Quick Links

CAVA Smashes Comp Sales Estimates: Leverage Scenarios, Peer Read-Through & Key Levels

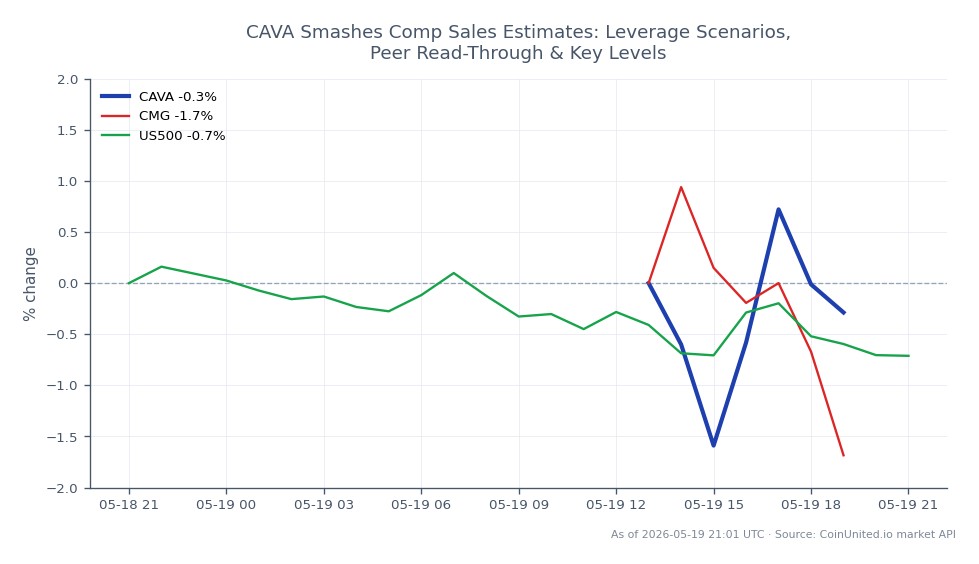

Data Snapshot

Key Takeaways

- •CAVA Q4 same-store sales came in at +0.5% vs. consensus of up to -1.4% — a major positive surprise driving a 26% intraday move to record highs.

- •Leverage risk is elevated post-gap: a 50x long CFD at the $79.70 intraday high is near liquidation at current $78.09 price — always size positions with post-earnings volatility buffers.

- •Management guided 2026 same-restaurant sales at +3–5%, above consensus, reinforcing the 'category decoupling' narrative from broader restaurant sector slowdown.

- •Cross-market read-through is positive for fast-casual peers like Chipotle (CMG) and Sweetgreen (SG); index impact on S&P 500 is marginal given CAVA's weighting.

- •Valuation dispersion is extreme — DCF fair value ~$34.82 vs. growth-model target ~$112 by 2028 — making each quarterly print a high-stakes binary event for both longs and shorts.

Cava Group (NYSE: CAVA) delivered a significant earnings beat in its Q4 and full-year 2025 results, with annual revenue surpassing $1 billion for the first time at approximately $1.17–$1.18 billion. A

Event Summary

Cava Group (NYSE: CAVA) delivered a significant earnings beat in its Q4 and full-year 2025 results, with annual revenue surpassing $1 billion for the first time at approximately $1.17–$1.18 billion. According to Reuters and confirmed by multiple sources, Q4 revenue came in at $275M (+21.2% YoY) versus the $268M consensus. The headline shock was same-store sales: analysts modeled up to a -1.4% decline, but CAVA posted a +0.5% increase — a meaningful positive delta driven by steady foot traffic, not just pricing. The stock surged as much as 26% intraday to record highs following the print, and is up approximately 30.3% in 2026 year-to-date. Management guided 2026 same-restaurant sales growth at 3–5%, above consensus, and signaled aggressive continued unit expansion.

A subsequent earnings report showed revenue of $331.8M (+28% YoY) with same-store sales of +10.8% and EPS of $0.22 — though the stock drifted lower after-hours on valuation concerns at ~180x current-year earnings.

Leverage Impact Analysis

CoinUnited.io offers CAVA stock CFDs with up to 2000x leverage and zero trading fees, making position sizing discipline critical around binary earnings events like this.

At the current live price of $78.09 (24h range: $76.84–$79.70, -2.32% on the day), consider these worked examples:

- -50x long CFD opened at $79.70 (yesterday's high): A -2.32% move to $78.09 represents a -116% move on margin — meaning a position opened at the intraday high is already near or past liquidation territory at 50x without adequate buffer.

- -10x long CFD opened at $78.09: A 5% pullback to ~$74.19 would erase approximately 50% of margin. Given post-earnings valuation overhang at ~180x earnings, 5–10% retracement moves are plausible within days.

- -Short-side risk: Any trader holding leveraged shorts pre-earnings faced a potential 26% gap — at 20x leverage, that's a 520% adverse move, an instant liquidation event.

The core leverage risk here is asymmetry: the earnings gap already occurred, meaning longs chasing the move face elevated liquidation risk if valuation concerns drive mean reversion, while shorts face re-acceleration risk if comps continue to beat. Traders should monitor open interest and funding rates on CoinUnited.io for directional confirmation. For broader context on how to trade earnings beats, position sizing relative to implied volatility is the critical variable.

Cross-Market Impact

CAVA's print is a positive read-through for growth-oriented fast-casual peers, particularly Chipotle Mexican Grill (CMG) and Sweetgreen (SG). The key message — that premium fast-casual concepts can decouple from sector-wide traffic slowdowns — supports a re-rating argument for best-in-class comps names. CMG CFD traders should watch whether Chipotle's next print confirms or denies the CAVA thesis.

At the index level, CAVA's direct weight in the S&P 500 is modest, limiting direct index impact. However, the beat contributes positive breadth to consumer discretionary within the index, a marginal supportive factor for US500 sentiment. The broader signal — that middle-to-upper-income consumers maintain discretionary spending capacity in 2026 — is a micro datapoint consistent with resilient demand narratives. This story fits the broader consumer earnings beat theme playing out across sectors.

No meaningful impact on forex, commodities, or crypto markets is expected from this single-stock event.

Trading Considerations

At $78.09, CAVA is trading well off its post-earnings record high surge but remains up ~30% YTD. Key near-term levels: the 24h low of $76.84 is immediate support; a break below opens a retest of pre-earnings consolidation zones. Resistance sits at the $79.70 intraday high. The valuation spread between a conservative DCF (~$34.82/share per Sahm Capital) and an aggressive growth model (~$112 by Dec 2028) underscores that every quarterly print is binary — guidance deceleration could trigger outsized multiple compression given a ~9.5x price/sales ratio.

Watch next quarter's same-restaurant sales print and unit opening cadence as the primary catalysts. Any deceleration from the 3–5% 2026 guidance range would be a high-conviction bearish signal.

Trade CAVA Group, Inc. on CoinUnited.io

Trade CAVA with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

At ~180x earnings and ~9.5x sales, CAVA has minimal margin for error; a 5–10% retracement (common post-earnings mean reversion) wipes out 50–100% of margin at 10–20x leverage. Traders holding high-leverage longs should set tight stop-losses near the $76.84 support level.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.