Quick Links

Oracle Slumps 10–12% Post-Earnings: Gross Margin Fear Overrides EPS Beat — Leverage Scenarios & Cross-Market Impact

Data Snapshot

Key Takeaways

- •ORCL fell 10–12% despite EPS and revenue beats, driven by gross margin concerns and plans to raise capital for AI infrastructure — a confirmed earnings-reaction dislocation.

- •Leverage risk is acute: a 50x long CFD opened near the $189 session high faces liquidation before the current $181.18 price level; position sizing must account for gap-down entry.

- •RPO of ~$138B (+41% YoY) confirms strong demand backlog, but markets are discounting the profitability of that backlog given AI-heavy cost structure.

- •Cross-market read: NASDAQ 100 faces incremental drag; AI hardware/data-center names see positive read-through as Oracle's capex confirms sustained infrastructure demand.

- •Capital raise structure is the key binary: equity issuance extends dilution risk and favors shorts; debt issuance is less equity-negative but widens credit spreads.

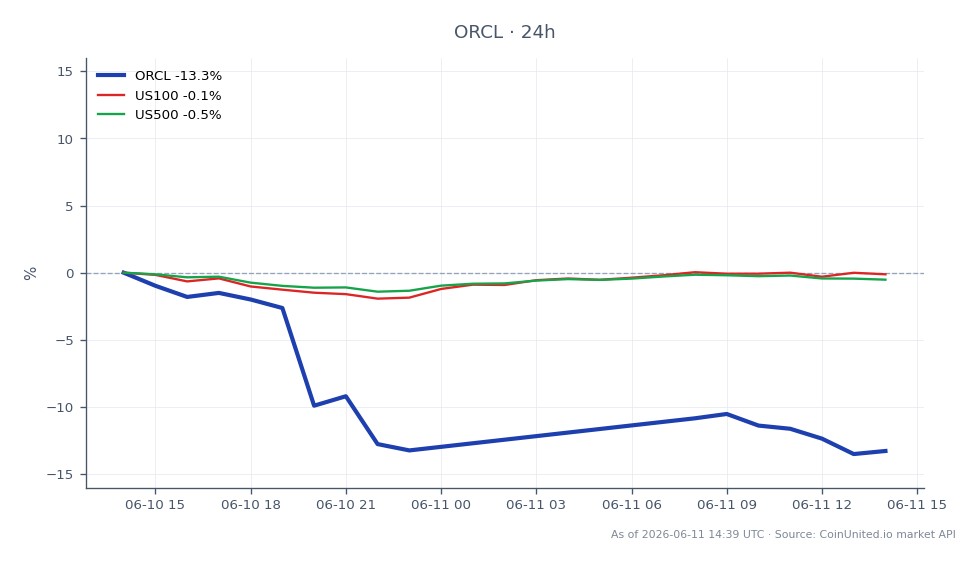

Oracle Corporation (ORCL) reported fiscal Q4 results that beat on both EPS and revenue — with approximately 21% revenue growth and 24% EPS YoY growth — and raised its full-year profit forecast. Accord

Event Summary

Oracle Corporation (ORCL) reported fiscal Q4 results that beat on both EPS and revenue — with approximately 21% revenue growth and 24% EPS YoY growth — and raised its full-year profit forecast. According to Oracle's own investor relations release, Remaining Performance Obligations (RPO) surged roughly 41% to ~$138B, signalling a robust contracted backlog. Despite the fundamental beat, ORCL shares dropped over 12% in extended trading and approximately 10% pre-market, as reported by CNBC, with the sell-off driven by gross margin pressure concerns and plans to raise significant new capital to fund AI infrastructure buildout. Live market data shows ORCL currently trading at $181.18, with a 24h range of $175.28–$189.17.

As reported by multiple sources including Seeking Alpha and CNBC, the market's reaction reflects the "good growth, expensive growth" dynamic: investors are repricing the stock on fears that AI-heavy capex will compress blended gross margins and depress near-term free cash flow. This is a classic earnings miss revenue shock pattern — where strong topline numbers are overshadowed by cost-structure concerns and capital allocation signals.

Leverage Impact Analysis

The 10–12% post-earnings gap creates asymmetric leverage risk. At CoinUnited's up to 2000x leverage on stock CFDs, even modest position sizing amplifies the move dramatically.

Long squeeze scenario: A trader holding a 50x long ORCL CFD opened at $189.00 (near the 24h high) would face approximately a 5.3% adverse move to the $179 range — representing a ~265% loss relative to margin at 50x, triggering liquidation well before the current $181.18 price. At 20x leverage, the same position survives to roughly $179.55 before margin exhaustion, meaning even moderate leverage long holders opened near the session high face severe pressure.

Short opportunity framing: Traders who opened short CFDs at the $185–$189 range following the earnings release captured a $6–$14 move. A 20x short at $187.00 with current price at $181.18 represents ~6.2% gain on the move, or ~124% return on margin — though with a stop above the 24h high of $189.17.

The capital raise narrative adds a second-order leverage risk: if Oracle proceeds with equity issuance, dilution expectations can extend the drawdown over days, not just the initial gap session. Traders should monitor open interest and check funding rates on CoinUnited.io for positioning confirmation. This event fits squarely within the broader AI datacenter energy and capital raise repricing theme, where high-capex commitments are being discounted faster than revenue beats are rewarded.

Cross-Market Impact

With a market cap around $515B (per Robinhood broker data), a 10–12% ORCL move is non-trivial for tech-weighted indices. The NASDAQ 100 Index carries measurable ORCL weight, and the sell-off adds incremental drag on software/cloud sector ETFs. The S&P 500 Index impact is more diluted but present on high-volume days.

The read-through extends to enterprise software peers — Salesforce, Inc., Adobe Inc., and Datadog, Inc. — where investors may similarly reprice AI capex intensity against margin expectations. AI chip and data-center hardware names see a *positive* read-through, as Oracle's heavy spend confirms sustained infrastructure demand — relevant context for NVIDIA and the broader AI CapEx supercycle thesis.

From a macro lens, this is a micro/sector event with limited direct forex or commodity spillover. However, if Oracle-style capital raises proliferate across large tech, incremental corporate bond supply could widen credit spreads modestly at the margin.

Trading Considerations

Key levels based on live data: immediate support at the 24h low of $175.28; resistance at $185–$189 range (pre-earnings base). The $175 zone is critical — a break lower on sustained volume could accelerate the drawdown if analyst downgrades follow. The P/E of ~34.5x (per Robinhood data) remains elevated for a margin-compressing story, suggesting multiple compression risk persists until Oracle provides clearer AI gross margin guidance.

Watch for: analyst price target revisions in the 24–48 hours post-print, any clarification on debt vs. equity capital raise structure (equity raise = greater downside; debt raise = spread widening but less equity dilution), and whether RPO-to-margin conversion timelines are addressed in the analyst call. For traders studying how to trade earnings misses, the post-print drift window is typically 3–5 sessions.

Trade Oracle Corporation on CoinUnited.io

Trade ORCL with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

A 50x long opened near $189 (the 24h high) would be liquidated before prices reached $181, as the ~4.2% adverse move exceeds the ~2% margin buffer at that leverage. Traders should size down significantly for post-earnings gap environments.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.