Quick Links

IQE Shares Hit 16-Year Low as Revenue Guidance Slashed 22% and Earnings Swing to Potential Loss

Data Snapshot

Key Takeaways

- •IQE revenue guidance cut to £90–100M from £115.1–123M, with core earnings now ranging from a £5M loss to a £2M profit — vs. prior £7.4–10M profit guidance.

- •Shares fell ~14% to 20.38p, reaching a 16-year low, confirming market re-rating of IQE's fundamental outlook.

- •Mobile handset and wireless market weakness is the primary driver, expected to persist through 2025 — a demand signal relevant to the broader semiconductor supply chain.

- •IQE has expanded its strategic review to include a potential full company sale after receiving an undisclosed approach, creating a speculative M&A overlay.

- •Large-cap AI-driven chip names are relatively insulated, but handset-cycle-exposed semiconductor suppliers face incremental sentiment pressure from this data point.

UK compound semiconductor maker IQE plc delivered a severe guidance cut that sent its shares to levels not seen in over 16 years. As reported by Reuters, IQE revised its core earnings forecast from a

Event Analysis

UK compound semiconductor maker IQE plc delivered a severe guidance cut that sent its shares to levels not seen in over 16 years. As reported by Reuters, IQE revised its core earnings forecast from a profit of £7.4–10 million down to a range spanning a £5 million loss to a £2 million profit — a swing that represents a roughly 60% downgrade at best. Revenue guidance was simultaneously cut from £115.1–123 million to £90–100 million, implying a shortfall of roughly 22% at the midpoint. Shares fell approximately 14% to 20.38p in early trade, according to Sharecast.

The operational driver is a familiar one in semiconductors: deteriorating mobile handset demand and weakness in wireless markets. What makes this earnings miss revenue shock particularly significant is the magnitude of the earnings range revision — from a comfortable profit zone to one that includes a loss scenario. This is not a minor guidance trim; it reflects a structural softening of IQE's core end-market that management acknowledges will persist through 2025.

Adding a strategic dimension, Reuters reported that IQE has expanded a review to include a potential sale of the entire company after receiving an approach from an undisclosed party. The company also confirmed its disposal of Taiwan operations is ongoing. This combination — operational distress plus a corporate event catalyst — creates a dual-driver situation that is uncommon for a company of IQE's size and adds a speculative overlay to what would otherwise be a straightforward earnings miss and guidance cut story.

What This Means for Traders

For traders focused on IQE directly, the price action indicates the market is now pricing sustained weakness rather than a one-quarter blip. A 14% single-day drop to a 16-year low, combined with a guidance range that includes a loss scenario, signals limited near-term support unless the M&A angle crystallizes. Traders should monitor whether any formal offer emerges — that would be the primary upside catalyst, and understanding how acquisitions move markets is key context here.

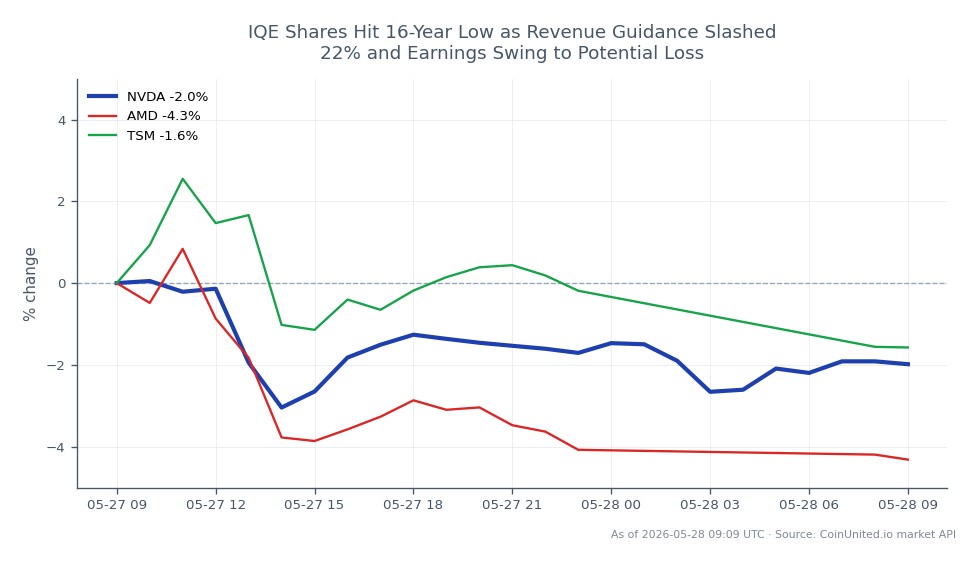

Beyond IQE itself, the handset and wireless demand signal carries read-through value for the broader semiconductor supply chain. The weakness IQE cites is consistent with soft consumer electronics cycles that could weigh on sentiment for other compound semiconductor and photonics-exposed names. While large-cap names like NVIDIA and AMD are more insulated due to their AI exposure, Taiwan Semiconductor Manufacturing Company and other handset-cycle-sensitive suppliers warrant attention as corroborating data points accumulate.

The M&A optionality introduces volatility asymmetry: downside is anchored by fundamental deterioration, but any confirmed takeover approach could trigger a sharp reversal. Traders comfortable navigating earnings miss recovery plays may find this setup relevant, though confirmation of a buyer is required before positioning for a bounce.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

Only if a formal offer is confirmed — unconfirmed approaches frequently lapse, and the underlying business deterioration provides continued downside pressure in the meantime. Wait for a named bidder before treating this as a pure acquisition play.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.