Quick Links

HSBC's $43B Microsoft–Anthropic Revenue Call: Leverage Angles on MSFT CFDs and AI Supply Chain

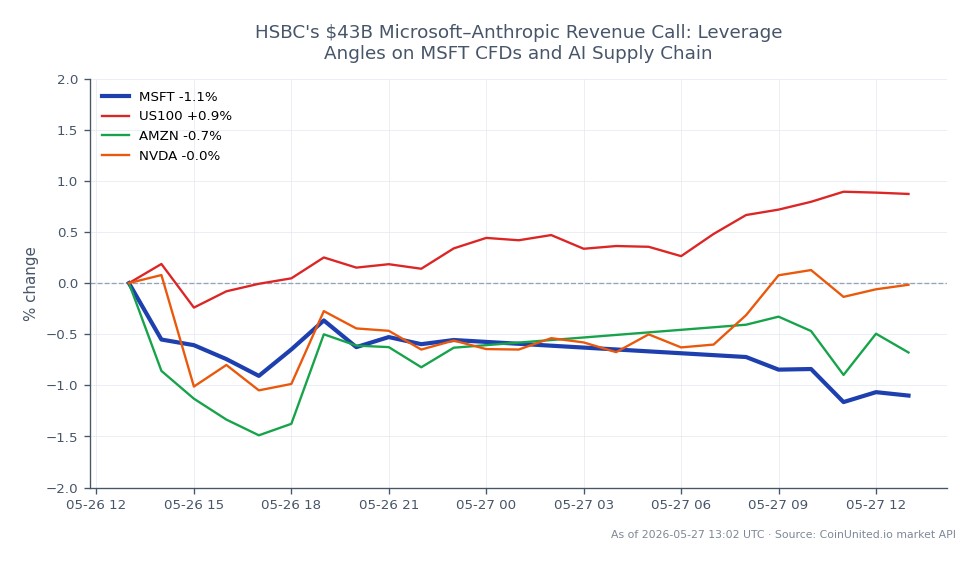

Data Snapshot

Key Takeaways

- •HSBC's $43B Microsoft–Anthropic revenue estimate is a sell-side projection, not contractual guidance — trade it as a sentiment/narrative catalyst, not a hard earnings signal.

- •MSFT CFDs at $412.99 with 50x leverage require only a 2% adverse move (~$404.73) to trigger liquidation — position sizing must reflect narrative-driven (not earnings-driven) volatility.

- •NVIDIA is the highest-conviction indirect beneficiary: more Anthropic workloads on Azure directly drives incremental GPU demand.

- •Amazon and Alphabet face relative competitive pressure as the HSBC framing positions Microsoft as capturing a disproportionate share of profitable AI workloads.

- •The NASDAQ-100 receives index-level support from MSFT re-rating, but macro/FX impact remains second-order with no Fed policy implications.

According to a research note cited by iTiger, HSBC analysts estimate that Microsoft's partnership with Anthropic could generate approximately $43 billion in incremental revenue for Microsoft over a mu

Event Summary

According to a research note cited by iTiger, HSBC analysts estimate that Microsoft's partnership with Anthropic could generate approximately $43 billion in incremental revenue for Microsoft over a multi-year horizon. The figure encompasses Azure cloud consumption from Anthropic's training and inference workloads, revenue-sharing on hosted model access, and pull-through demand for Microsoft's broader AI product suite including Copilot and enterprise solutions.

This is a sell-side projection, not company guidance or contractual commitment. No SEC filing or official Microsoft disclosure confirms the $43B figure. The signal's trading relevance lies in HSBC quantifying the scale of AI upside embedded in the Microsoft–Anthropic strategic partnership — a relationship that now sits alongside Microsoft's existing OpenAI alignment as a dual-model competitive moat.

Leverage Impact Analysis

MSFT CFDs are trading at $412.99 (24h range: $412.46–$414.94, down 0.54% on the day) — meaning the stock has not yet repriced meaningfully on this analyst call. That creates an asymmetric setup for leveraged traders who believe HSBC's thesis will gain consensus traction.

Worked example — 50x long MSFT CFD:

- -Entry: $412.99

- -A 2% move to ~$421.25 produces a 100% return on margin at 50x

- -A 2% adverse move to ~$404.73 triggers full margin wipe — position sizing is critical

Worked example — 100x long MSFT CFD:

- -The same 2% upside doubles capital; a 1% decline to ~$408.86 liquidates the position

- -Given MSFT's recent 24h low of $412.46, a 100x position opened at current price has less than 0.2% buffer before hitting that level

This is a sentiment/narrative catalyst, not a hard earnings beat — meaning price reaction may be delayed or distributed across sessions rather than immediate. Traders using high leverage on MSFT CFDs should account for the risk of intraday whipsaws before any sustained re-rating. Monitor funding rates and open interest on CoinUnited.io for confirmation signals. The AI-cloud enterprise embedding wave theme underpins medium-term directional bias but demands tight position sizing at extreme leverage.

Cross-Market Impact

NVIDIA (NVDA): The $43B revenue estimate implies substantial incremental Azure compute capacity. More Anthropic workloads on Azure = more GPU demand. NVDA CFDs remain the highest-conviction indirect beneficiary of this thesis, consistent with the AI revenue monetization and chip demand surge theme.

Amazon (AMZN): Competitively pressured in relative terms. AWS has its own Anthropic relationship via Bedrock, but HSBC's framing positions Microsoft as capturing disproportionate AI workload revenue share — a narrative headwind for AMZN's cloud story.

Alphabet (GOOGL): Similar relative-pressure dynamic. Google Cloud and Gemini compete directly; a stronger Microsoft AI monetization narrative widens the perceived gap.

NASDAQ-100 (US100): MSFT is a top index weight. Sustained re-rating of MSFT on AI revenue expectations provides index-level support, particularly for the tech-heavy US100 CFD.

Macro/FX: Impact is second-order. Stronger US tech earnings narratives marginally support USD via equity inflows but do not shift Fed expectations.

Trading Considerations

MSFT's current price of $412.99 sits just above the session low of $412.46, with the 24h high at $414.94 acting as immediate resistance. A clean break above $414.94 on volume would signal the market is beginning to price HSBC's upside scenario. Key risk factors include execution uncertainty on Anthropic's enterprise adoption curve, competitive pressure from open-source LLMs, and potential antitrust scrutiny of large-model-provider partnerships.

For traders tracking the broader AI infrastructure capital reallocation thesis, the Microsoft–Anthropic relationship adds another data point confirming hyperscaler model-partnership strategies as a durable revenue mechanism — not a one-off deal.

Trade Microsoft Corp. on CoinUnited.io

Trade MSFT with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

MSFT is trading at $412.99 — the stock hasn't repriced on this call yet, so leveraged longs are entering before consensus forms. At 50x, a 2% upside to ~$421 doubles capital, but the same 2% downside liquidates the position entirely.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.