त्वरित लिंक

Sodexo Q3 Organic Revenue Beats Consensus, Raises Full-Year Outlook — What It Means for European Markets

डेटा स्नैपशॉट

मुख्य निष्कर्ष

- •Sodexo reported Q3 organic revenue growth of +10.5% in its strongest beat cycle (FY2023), raising full-year guidance to close to +11% — materially above prior consensus.

- •North American segment strength (~9% organic growth in peak periods) across healthcare, education, and corporate services signals broad volume resilience, not just pricing.

- •Net debt/EBITDA of 1.8x and a €2.70 proposed dividend reinforce Sodexo's quality-defensive profile, attracting factor investors post-beat.

- •EUR/USD headwinds are a structural risk: a -2.1% to -4.0% FX drag on revenues means euro appreciation can erode organic beats at the reported level.

- •Index-level spillover into the CAC 40, EURO STOXX 50, and STOXX Europe 600 is directionally positive but modest given Sodexo's weighting.

Sodexo SA (EPA: EXHO) has reported Q3 organic revenue growth that exceeded analyst consensus and upgraded its full-year guidance — a pattern most clearly demonstrated in the company's Q3 Fiscal 2023 u

Event Analysis

Sodexo SA (EPA: EXHO) has reported Q3 organic revenue growth that exceeded analyst consensus and upgraded its full-year guidance — a pattern most clearly demonstrated in the company's Q3 Fiscal 2023 update, when the company reported +10.5% organic revenue growth and raised its full-year group organic growth target to close to +11%, with underlying operating margin guidance set at 5.5%. According to Sodexo's official investor communications, consolidated Q3 revenues reached approximately €6.0bn, and On-Site Services posted +9.9% organic growth. The guidance raise confirmed a material positive inflection in the company's post-pandemic recovery trajectory.

What distinguishes this event from routine quarterly updates is the combination of a top-line beat *and* a margin trajectory upgrade. As detailed in Sodexo's newsroom releases, the company's North American operations have been a key engine, with regional organic growth reaching approximately +9% in certain periods, driven by corporate services, healthcare, education, and sports/leisure segments. This breadth of segment strength implies genuine volume recovery rather than pure pricing uplift — a more durable signal for investors assessing earnings quality.

For context, the trajectory has moderated in subsequent years: Q3 FY2024 delivered +6.8% organic growth (confirmed at the top of the +6–8% range), while Q3 FY2025 came in at +3.0%, with guidance revised to the lower end of targets. The guidance-raise scenario is therefore most relevant in high-momentum periods where organic growth meaningfully exceeds the midpoint of the company's prior range. Traders reading earnings beats across sectors should note that Sodexo's beat cycles have historically been tied to broader services-sector normalization waves.

A notable cross-market dimension: Sodexo's Q3 FY2025 results showed revenues reduced by 2.1% due to currency effects, primarily USD depreciation versus EUR, and Q1 FY2026 guidance flagged a -4.0% FX drag from the same source. This makes Sodexo's earnings a useful proxy for the sensitivity of pan-European multinationals to EUR/USD dynamics — a theme relevant beyond the stock itself.

What This Means for Traders

The immediate tradeable impact centers on Sodexo equity (EXHO) and sector read-through into European business-services peers. A guidance raise, combined with an organic growth beat, typically drives positive EPS revisions and multiple expansion via higher EV/EBITDA and P/E re-rating. With net debt/EBITDA at a conservative 1.8x and a proposed dividend of €2.70 (per Sodexo's FY2025 results), the stock offers a quality-defensive profile that can attract factor-driven buyers — particularly in risk-on European equity sessions. Traders exploring how to systematically approach these setups can reference the Q1 earnings beats and outlook upgrade trading guide for framework.

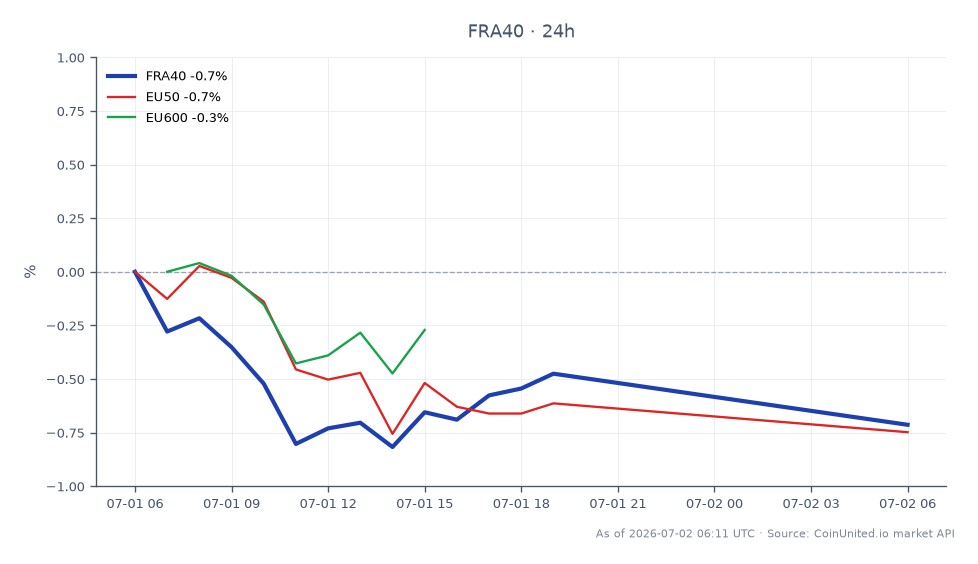

At the index level, EXHO's weight in French large-cap and pan-European baskets creates modest positive spillover for the CAC 40 Index, the EURO STOXX 50 Index, and the STOXX Europe 600 Index. The effect is diffuse but directionally constructive for European consumer services and industrials exposure. Sentiment is broadly risk-on for European equities in the near term, though the persistence of the move depends on whether management commentary on pricing power and margin improvement holds through the full-year result.

One structural caveat: the EUR/USD FX drag on Sodexo's reported revenues means that a strengthening euro creates a headwind for future guidance. Traders with positions in European multinationals should monitor EUR/USD closely, as outlined in the Fed vs. ECB macro policy divergence guide, since currency moves can erode organic growth beats at the reported revenue level.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

अक्सर पूछे जाने वाले प्रश्न

In FY2023, the raise was material — moving from mid-range expectations to 'close to +11%' organic growth, with margin guidance also tightened upward. In FY2024 and FY2025, guidance was confirmed rather than raised, making the FY2023 episode the clearest 'beat and raise' cycle.

जारी रखें अन्वेषण

अस्वीकरण: यह संक्षेप केवल शैक्षिक उद्देश्यों के लिए है और यह निवेश सलाह नहीं है।