Quick Links

QinetiQ +8% Earnings Beat: Leverage Scenarios & UK Defence Sector Read-Through

Data Snapshot

Key Takeaways

- •QinetiQ H1 FY26 underlying operating profit of £96.0m beat consensus despite a ~4.9% revenue decline, with FY26 EPS growth guided at +15–20% vs FY25.

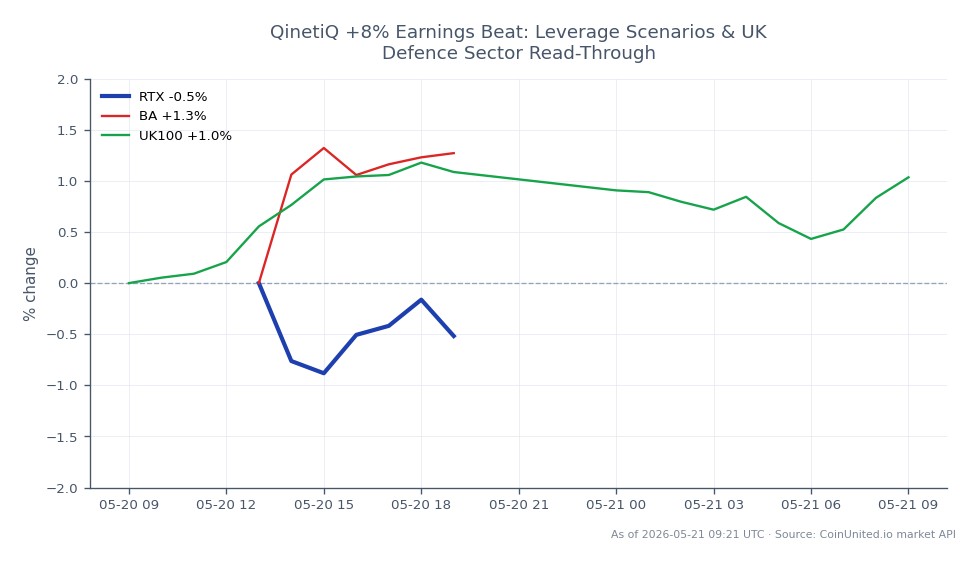

- •A 50x long QQ. CFD captured ~400% gain on margin from the ~8% share price move; short positions above 20x leverage faced liquidation on the gap.

- •The strategic review of QinetiQ's U.S. Federal business is the key medium-term catalyst — a clean divestiture would improve group margins and reduce earnings volatility.

- •UK/European defence peers (BAE Systems, Thales, Leonardo) see a mild positive read-through, confirming sustained defence spending and margin resilience across the sector.

- •Record order backlog provides high FY26 revenue coverage, compressing downside earnings risk and supporting a potential multiple re-rating toward the 500p resistance zone.

QinetiQ Group (LON: QQ.) shares surged approximately 8% after the UK defence technology firm reported FY26 results that beat consensus profit estimates. According to LSE RNS filings and AJ Bell covera

Event Summary

QinetiQ Group (LON: QQ.) shares surged approximately 8% after the UK defence technology firm reported FY26 results that beat consensus profit estimates. According to LSE RNS filings and AJ Bell coverage, H1 FY26 (six months to 30 September 2025) delivered underlying operating profit of £96.0m against £106.6m in the prior year — but crucially, the margin and earnings trajectory came in ahead of analyst expectations. The company reaffirmed FY26 guidance of c.3–5% revenue growth and 11–12% operating margins, alongside a 7.1% dividend increase to 3.0p.

Additionally, QinetiQ confirmed a strategic review of its U.S. Federal business unit — a lower-margin, operationally complex division. As reported by AJ Bell, the company had previously flagged guidance "before currency movements and the Federal IT disposal," signalling active portfolio optimisation. A record order backlog underpins visibility into FY26 and beyond, with full-year EPS growth guided at +15–20% vs FY25's base of 26.1p.

Leverage Impact Analysis

With QinetiQ shares up ~8% on the session, leveraged CFD traders on CoinUnited.io face asymmetric scenarios depending on direction and entry.

Long scenario: A trader holding a 50x long QQ. CFD entered before the earnings print sees the 8% underlying move amplified to a ~400% gain on margin deployed — a substantial return but also a reminder that pre-earnings leverage carries gap risk in both directions.

Short squeeze risk: Traders who were short QQ. at 20x leverage face a ~160% loss on margin from an 8% adverse move. Short positions opened near prior resistance (~430–460p range per MarketBeat data) face liquidation pressure if the stock holds above those levels post-print.

Volatility consideration: Post-earnings sessions typically see elevated intraday swings as broker upgrades and target price revisions flow in. Traders entering *after* the 8% gap should account for mean-reversion risk if the beat is partly driven by non-recurring items — position sizing at 10x–20x rather than maximum leverage is prudent until the U.S. unit review details crystallise. Monitor open interest and funding rates on CoinUnited.io for confirmation signals.

Cross-Market Impact

This result reinforces the drone imaging & defense tech breakout theme across UK and European defence. The most direct read-through is to BAE Systems (BA.) and RTX Corporation, where QinetiQ's margin resilience and record backlog validate sustained Western defence procurement budgets — mildly bullish for the sector.

The FTSE 100 Index sees marginal compositional support, though QinetiQ's primary weighting is in the FTSE 250. A broader cluster of strong UK defence earnings could support sterling-denominated equity flows at the margin. There is no material commodity or crypto spillover from this event — QinetiQ is a technology/services firm with limited raw material exposure.

For traders watching the financials & industrials earnings beat theme, QinetiQ's result adds another data point confirming that defence contractors with long-cycle backlogs are outperforming top-line softness through margin discipline — a playbook relevant to Thales, Leonardo, and Rolls-Royce.

Trading Considerations

Key levels to watch: prior resistance at 430–460p now acts as potential support post-gap; the 500p zone (noted by Fidelity/Sharecast in late 2025) represents the next meaningful resistance. The U.S. unit review is the pivotal catalyst — clarity on disposal vs. restructuring will determine whether the re-rating sustains. A clean divestiture at an accretive multiple would be incrementally bullish; a prolonged strategic review introduces uncertainty overhang.

Broker target price revisions in the 48–72 hours post-print are the key event to monitor. If consensus upgrades push the 12-month target above 500p, momentum buyers may extend the move. Downside risk centres on whether the £140m goodwill impairment (non-cash, FY25) signals deeper structural issues in the U.S. business.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

At 50x leverage, the 8% underlying move translates to approximately 400% gain or loss on margin — a long position profits dramatically while a short faces near-total margin wipeout. Traders holding overnight positions through the earnings print absorbed the full gap without opportunity to cut mid-move.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.