveraged short CFD positions above $175 with >20x leverage faced near-certain liquidation; new longs above $235 must size conservatively given post-earnings vol compression and a 5% drawdown wiping 20x margin buffers.

- •Sector read-through is broadly bullish for enterprise AI software — ServiceNow, Oracle, and Palantir are the highest-conviction sympathy plays.

- •NASDAQ 100 benefits from large-cap software re-rating; the move undermines the 'AI earnings cliff' narrative and supports risk-on positioning across growth tech.

- •Consensus analyst targets of ~$250+ imply residual upside, but the stock has closed much of that gap in a single session — follow-through confirmation in the next 48–72 hours is the key signal to watch.

According to MarketBeat and Perplexity Finance data, Snowflake Inc. (SNOW) surged approximately 34.58% in a single session — trading at $235.01 with an intraday high of $240.41 — on the back of a stro

Event Summary

According to MarketBeat and Perplexity Finance data, Snowflake Inc. (SNOW) surged approximately 34.58% in a single session — trading at $235.01 with an intraday high of $240.41 — on the back of a strong AI-driven earnings print. The company reported Q4 FY2026 revenue of approximately $1.28 billion, representing ~30% year-over-year growth and beating consensus by roughly 230 basis points, per research sources.

The move is especially notable given SNOW had been down approximately 35% YTD in 2026 heading into earnings, as investors questioned whether AI initiatives would translate into revenue. Management's framing of Snowflake as a critical data layer for AI training and inference — not an AI disruption victim — triggered violent short-covering and a growth multiple re-rating. This is squarely part of the broader AI-Cloud Enterprise Embedding Wave reshaping enterprise software valuations.

Leverage Impact Analysis

For traders using CoinUnited.io's stock CFDs (up to 2000x leverage), this 34.58% single-session move creates extreme leverage math — in both directions.

Long scenario: A trader holding a 50x long SNOW CFD opened at $175 (pre-earnings, near YTD lows) would see a gross return of ~1,729% on margin — a $1,000 margin position yielding ~$17,290 in P&L at $235.01. The key risk: leveraged longs opened *after* the spike are now entering at elevated implied volatility with compressed upside.

Short squeeze danger: Any remaining short positions with >20x leverage opened above $175 faced near-certain liquidation as SNOW ripped through resistance levels toward $240.41. With consensus analyst targets around $250+, short positions above current price remain at risk of further forced covering.

Volatility note: Post-earnings implied volatility will compress (vol crush), but realized volatility stays elevated. Traders using high leverage (100x+) on SNOW CFDs should size positions conservatively — a 5% retracement from $235 to $223 wipes a 20x position's 25% margin buffer. Monitor open interest on CoinUnited.io for confirmation of directional conviction.

Cross-Market Impact

Snowflake's move has clear read-through for the broader AI-Cloud enterprise integration trade. Sympathy bids are most likely in:

- -ServiceNow (NOW) and Oracle (ORCL): Direct peers in enterprise data/AI platforms. Strong SNOW AI monetization data reduces sector-wide fears of AI SaaS disruption and supports multiple expansion.

- -Palantir (PLTR): Re-rated higher on similar AI-data-layer narratives; SNOW confirmation of enterprise AI demand is broadly bullish.

- -NASDAQ 100 (US100): A +34% move in a large-cap software name adds visible basis points to the index, supporting growth-style benchmarks and potentially triggering momentum ETF inflows.

- -Microsoft (MSFT) and Meta Platforms: As hyperscale cloud providers and AI infrastructure heavyweights, sustained Snowflake workload growth implies increased compute/storage consumption on their platforms.

For macro context, a landmark AI software earnings beat reduces the "AI earnings cliff" narrative, supporting risk-on positioning broadly without significant FX or commodity spillover — this is primarily a tech/growth equities event.

Trading Considerations

Key levels: SNOW is trading at $235.01, with intraday range $229.54–$240.41. Analyst consensus targets around $250+ suggest continued upside, but the stock has already repriced a significant portion of that gap in one session. Watch for follow-through buying vs. a fade-and-consolidate pattern in the sessions ahead — earnings beat trading setups historically show the first 48–72 hours post-spike as the critical confirmation window.

Core risk: if AI monetization commentary fails to sustain in subsequent quarters, the stock remains vulnerable to another sharp de-rating. Competition from open-source data formats and alternative AI data platforms remains a structural concern cited by multiple research sources.

Trade Snowflake Inc. on CoinUnited.io

Trade SNOW with up to 800xx leverage → | Create Free Account

Frequently Asked Questions

Short positions with leverage above 20x opened below ~$175 would have been liquidated well before the $235 close. Any remaining shorts near current price with consensus targets at $250+ face continued squeeze risk — tight stop placement above $240.41 (intraday high) is the critical level to watch.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.