त्वरित लिंक

Criteo Surges 29% on Vista Equity Takeover Report — Leverage Scenarios & Ad-Tech Read-Through

डेटा स्नैपशॉट

मुख्य निष्कर्ष

- •Criteo's 29% spike is rumor-stage only — no binding deal or SEC filing confirmed, per Reuters reporting on the active sale process.

- •Leveraged long CFD positions opened near the post-spike price face acute deal-break reversal risk; Criteo failed to close prior M&A talks in both 2021 and 2023.

- •Analyst fair value consensus sits in the mid-$20s to low-$40s; bull-case take-private scenarios reference $60+, defining the risk/reward corridor.

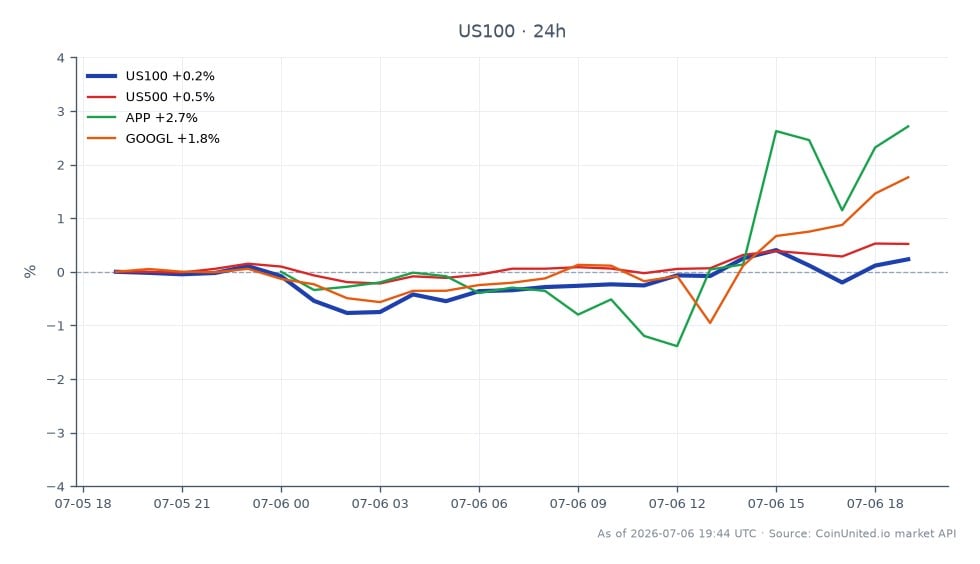

- •Cross-market impact is limited — ad-tech peers (AppLovin, Meta, Alphabet) may see modest sympathy repricing, but major index impact is negligible.

- •Vista Equity's enterprise software focus and reported dry powder reinforces the broader PE acquisition wave theme for data-centric mid-cap tech names.

Shares of Criteo S.A. (NASDAQ: CRTO), the French advertising technology firm, surged approximately 29% following reports of a takeover approach by Vista Equity Partners, a major private equity firm fo

Event Summary

Shares of Criteo S.A. (NASDAQ: CRTO), the French advertising technology firm, surged approximately 29% following reports of a takeover approach by Vista Equity Partners, a major private equity firm focused exclusively on enterprise software. As reported by Reuters, Criteo has been running an active sale process, with prior Bloomberg reporting in 2021 noting earlier takeover inquiries that ultimately failed to close. The current move represents the latest chapter in a multi-year M&A acquisition wave around mid-cap ad-tech assets.

The specific bid price and deal terms from Vista remain at the rumor/media-reported stage — no binding agreement or SEC filing has been confirmed. Reuters previously noted that sell-side commentary suggested Criteo could justify valuations north of $60 per share in some analyses, implying meaningful upside from pre-rumor levels near the mid-$30s. The prior sale-process report in 2023 sent CRTO up ~8% to approximately $33, giving the company a market cap around $2 billion at that time.

Leverage Impact Analysis

This is a classic event-driven, single-stock volatility scenario — the highest-risk environment for leveraged CFD traders.

Long-side scenario: A trader holding a 50x long CRTO CFD who entered before the 29% spike sees amplified gains — but also faces the primary risk of a deal-break reversal. Given Criteo's history of failed negotiations (per Reuters), a denial or collapse in talks could erase 15–25% rapidly, liquidating high-leverage longs opened near the post-spike price.

Short-side danger: Any trader shorting into this 29% move at elevated leverage faces acute squeeze risk. With M&A rumor momentum active, short positions above 20x face liquidation exposure on any incremental bid confirmation headline.

Key leverage consideration: With no confirmed deal terms, this remains a rumor-stage trade. Position sizing should reflect the binary outcome risk — full deal confirmation re-rates the stock further; deal collapse returns CRTO toward pre-rumor fundamentals (mid-$20s to low-$30s per analyst consensus). Traders should monitor open interest on CoinUnited.io for positioning confirmation signals before sizing up.

For context on how buyout offers structurally reprice targets, see acquisition repricing mechanics.

Cross-Market Impact

The cross-sector acquisition repricing read-through is limited but real for ad-tech peers. Meta Platforms and Alphabet (Google) are not M&A targets, but a visible PE bid for Criteo validates the strategic value of programmatic advertising infrastructure — modestly supportive for sentiment across the digital ads complex. AppLovin Corporation operates in the adjacent performance advertising space and may see minor sympathy repricing on increased deal speculation.

For major indices, the impact on the NASDAQ-100 and S&P 500 is marginal given Criteo's mid-cap, sector-specific weighting. The more meaningful signal is for thematic ad-tech ETFs and software PE deal-flow narratives — Vista's activity reinforces that private equity retains dry powder for data-rich software platforms even in a higher-rate environment.

Forex and commodities channels see negligible direct impact. There are minor EUR/USD cash flow considerations given Criteo's French domicile, but not at a tradeable macro scale.

Trading Considerations

Key levels to watch: pre-rumor consensus fair value sits in the mid-$20s to low-$40s range per analyst estimates (Simply Wall St / sell-side), with some bull-case take-private scenarios referencing $60+. The current 29% spike prices in a meaningful deal probability premium — gap-down risk on deal denial is substantial.

Criteo's repeated history of failed sale processes (2021, 2023 per Reuters/Bloomberg) means deal-break probability is non-trivial. Watch for any SEC Form 8-K filing or official company statement as the confirmation trigger. Until then, this is a merger arbitrage setup with elevated headline risk in both directions.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

अक्सर पूछे जाने वाले प्रश्न

Treat this as a binary event — position size should be small enough to survive a 20–25% reversal if deal talks collapse, as Criteo has failed to close M&A negotiations twice before (2021, 2023 per Reuters). Avoid high-leverage entries at the post-spike price without a confirmed SEC filing.

जारी रखें अन्वेषण

अस्वीकरण: यह संक्षेप केवल शैक्षिक उद्देश्यों के लिए है और यह निवेश सलाह नहीं है।